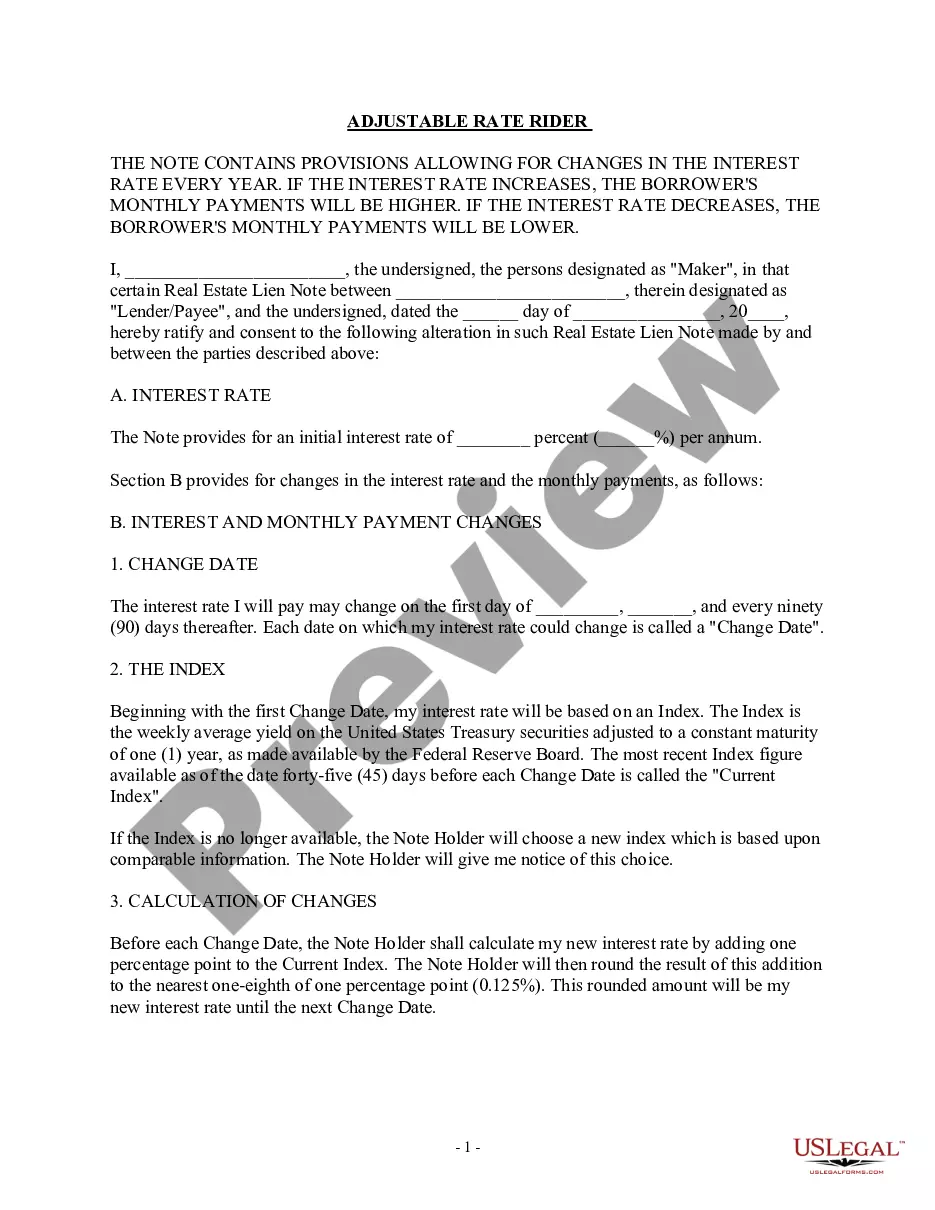

Model Adjustable Rate Note - Home Equity Conversion

What this document covers

The Model Adjustable Rate Note for Home Equity Conversion is a legally binding document that outlines the terms under which a borrower agrees to repay a loan secured by the equity of their home. Unlike fixed-rate notes, this adjustable rate note allows for the interest rate to change periodically based on market conditions. This flexibility enables borrowers to benefit from lower payments when interest rates decrease, while also accounting for potential increases in their payments if the rates rise.

Key parts of this document

- Definitions of key terms such as "Borrower" and "Lender."

- Borrower's promise to repay the loan amount with interest, including conditions for interest rate changes.

- Secured payment promises through a mortgage or deed of trust.

- Details on the manner of payment and limitations of Borrower's personal liability.

- Provisions for interest rate changes and notification requirements.

- Borrower's rights regarding prepayment of the loan.

When to use this form

This form is required when a homeowner wishes to access the equity in their property through a Home Equity Conversion loan. It is suitable for seniors seeking to convert cash from their home equity while retaining ownership of their property. Use this form to create a structured agreement that outlines repayment terms, conditions for interest rate adjustments, and rights regarding prepayment or full repayment.

Who can use this document

- Homeowners over the age of sixty-two applying for a Home Equity Conversion loan.

- Borrowers looking to manage fluctuating monthly payments tied to market interest rates.

- Individuals seeking to withdraw cash from their home equity while maintaining their home as their primary residence.

Instructions for completing this form

- Fill in the date and the address of the property securing the loan.

- Define the interest rate and the index it is based on for potential adjustments.

- Include borrower's details, ensuring all parties sign at the end of the note.

- Specify the place where payments will be made, under the terms defined in the agreement.

- Review and confirm all fields for accuracy before finalizing and signing the document.

Notarization guidance

This form does not typically require notarization unless specified by local law. However, it is advisable to check local regulations to confirm if notarization is necessary to enhance the validity of the document.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Common mistakes

- Failing to understand the implications of an adjustable interest rate and its potential impact on payments.

- Not providing accurate property address information.

- Overlooking the requirement of signatures from all borrowers involved.

- Ignoring state-specific modifications that might be required for compliance.

Why complete this form online

- Convenience of completing the form from home without needing to visit a lawyer.

- Editability to customize terms according to the borrower's specific needs.

- Access to templates drafted by licensed attorneys, ensuring legal compliance.

- Ability to download and print for record-keeping and formal filing.

Looking for another form?

Form popularity

FAQ

Overall, Suze's opinion on reverse mortgages is that they should be a last resort for older Americans who need extra income. She recommends exploring other options first, such as downsizing to a smaller home or taking out a home equity line of credit.

THIS NOTE CONTAINS PROVISIONS ALLOWING FOR CHANGES IN MY INTEREST RATE AND MY MONTHLY PAYMENT. THIS NOTE LIMITS THE AMOUNT MY INTEREST RATE CAN CHANGE AT ANY ONE TIME AND THE MAXIMUM RATE I MUST PAY.

Key Differences Between Reverse Mortgages and HECMs Reverse mortgages are available to consumers who are 55 and older in most states while HECMs are only available if you are 62 or older. HECMs also have more flexibility in their payout options while reverse mortgages only offer a single-lump sum in most cases.

Some of the potential disadvantages of getting a HECM include: You have to live in your home: When you get a HECM, your property must be your principal residence for much of the year. You'll have to pay back the HECM if you sell the home or want to move.

Does AARP recommend reverse mortgages? AARP does not recommend for or against reverse mortgages. They do however recommend that borrowers take the time to become educated so that borrowers are doing what is right for their circumstances.

While a reverse mortgage lets you access your equity without selling your house right away, it can be financially risky: A reverse mortgage increases your debt and can use up your equity. While the amount is based on your equity, you're still borrowing the money and paying the lender a fee and interest.

After a set period of time, often 1 ? 5 years, you'll have the option to convert your ARM loan into a conventional fixed-rate loan. In other words, you'll be able to settle into a single rate for the remaining life of your loan. While you won't pay closing costs on your conversion, there is generally an associated fee.

Reverse mortgages are ideal for retirees who don't have a lot of cash savings or investments but do have a lot of wealth built up in their homes. A reverse mortgage allows you to turn an otherwise illiquid asset into cash that you can use to cover expenses in retirement.