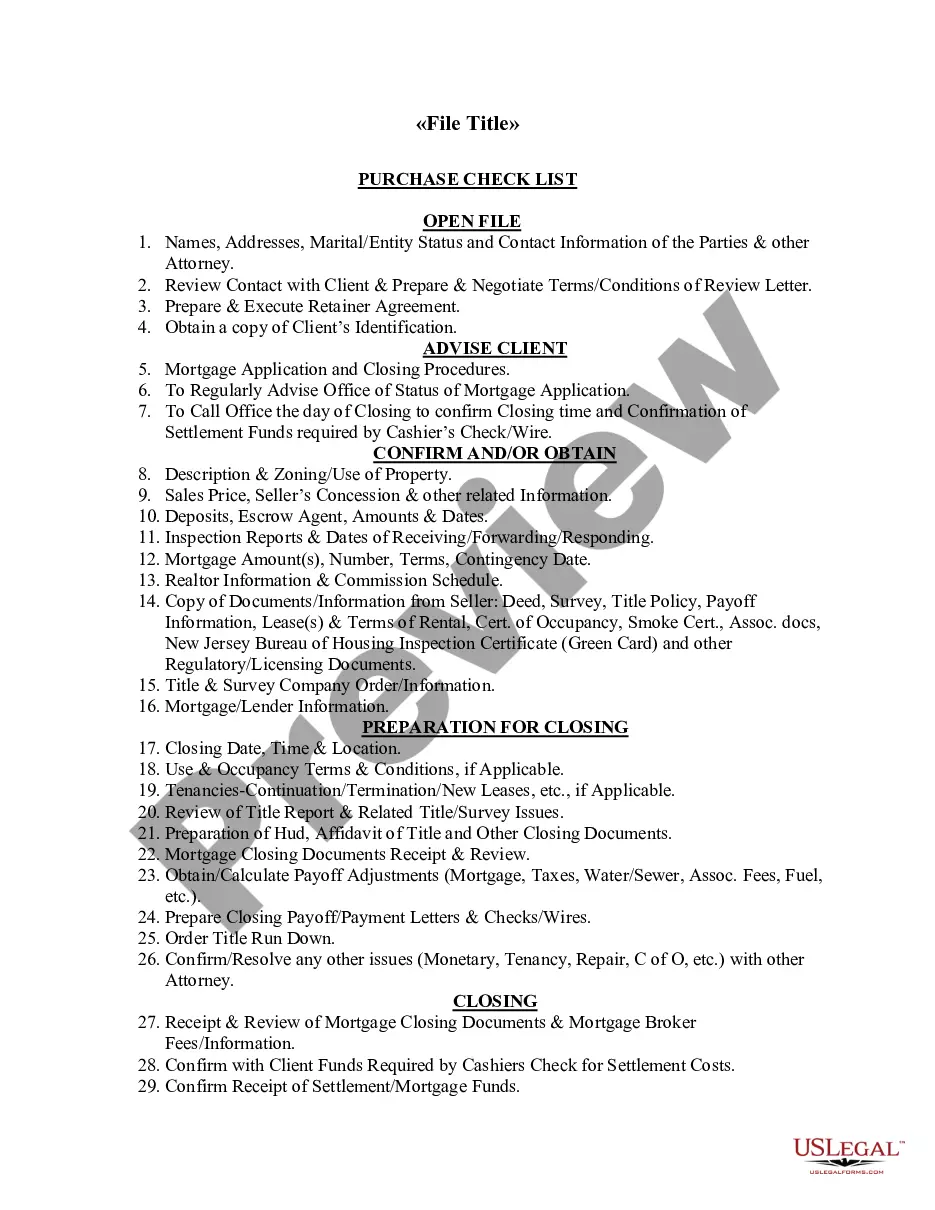

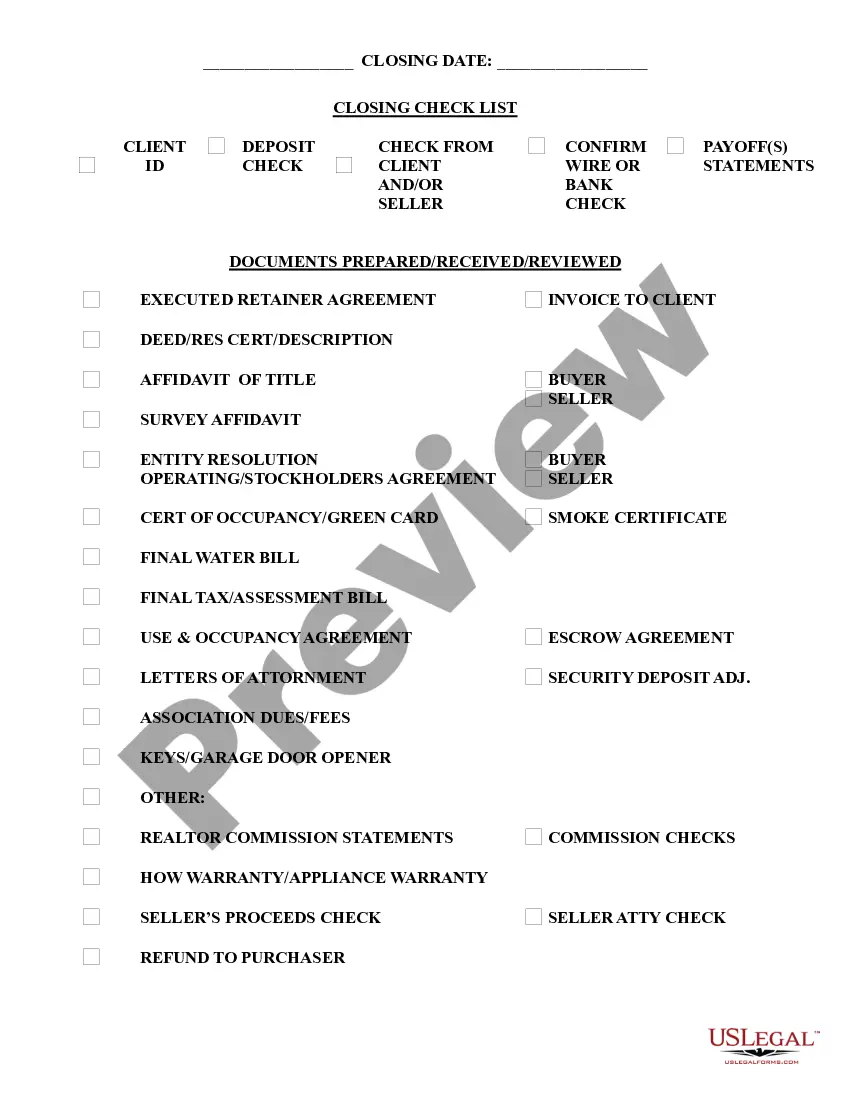

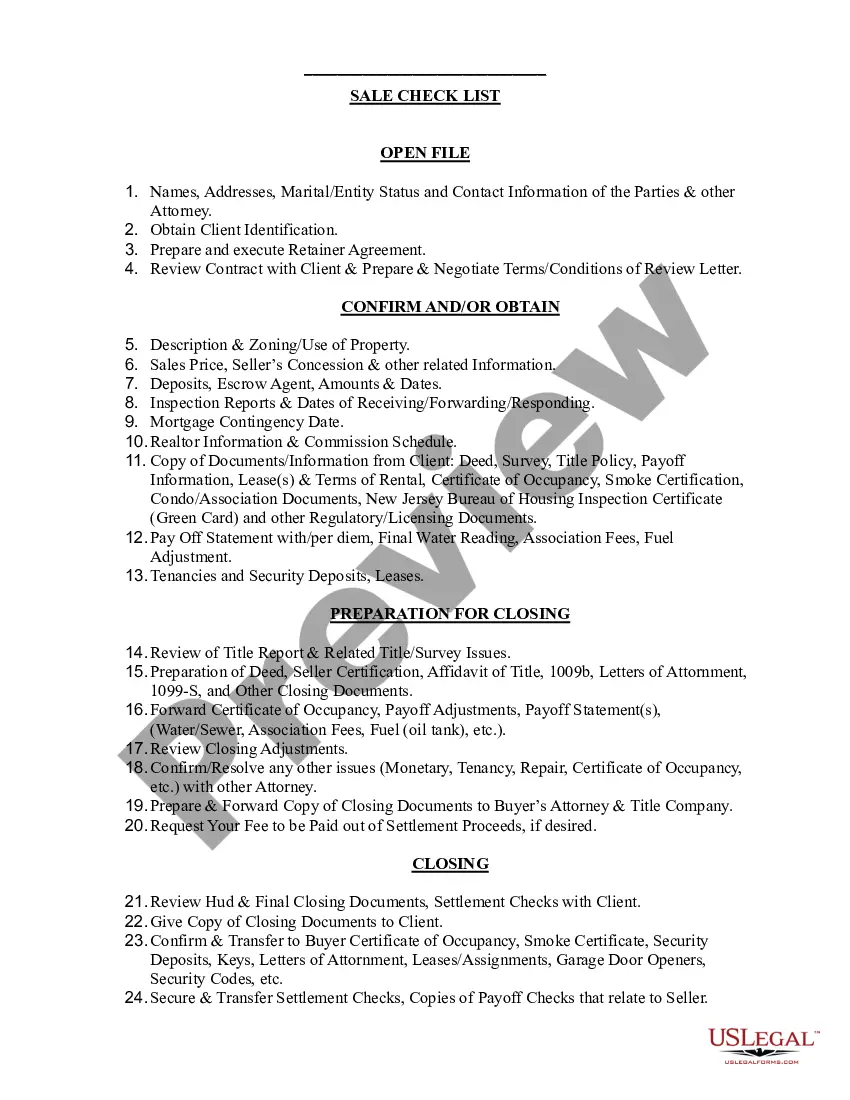

Check List: Refinance property

Overview of this form

The Check List: Refinance property serves as a comprehensive guide for individuals or entities considering refinancing their real estate. This document outlines the essential steps and information needed to navigate the refinancing process efficiently, distinguishing itself from similar forms by focusing specifically on a checklist approach to due diligence and preparation.

What’s included in this form

- Client information, including names, addresses, and contact details.

- Identification requirements for the client.

- Preparation and execution of a retainer agreement.

- Mortgage application and closing procedure details.

- Documentation needed for closing, such as title reports and payoff statements.

- Post-closing tasks like recording documents and forwarding pertinent checks.

Situations where this form applies

This checklist is useful during the refinancing of a property. It can guide users through critical phases such as gathering necessary documentation, preparing for closing, and ensuring that all legal requirements are met. Utilize this form when you are ready to start the refinancing process or need to organize tasks involved in the transition from one mortgage to another.

Who this form is for

Individuals and entities seeking to refinance real property should use this checklist. It is designed for:

- Homeowners looking to lower their mortgage rates or alter their loan terms.

- Real estate investors wanting to improve their cash flow through refinancing.

- Lending professionals who provide refinancing services.

How to prepare this document

- Identify the client's personal information, including their contact details and marital status.

- Collect necessary identification and documentation from the client.

- Draft and execute a retainer agreement outlining the terms of service.

- Gather critical information regarding the mortgage, including amounts and terms.

- Prepare for closing by confirming the date, time, and location, and ensure all documents are ready.

Does this document require notarization?

This form does not typically require notarization unless specified by local law. Always check your state's requirements regarding notarization to ensure compliance during the refinancing process.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Typical mistakes to avoid

- Failing to obtain a mortgage payoff statement before closing.

- Not confirming closing details in advance, leading to potential delays.

- Missing essential documents required for the refinancing process.

- Overlooking state-specific rules that may impact the refinancing procedure.

Advantages of online completion

- Convenient access to a structured guide that simplifies the refinancing process.

- Ability to edit and customize the checklist to fit individual needs.

- Reliable information drafted by licensed attorneys, ensuring legal accuracy.

Looking for another form?

Form popularity

FAQ

One refinance option is a cash-out refinance, which allows homeowners to reduce their equity in return for cash and grants them better rates. After closing, the homeowner receives a check that they can use for anything from paying off debt to improving their home.

If the appraised value comes in lower than what you owe on the mortgage, you may have to put off refinancing. A lower-than-expected appraisal can also dash hopes of getting rid of private mortgage insurance on a conventional loan, or reduce the amount of cash the lender will let you pocket in a cash-out refinance.

They'll look at your income, assets, debt and credit score to determine whether you meet the requirements to refinance and can pay back the loan. Some of the documents your lender might need include your: Two most recent pay stubs. Two most recent W-2s.

You'll also want to make sure that you give your home a deep cleaning a few days before your appraisal to reduce clutter. Make sure that everything is neat, put away and in its place before your appraiser arrives.

Understanding refinancing closing documents Closing disclosure. The closing disclosure provides the actual fees, costs and credits associated with closing your loan.Promissory note.Deed of trust.Affidavits and declarations.

If you are ready to have your home appraised, you should address any significant issues that may affect your home's value?such as damaged flooring, outdated appliances, and broken windows. A messy home should not affect an appraisal, but signs of neglect may influence how much lenders are willing to let you borrow.

Appraisers flush toilets, turn on all faucets and ensure that both hot and cold water are working. The water heater must be in working order and strapped ing to local code.

There are several things an appraiser looks for in a refinance. These include your home's condition and size, comparable properties, home system conditions, amenities, improvements and remodels, negative features, and location.