Full, Final and Absolute Release

What this document covers

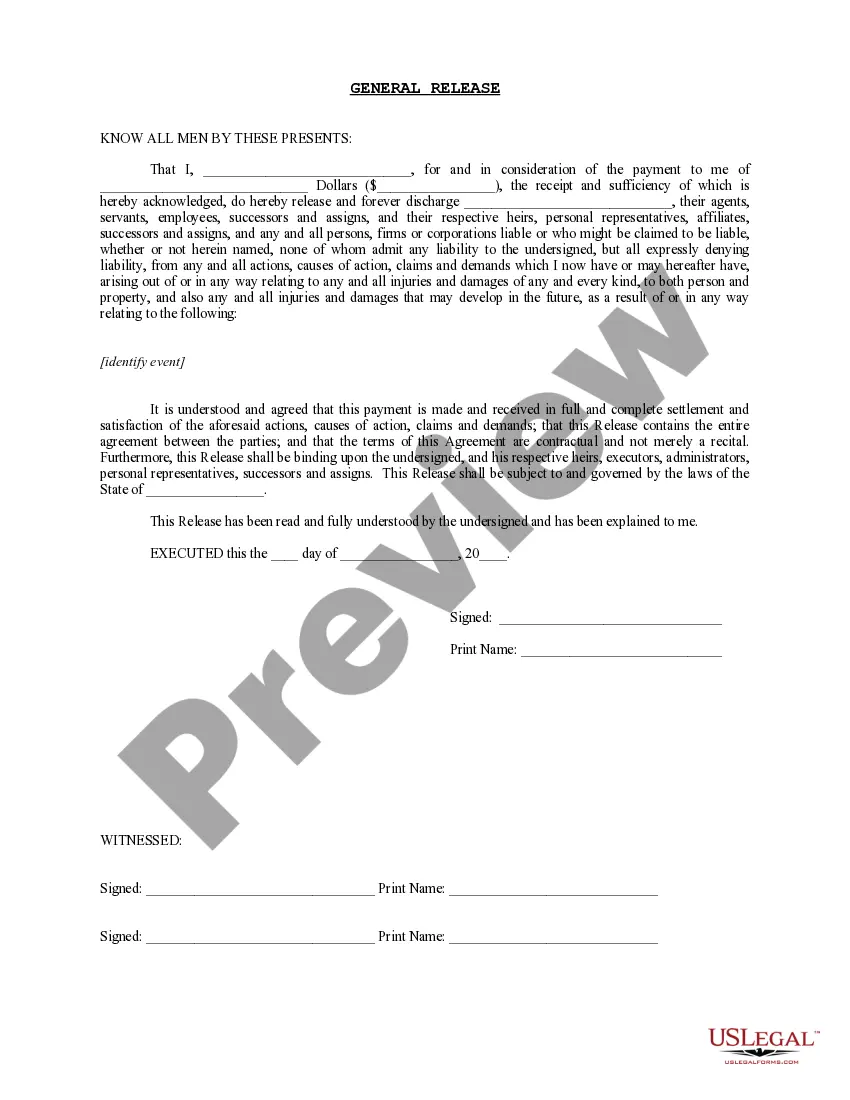

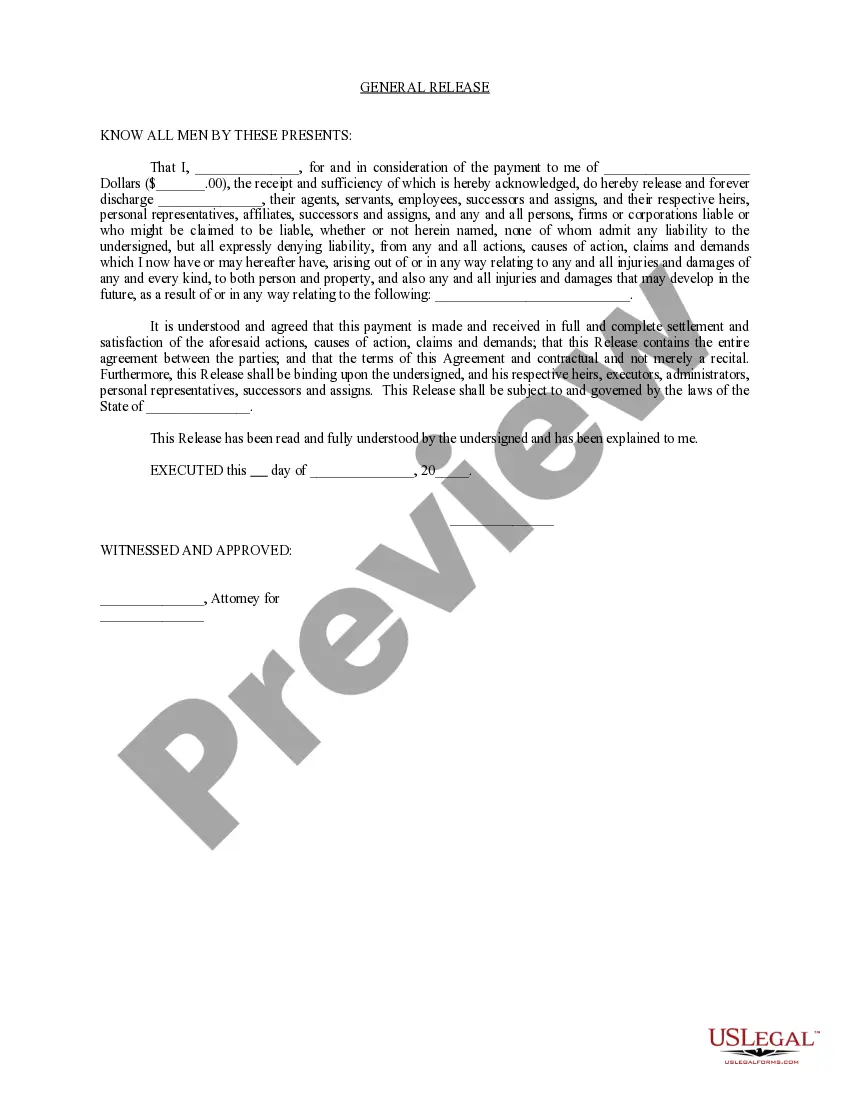

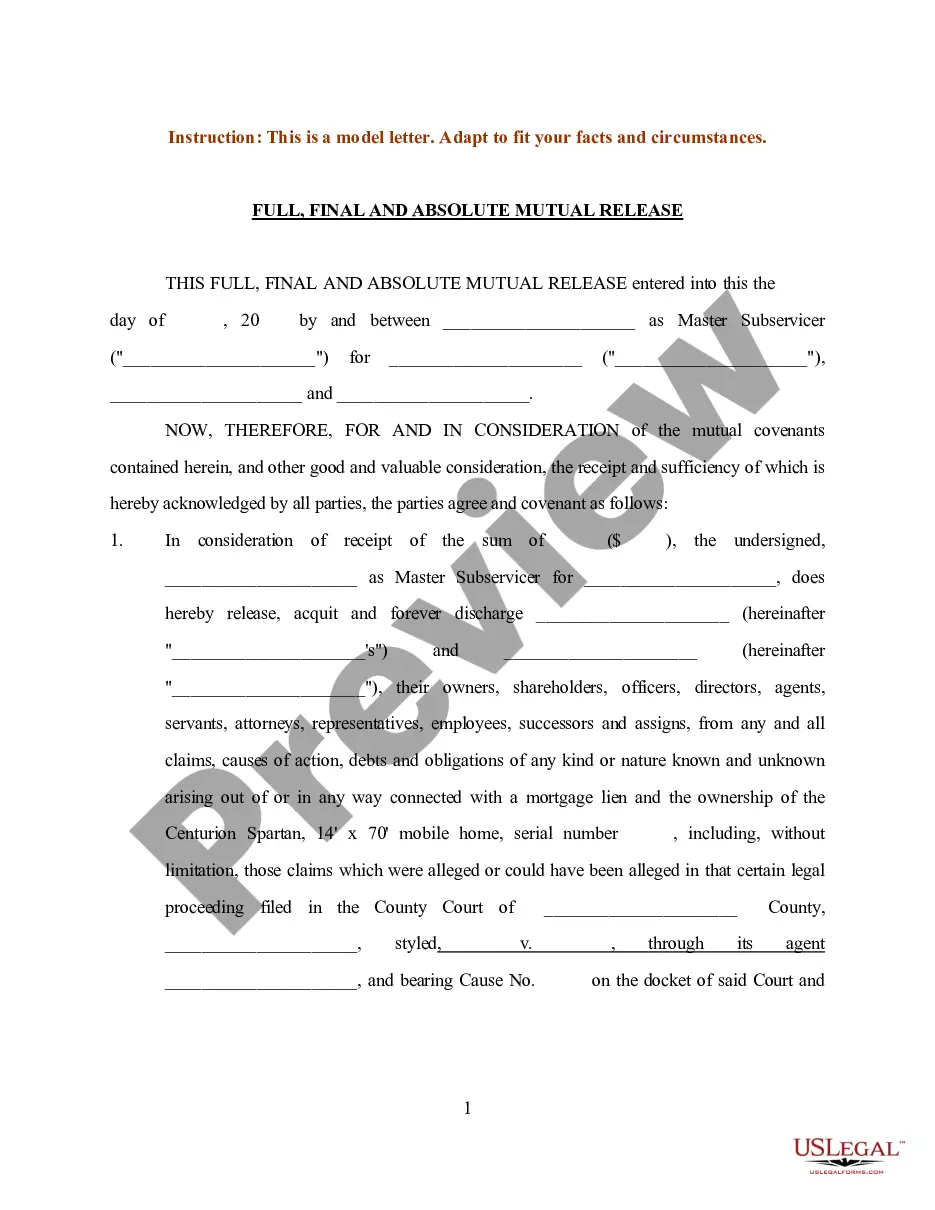

The Full, Final and Absolute Release is a legal document that allows the releasor to relinquish any claims against the releasee, particularly those related to a fire and the cancellation of an insurance policy. This form is distinct from other release agreements as it ensures no liability is admitted by the releasee while confirming the total and final settlement of all related claims.

Form components explained

- Parties involved: Identification of the releasor and releasee.

- Consideration: Indicates the amount paid to the releasor for the release.

- Claims being released: Specific mention of claims related to the fire and insurance policy cancellation.

- Non-admission of liability: Clear statement that the releasee does not admit to any liability.

- Complete settlement: Acknowledgment that this document settles all claims permanently.

- Notary section: Certification by a notary public to validate the execution of the release.

Common use cases

This form should be utilized when a party (the releasor) wants to release another party (the releasee) from any further claims related to damages or liabilities arising from a specific event, such as a fire incident and its implications on insurance. It is commonly used in settlements where both parties aim to conclude any further disputes.

Intended users of this form

- Individuals or entities that have experienced a fire and are settling claims with an insurance provider.

- Policyholders seeking to formally waive their right to pursue further claims related to a fire.

- Attorneys representing clients in the settlement process of such claims.

- Parties involved in litigation regarding insurance coverage disputes.

How to prepare this document

- Identify the parties by filling in the names of the releasor and releasee.

- Specify the consideration amount, which is the sum paid for the release.

- Detail the claims being released related to the fire and insurance policy.

- Ensure all parties agree to the terms, confirming there are no additional agreements outside this document.

- Sign and date the release, then have it notarized to ensure its legal validity.

Notarization guidance

Notarization is required for this form to take effect. Our online notarization service, powered by Notarize, lets you verify and sign documents remotely through an encrypted video session, available 24/7.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Common mistakes

- Failing to fully identify all parties involved in the agreement.

- Neglecting to specify the consideration amount, leading to ambiguity.

- Omitting required signatures or not having the document notarized.

- Not clearly stating all claims being released, which can cause future disputes.

Why use this form online

- Convenience of downloading and filling out the form from anywhere, at any time.

- Editability to ensure all information is accurate before finalizing.

- Instant access to professionally drafted templates created by licensed attorneys.

- Time-saving compared to seeking legal assistance for drafting from scratch.

Looking for another form?

Form popularity

FAQ

Most cases settle out of court before proceeding to trial. Some say that the measure of a good settlement is when both parties walk away from the settlement unhappy.This means that the defendant paid more than he wanted to pay, and the plaintiff accepted less than he wanted to accept.

If a debtor makes a written or verbal statement saying that they are making payment to you in full and final settlement of the debt, or words to that effect, and that payment is less than the debt owed, care needs to be taken as you could inadvertently lose your legal right to pursue the balance of the debt.

Full and final settlement means that you ask your creditors to let you pay a lump sum instead of the full balance you owe on the debt. In return for having a lump-sum payment, the creditor agrees to write off the rest of the debt.

By contrast, a payment "in full and final settlement" can usually be interpreted as an offer to settle a dispute on terms that, in exchange for the sum tendered, the creditor will give up the rest of its claim.

Depending on your case, it can take from 1 6 weeks to receive your money after your case has been settled. This is due to many factors but below outlines the basic process. If you have been awarded a large sum, it may come in the form of periodic payments. These periodic payments are called a structured settlement.

With that being said, studies have found that most settlement amounts total between $2,000 and $20,000.

What percentage should I offer a full and final settlement? It depends on what you can afford, but you should offer equal amounts to each creditor as a full and final settlement. For example, if the lump sum you have is 75% of your total debt, you should offer each creditor 75% of the amount you owe them.

Payment for non-availed leaves (earned or privilege leave), which is calculated as the number of days of non-availed leaves multiplied by basic salary divided by 26 days (paid days in a month).

How Is a Settlement Paid Out? Compensation for a personal injury can be paid out as a single lump sum or as a series of periodic payments in the form of a structured settlement. Structured settlement annuities can be tailored to meet individual needs, but once agreed upon, the terms cannot be changed.