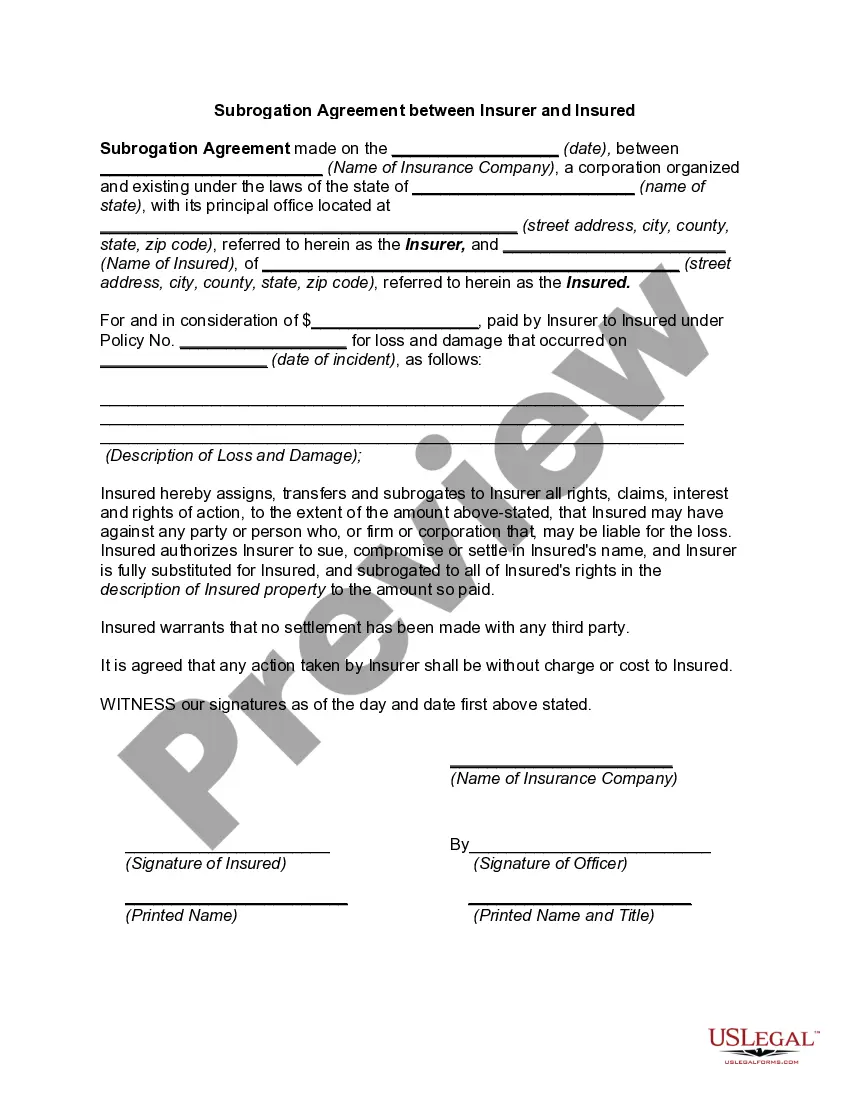

Subrogation Agreement Authorizing Insurer to Bring Action in Insured's Name

Understanding this form

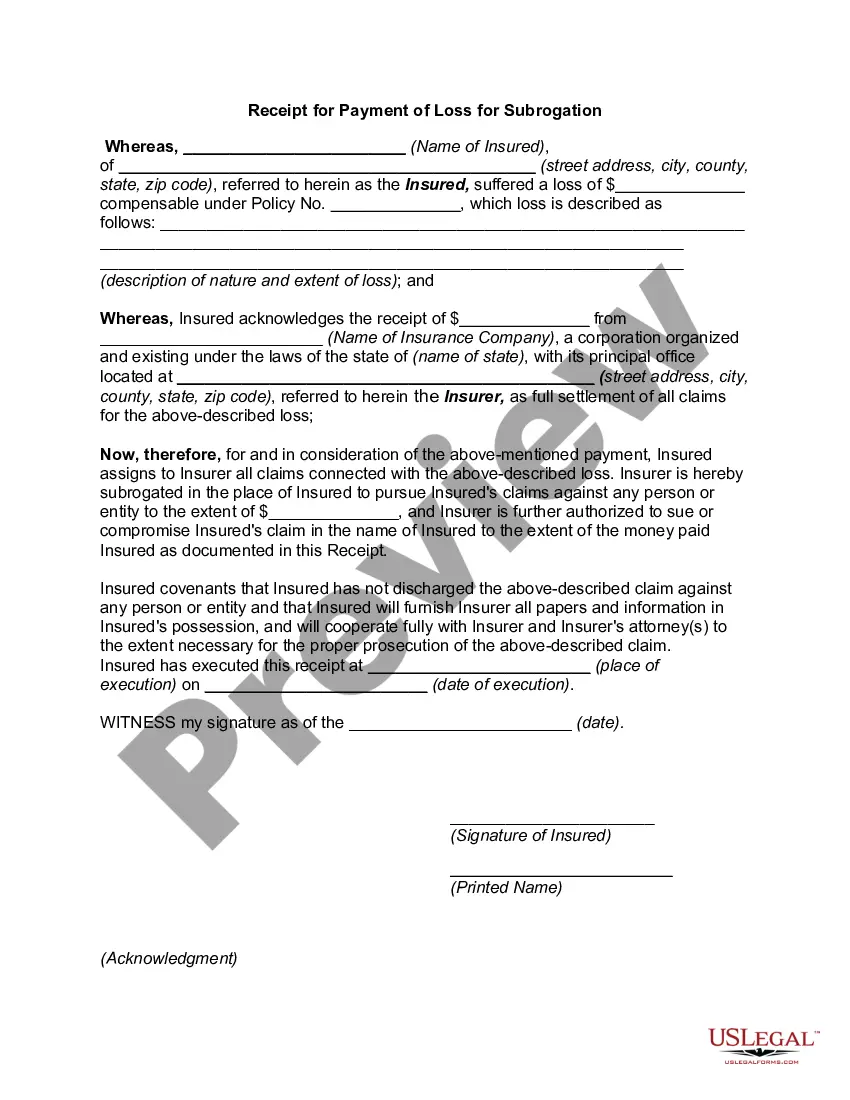

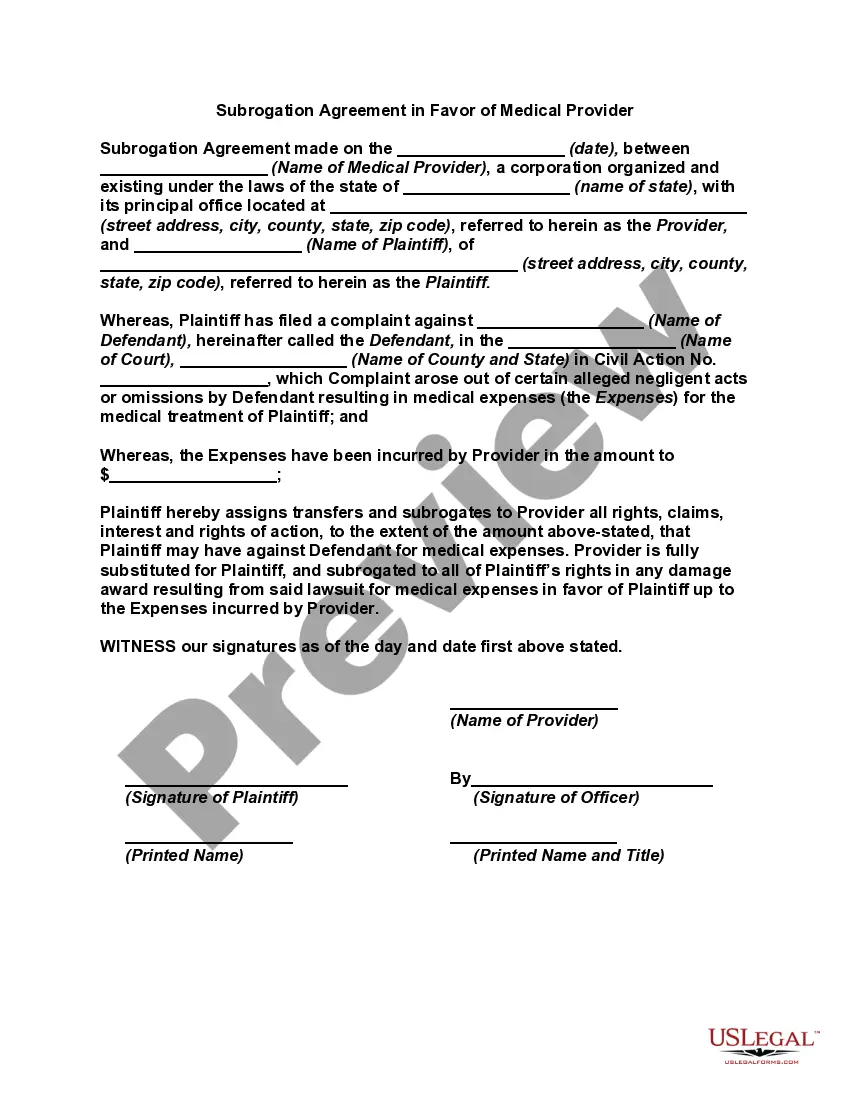

The Subrogation Agreement Authorizing Insurer to Bring Action in Insured's Name is a legal document that allows an insurance company (the Insurer) to step into the shoes of the insured individual (the Insured) to pursue recovery from a third party responsible for a loss. This form is essential in insurance matters, especially after the insurer has compensated the insured for a covered loss. By signing this agreement, the insured authorizes the insurer to act on their behalf, making it possible for the insurer to recover costs from the at-fault party.

Main sections of this form

- Parties Involved: Identification of the insurer and the insured, including their names and addresses.

- Assignment of Claim: Transfer of the insured's rights to the insurer to pursue compensation from a liable third party.

- Prosecution of Claim: Stipulations regarding how the claim will be prosecuted and that the insurer will cover all related expenses.

- Trust Fund Provision: Any recovery is to be held as trust funds to be repaid to the insurer.

- Signatures: Required signatures of the parties involved, ensuring legal validation of the agreement.

Situations where this form applies

This form should be used when an insured individual has suffered a loss due to the actions of a third party and has received compensation from their insurer. It is necessary in situations where the insurer needs to recover these costs by pursuing legal action against the party responsible for the loss. Examples include auto accidents, property damage, or situations involving liability claims.

Who this form is for

- Individuals who have an active insurance policy and have experienced a loss due to another party's negligence.

- Insurance companies seeking a formal agreement to recover costs from a third party.

- Legal professionals representing either the insurer or the insured in subrogation matters.

How to prepare this document

- Identify the parties: Fill in the names and addresses of both the insurer and the insured.

- Specify the insurance policy: Enter the policy number and the date of the incident.

- Detail the claim: Clearly state the nature of the claim and the third party involved.

- Enter payment details: Include the sum to be paid to the insured upon execution of the agreement.

- Obtain signatures: Ensure that both the insurer's representative and the insured sign the document with printed names and titles.

Is notarization required?

This form does not typically require notarization unless specified by local law. It is always advisable to check local regulations to ensure compliance.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Common mistakes

- Failing to include all necessary identification information for both parties.

- Not specifying the exact amount to be paid to the insured.

- Inadequately detailing the claim and the circumstances surrounding the loss.

- Neglecting to sign and date the agreement properly.

- Overlooking the need for a clear understanding of legal obligations regarding the prosecution of the claim.

Advantages of online completion

- Convenient access from anywhere, allowing users to fill out and download the form at their own pace.

- Editability of the document ensures that all necessary details can be adjusted before finalization.

- Reliability in having a form drafted by legal experts, which helps avoid common pitfalls.

- Secure storage of completed forms for easy retrieval in the future if needed.

Legal use & context

- This agreement allows insurers to pursue claims while protecting the rights of the insured.

- Subrogation rights can vary by state, impacting the actions an insurer can legally take.

- Ensure that the terms of the agreement do not infringe on any rights of the insured as per state law.

Quick recap

- A subrogation agreement allows insurers to recover costs from third parties on behalf of their insured clients.

- The form is essential for clarifying responsibilities and rights between the insurer and the insured.

- Proper completion and understanding of this agreement are critical to ensuring legal compliance and effective claim recovery.

Looking for another form?

Form popularity

FAQ

Letter creation date. The name of the insured and the name of the at-fault party. The sum paid to the insured. Summary of the damages. Request for the policy number of the recipient. Request to contact the insurance company and contact details.

Subrogation is the assumption by a third party (such as a second creditor or an insurance company) of another party's legal right to collect a debt or damages.A right of subrogation typically arises by operation of law, but can also arise by statute or by agreement.

By negotiating down the subrogation lien and convincing the hospital to accept only one or two-thirds (or even less) of that amount, an attorney could save the plaintiff a lot of money. A plaintiff who has received a subrogation letter should find a personal injury attorney who can speak on their behalf.

Under the principle of subrogation the insurer can assume the rights of the insured in order to recover from a third party the loss paid under a policy.

What Is the Principle of Subrogation in Insurance.To make up for the compensation paid, your insurer can claim the (insured) right over that third party. You surrender your rights over the third party to the insurer. This transfer of all the rights, and remedies, from insured to insurer is called subrogation.

A Waiver of Subrogation is an endorsement that prohibits an insurance carrier from recovering the money they paid on a claim from a negligent third party. An Owner Client may require this endorsement from their vendors to avoid being held liable for claims that occur on their jobsite.

An insurance company may not subrogate against its own insured or a co-insured. However, when a party claiming to be a co-insured is merely a loss payee to which no liability coverage is afforded, subrogation is permissible.