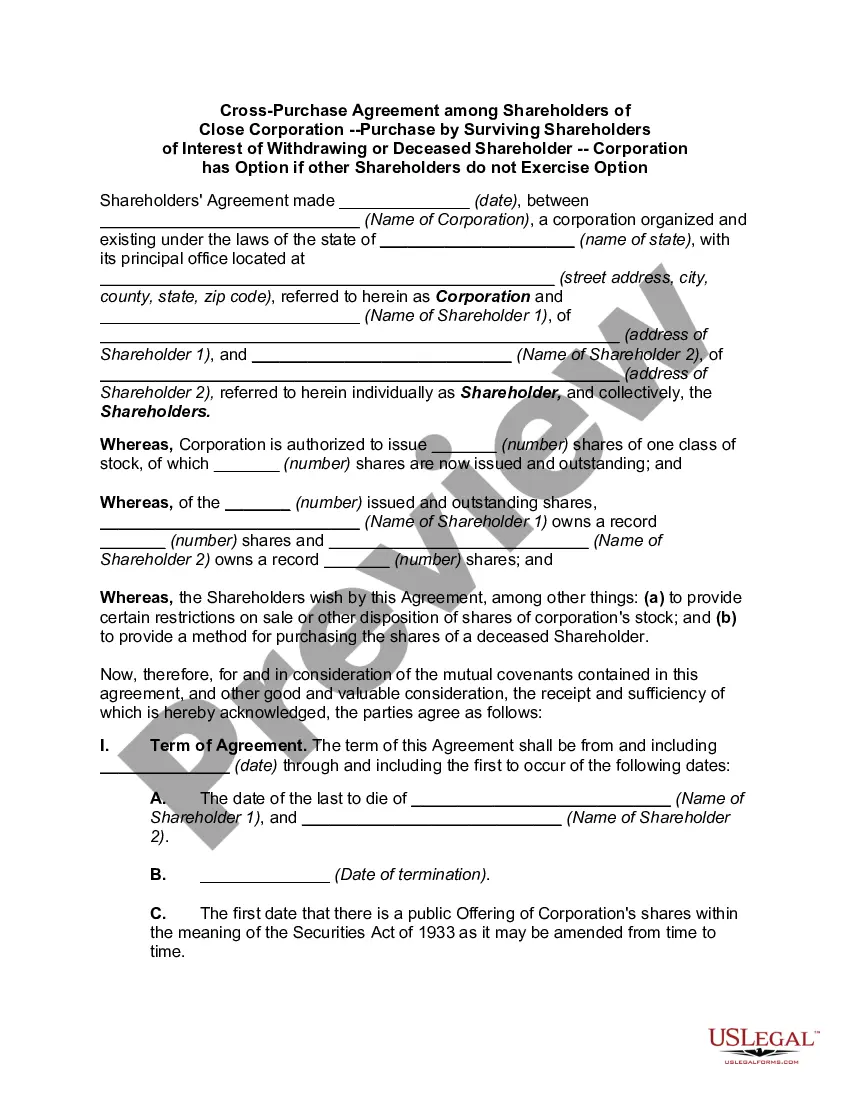

Corporate Cross Purchase Agreement

Understanding this form

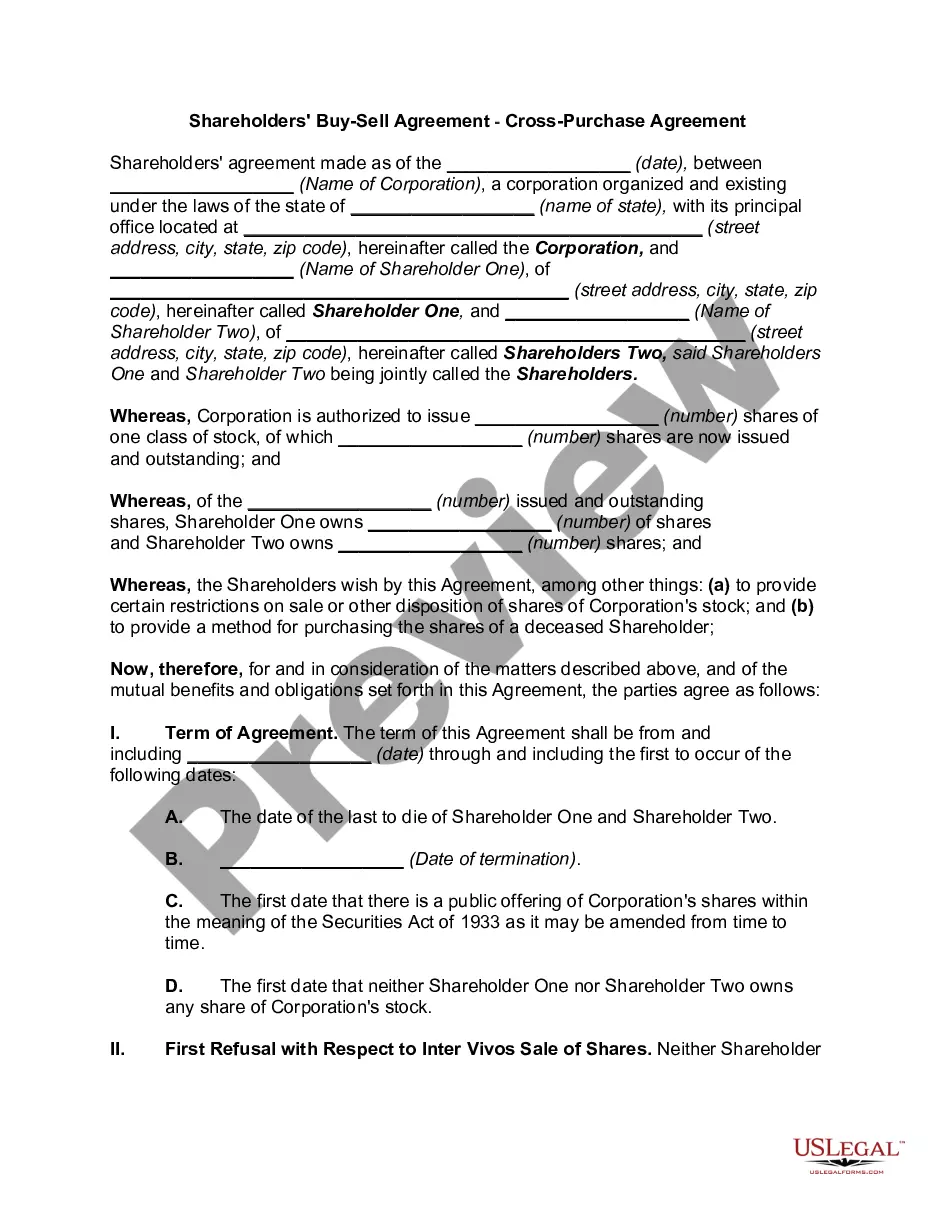

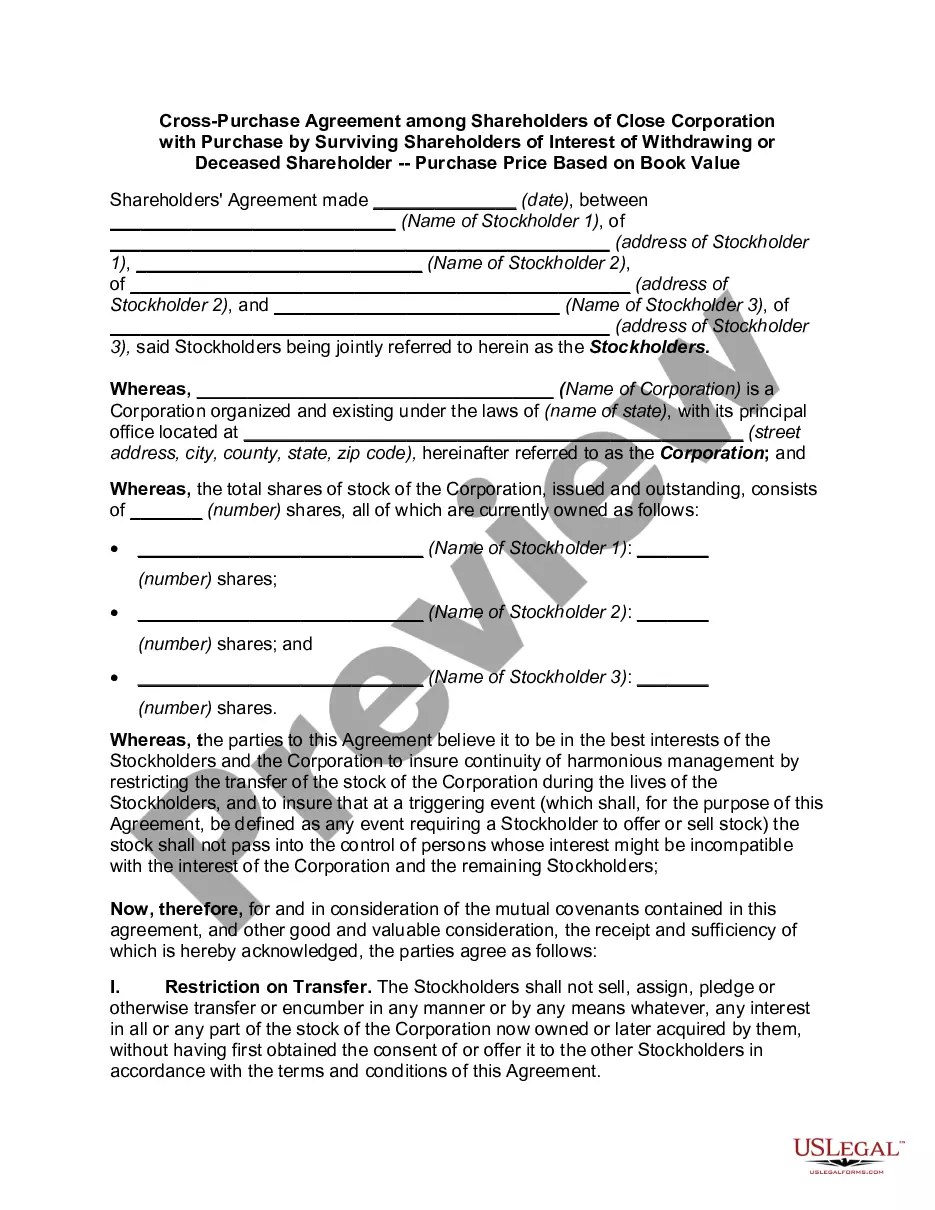

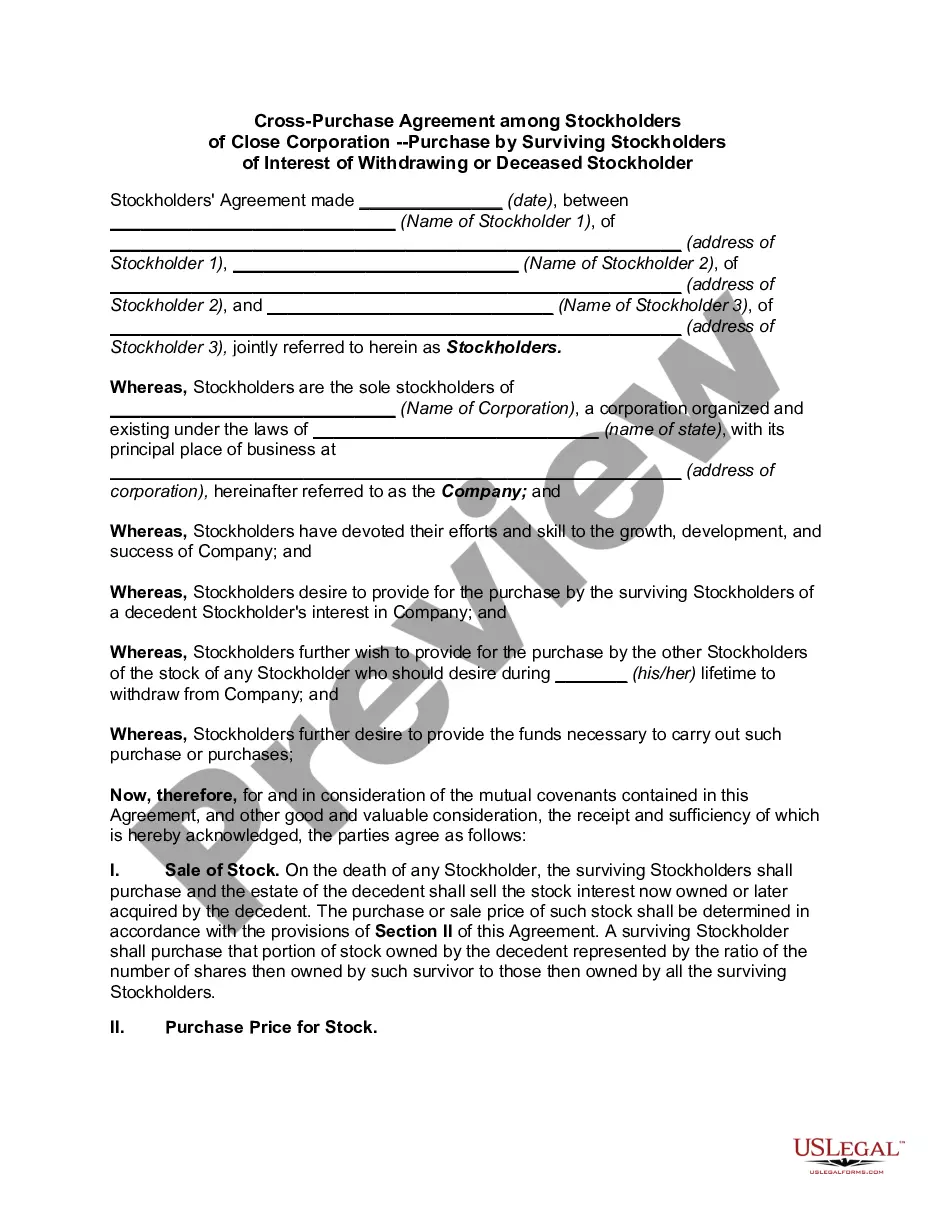

A Corporate Cross Purchase Agreement is a legal document used by business owners to outline how ownership in a corporation is transferred in the event of death, retirement, or disability of a shareholder. Unlike other buy-sell agreements, this type specifically involves a seller and a buyer among existing shareholders, ensuring that business interests are fairly priced and transferred smoothly. The agreement not only sets the terms for this transfer but also often provides for securing funding through insurance for a smoother transaction process.

What’s included in this form

- Restriction on stock transfer to prevent unauthorized sales.

- Sale procedures during a shareholderâs lifetime, including notification requirements.

- Terms for stock sale upon a shareholder's death or disability.

- Valuation methods to determine the fair market value of shares.

- Life insurance provisions to fund buyouts when necessary.

When to use this form

This form is necessary when shareholders want to ensure their business interests are handled effectively during life transitions such as death, retirement, or disability. It is typically used by closely held corporations where continuity of ownership is critical for ongoing operations. If a shareholder plans for their exit or the potential risk of a shareholder becoming unable to continue their role, this agreement helps stipulate who will buy out their shares and at what price.

Intended users of this form

This form is suitable for:

- Business owners in a partnership or close corporation with multiple shareholders.

- Shareholders who want to establish clear terms for the buyout of shares in critical life events.

- Corporations wanting to secure financial stability through structured buy-sell agreements.

Steps to complete this form

- Identify and list the shareholders involved, including their names and addresses.

- Detail the corporation's information, including its name and registered address.

- Specify the total shares and the ownership percentage of each shareholder.

- Include provisions for the sale of shares in the event of death, disability, or retirement.

- Outline insurance coverage and payment terms to secure the buyout process.

Does this document require notarization?

This form does not typically require notarization unless specified by local law. However, getting the agreement notarized can help ensure its enforceability and may be a good practice to establish strong legal standing.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Typical mistakes to avoid

- Failing to regularly update the agreement to reflect changes in ownership or business structure.

- Not specifying a clear method for the valuation of shares.

- Overlooking the need for insurance provisions to fund the buyout effectively.

Benefits of completing this form online

- Immediate access to a professionally drafted agreement tailored for your needs.

- Editable fields allow customization to fit your specific situation and business structure.

- Secure storage and retrieval of your completed documents for future use.

Looking for another form?

Form popularity

FAQ

The main disadvantages of the cross-purchase plan are the complications that arise because each owner has to buy and manage a policy for each of their partners. The estate of the deceased owner benefits from a tax advantage with an entity purchase plan.

purchase agreement is a document that allows a company's partners or other shareholders to purchase the interest or shares of a partner who dies, becomes incapacitated or retires. The mechanism often relies on a life insurance policy in the event of a death to facilitate that exchange of value.

In a cross purchase buy-sell agreement, each business owner buys a life insurance policy on the other owner(s). With multiple owners, this can get very complex and complicated. Instead, try a trusteed cross purchase buy-sell, in which a third-party (acting as trustee) takes care of the buy-sell arrangement.

Advantages of a Cross Purchase Agreement A cross purchase agreement allows a smooth transition of ownership from departing partners or shareholders to others in the company. The transfer of ownership through the proceeds from life insurance is not subject to income tax.

The main disadvantages of the cross-purchase plan are the complications that arise because each owner has to buy and manage a policy for each of their partners. The estate of the deceased owner benefits from a tax advantage with an entity purchase plan.

With a redemption plan, the business enters into a contract with the owners to purchase each owner's interest at a specified time. In the cross- purchase arrangement, the owners establish an agreement among themselves to buy and sell the stock. The business entity is not a party to the arrangement.

The surviving owners have a better tax consequence from the cross purchase plan than the entity purchase plan in their own future exit. When the owner(s) purchase the business interest of their departed or deceased owner, their basis increases by what they pay to the exiting owner or estate of the deceased owner.

Example: Alma owns 60%, Betty 20% and Catherine 20% of their company. The cross-purchase agreement states that if one owner dies, her interest is divided equally between the survivors. Therefore, if Betty dies, Alma's ownership interest grows from 60% to 70%, while Catherine's interest grows from 20% to 30%.