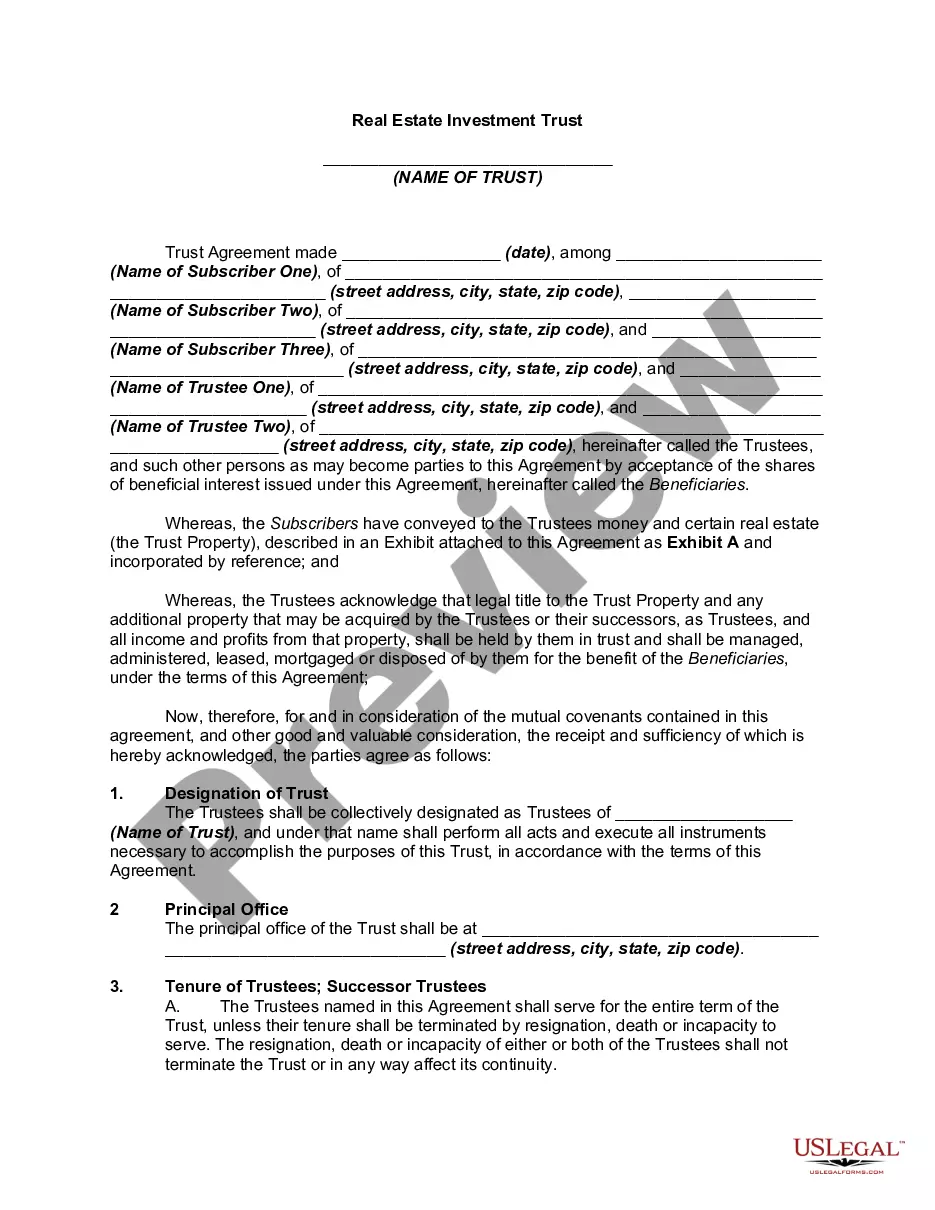

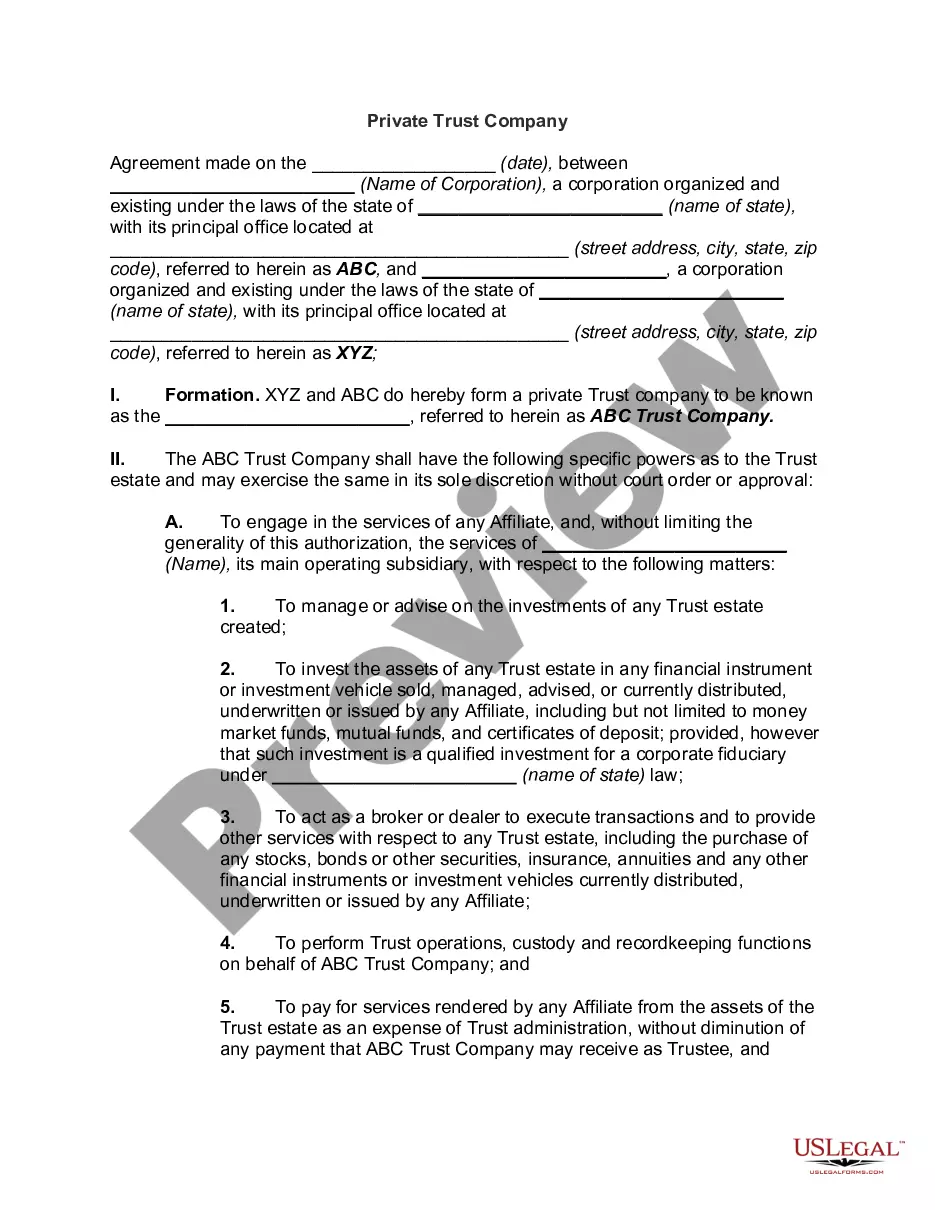

Business Trust

Overview of this form

The Business Trust form is a legal document used to establish a business trust, which is a type of business organization similar to a corporation. In a business trust, investors receive transferable certificates of beneficial interest, while the appointed trustees manage the trust for the benefit of its beneficiaries. This form provides a framework for organizing the trust and outlines the rights and responsibilities of both trustees and shareholders, differing it from other organizational forms like partnerships or limited liability companies.

What’s included in this form

- Names and addresses of the trustees managing the business trust.

- Declaration of trust property and any assets included.

- Specification of capital stock and shares, including contributions and distributions.

- Transfer procedures for shares among shareholders.

- Rights and liabilities of shareholders regarding the trust management.

- Provisions for meetings of trustees and shareholders to discuss trust affairs.

When to use this document

This Business Trust form should be used when setting up a new business trust or when existing trust documents require formalization. It's particularly useful for entrepreneurs looking to create an entity that allows for the management of assets by trustees on behalf of beneficiaries while maintaining limited liability for the shareholders. This form is ideal for situations involving multiple investors or parties looking to share profits while safeguarding personal assets.

Who this form is for

- Individuals looking to establish a business trust for investment purposes.

- Business owners seeking to manage risk and separate personal liabilities.

- Investors or groups of individuals interested in pooling resources to manage and profit from shared investments.

- Trustees who need a clear framework for managing a business trust's affairs.

Steps to complete this form

- Identify the names and addresses of the trustees who will manage the trust.

- Define the property or assets that will be included in the trust by referencing Exhibit A.

- Designate a business name for the trust and its principal office location.

- Determine the amount of capital contributions and specify the shares to be issued.

- Include clauses on the transfer of shares and rights of the shareholders, ensuring clear governance.

Does this document require notarization?

This form does not typically require notarization unless specified by local law. However, it's always advisable to consult with a legal professional familiar with your jurisdiction to ensure compliance.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Mistakes to watch out for

- Failing to clearly define the trust's property or assets in Exhibit A.

- Neglecting to specify quorum requirements for meetings.

- Omitting the proper endorsement of capital contributions and share allocations.

- Not updating the form if the trustees or significant agreements change.

Advantages of online completion

- Convenience of completing the form in a digital format from any location.

- Editability allows easy adjustments to meet specific needs.

- Access to legal form templates created by licensed attorneys enhances reliability.

Looking for another form?

Form popularity

FAQ

An example of business trust assets might include stocks, cash, real estate, ownership in a company, or items of value. Depending on the terms in the declaration of trust, the trustees may have the rights to sell existing property, buy additional property, or try to expand the assets through business.

The Business Dictionary defines a trust as a "legal entity created by a party (the trustor) through which a second party (the trustee) holds the right to manage the trustor's assets or property for the benefit of a third party (the beneficiary)." Basically, a trust is a financial arrangement between three parties that

Business trusts, also known as common law trusts, are legal instruments that give a trustee the authority to manage a beneficiary's interest in a business. A business trust can be used as the legal entity that runs the business.

Some of the larger trust companies are Northern Trust, Bessemer Trust, and U.S. Trust, which is now part of Bank of America Corporation.

A business trust is defined as a trust where the trustee uses the trust assets to do business for profit in order to benefit the trust beneficiary or to further the aims of the trust.The trust protects your assets against personal creditors, because the assets of the trust belong to the trust alone.

A business trust is set up when the assets and property of a business corporation are entrusted to an appointed trustee. The trustees will manage the operation and assets of the business, not for their own profit, but for the profit of the beneficiaries.

Among the chief advantages of trusts, they let you: Put conditions on how and when your assets are distributed after you die; Reduce estate and gift taxes; Distribute assets to heirs efficiently without the cost, delay and publicity of probate court.