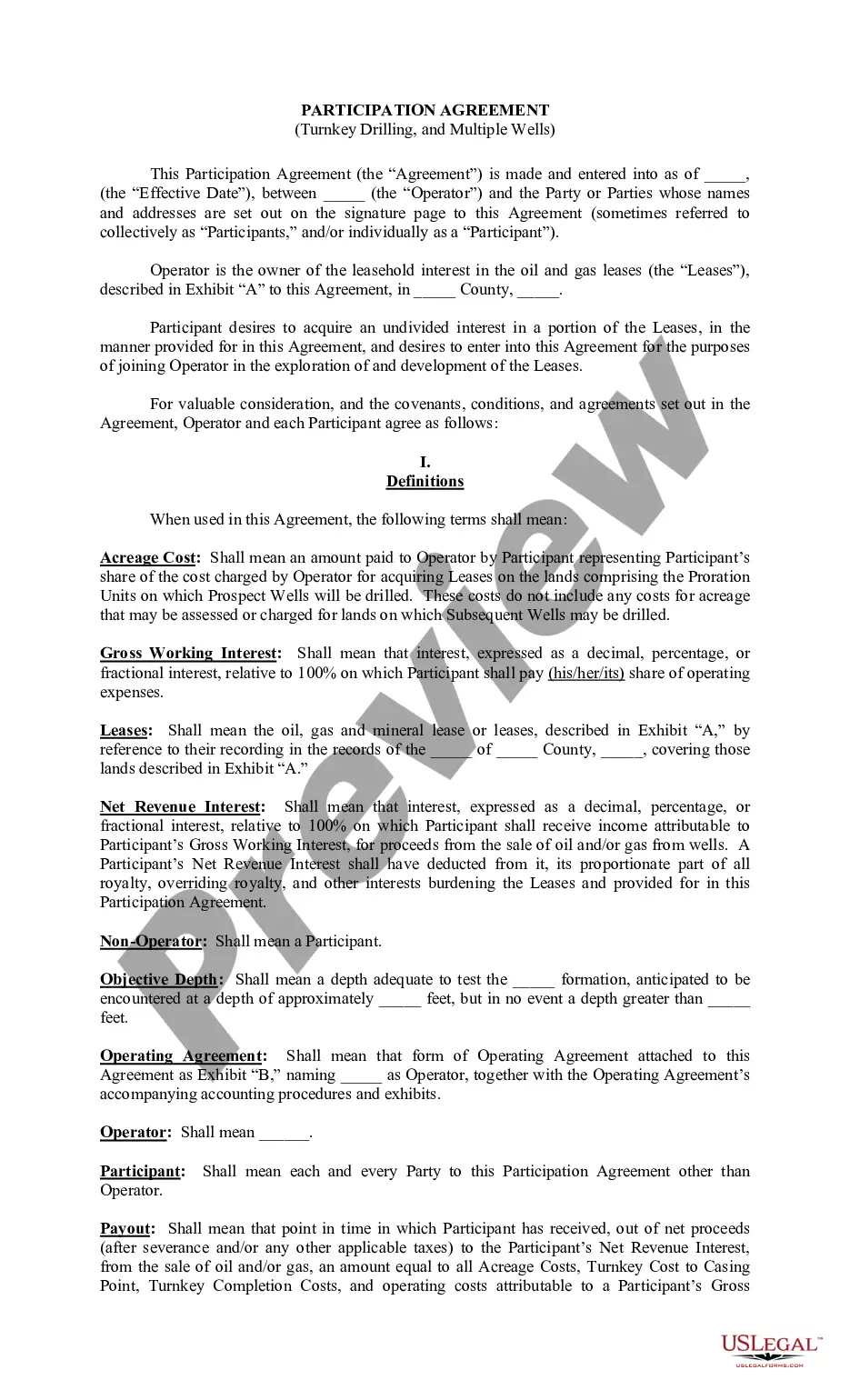

The Agreement is between an Operator and Participant. The Operator is the owner of the oil and gas leases covering the acreage described as the Contract Area in the Operating Agreement attached to this Agreement as Exhibit A . The Participant desires to acquire an undivided percent leasehold working interest in the Leased Acreage, and participate in drilling the well, which will be an approximate ft. test, which will be located on the Leased Acreage.

Participation Agreement for Single Well

Category:

State:

Multi-State

Control #:

US-OG-218

Format:

Word;

Rich Text

Instant download

Description

Free preview

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Built-in online Word editor

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Export easily

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

E-sign your document

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

Notarize online 24/7

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

Store your document securely

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Participation Agreement For Single Well?

When it comes to drafting a legal form, it is better to leave it to the professionals. However, that doesn't mean you yourself cannot get a template to utilize. That doesn't mean you yourself cannot get a sample to use, nevertheless. Download Participation Agreement for Single Well from the US Legal Forms web site. It provides numerous professionally drafted and lawyer-approved documents and templates.

For full access to 85,000 legal and tax forms, users simply have to sign up and choose a subscription. Once you’re registered with an account, log in, look for a specific document template, and save it to My Forms or download it to your gadget.

To make things much easier, we have provided an 8-step how-to guide for finding and downloading Participation Agreement for Single Well fast:

- Be sure the document meets all the necessary state requirements.

- If possible preview it and read the description before buying it.

- Click Buy Now.

- Choose the appropriate subscription to meet your needs.

- Make your account.

- Pay via PayPal or by credit/bank card.

- Select a needed format if a number of options are available (e.g., PDF or Word).

- Download the document.

Once the Participation Agreement for Single Well is downloaded you are able to complete, print out and sign it in almost any editor or by hand. Get professionally drafted state-relevant documents within a matter of minutes in a preferable format with US Legal Forms!

Form popularity

FAQ

That can include private benefit, inurement, lobbying, political campaign activity, excessive unrelated business income, not filing an annual 990 tax information form, and failing to achieve its original purpose.

Political activity. All section 501(c)(3) organizations are prohibited from directly or indirectly participating in, or intervening in, any political campaign on behalf of (or in opposition to) any candidate running for public office. The prohibition applies to all campaigns (federal, state and local level).

IRC 501(c)(4), (c)(5), and (c)(6) organizations may engage in political campaigns on behalf of or in opposition to candidates for public office provided that such intervention does not constitute the organization's primary activity.

A 501(c)(3) organization may engage in some lobbying, but too much lobbying activity risks loss of tax-exempt status.Organizations may, however, involve themselves in issues of public policy without the activity being considered as lobbying.

In general, no organization may qualify for section 501(c)(3) status if a substantial part of its activities is attempting to influence legislation (commonly known as lobbying). A 501(c)(3) organization may engage in some lobbying, but too much lobbying activity risks loss of tax-exempt status.

For example, a section 501(c)(3) organization may not publish or distribute printed statements or make oral statements on behalf of, or in opposition to, a candidate for public office. Consequently, a written or oral endorsement of a candidate is strictly forbidden.

Currently, the law prohibits political campaign activity by charities and churches by defining a 501(c)(3) organization as one "which does not participate in, or intervene in (including the publishing or distributing of statements), any political campaign on behalf of (or in opposition to) any candidate for public

Exemption Requirements - 501(c)(3) Organizations To be tax-exempt under section 501(c)(3) of the Internal Revenue Code, an organization must be organized and operated exclusively for exempt purposes set forth in section 501(c)(3), and none of its earnings may inure to any private shareholder or individual.