Adjustable Rate Rider - Variable Rate Note

What this document covers

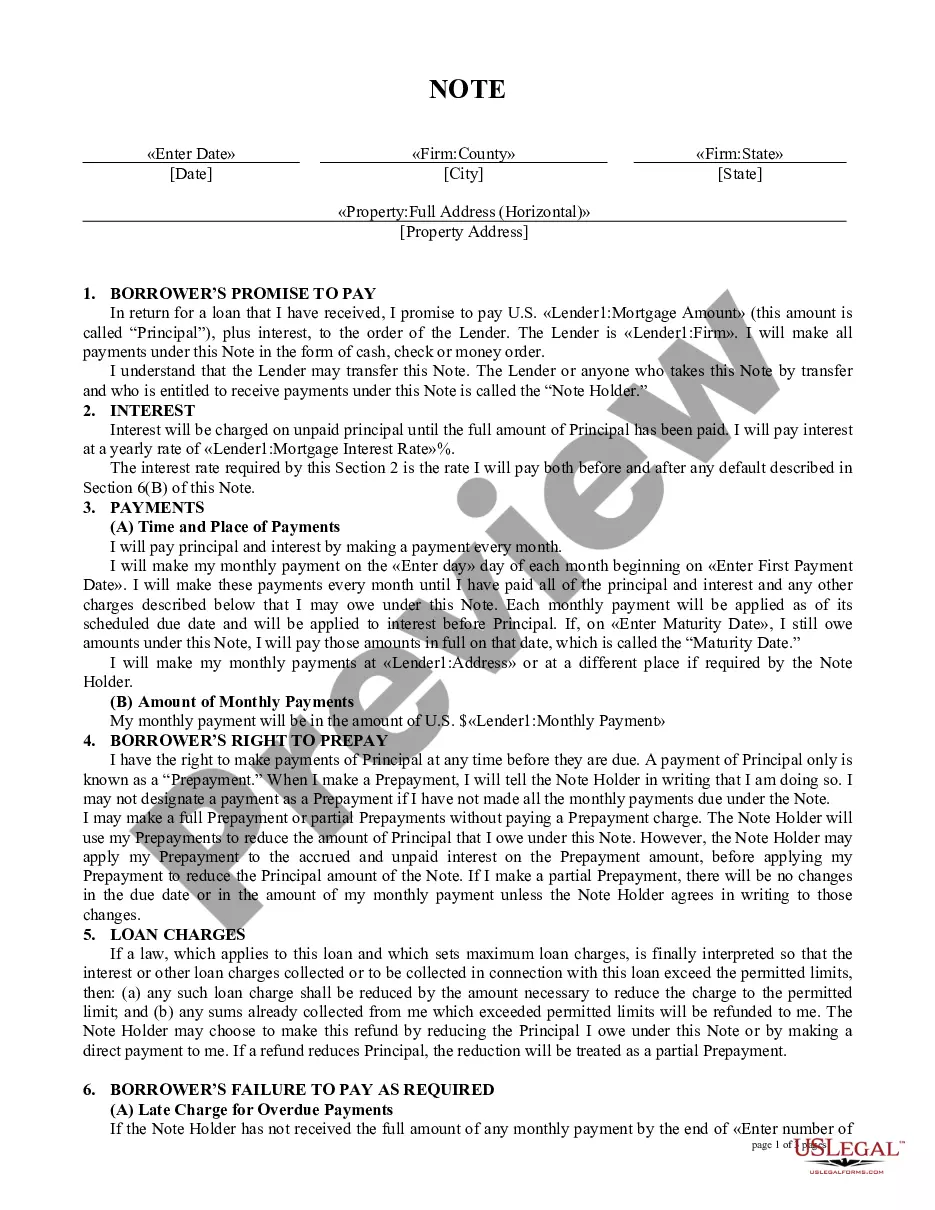

The Adjustable Rate Rider - Variable Rate Note is a legal document that includes provisions for changes in interest rates on a loan every year. Unlike fixed-rate notes, this form allows borrowers to adjust their monthly payments based on fluctuations in interest rates. If rates rise, the borrower's payments increase; if rates fall, payments decrease. This form is essential for borrowers who prefer lower initial rates with the understanding that their payments may vary over time.

Form components explained

- Interest Rate: Specifies the initial interest rate of the loan.

- Change Date: Indicates when interest rate adjustments will occur, typically every ninety days.

- The Index: Describes how the new interest rate is determined based on a designated financial index.

- Calculation of Changes: Details the formula used to calculate new interest rates and monthly payments.

- Notice of Changes: Outlines the process for notifying the borrower of changes to payments.

- Maximum Rate: Sets a cap on the interest rate that can be charged over the loan's term.

When to use this document

This form is useful for homeowners or individuals taking out a loan with an adjustable interest rate. It is beneficial when you expect interest rates to decrease or want flexibility in payment amounts. You may find it necessary if you are refinancing an existing adjustable-rate loan or purchasing a new property with such financing terms.

Who this form is for

This form is intended for:

- Borrowers seeking an adjustable-rate loan.

- Homeowners refinancing into a variable rate note.

- Lenders who provide adjustable-rate mortgages and require a formal agreement on variable payments.

How to complete this form

- Identify the parties involved: Insert the names of the borrower and lender.

- Input the initial interest rate: Specify the starting interest rate in the designated field.

- Set the change date: Indicate the date when the first interest rate change will occur.

- Complete the index section: Provide details on the index being used for future rate adjustments.

- Enter the maximum interest rate: Fill in the highest interest rate allowable under the agreement.

- Sign and date the form: Ensure all parties sign and date to validate the agreement.

Is notarization required?

To make this form legally binding, it must be notarized. Our online notarization service, powered by Notarize, lets you verify and sign documents remotely through an encrypted video session.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Mistakes to watch out for

- Failing to specify the exact change dates for interest rates.

- Not accurately completing the index section, leading to confusion on rate changes.

- Leaving out signatures, which can invalidate the form.

- Overlooking the maximum rate cap, which may result in excessive charges.

Benefits of completing this form online

- Convenient access: Download and complete the form at your own pace and convenience.

- Editability: Easily modify the document as needed before finalizing it.

- Legal reliability: Access forms drafted by licensed attorneys to ensure compliance with legal standards.

Legal use & context

- Adjustable rate riders are legally enforceable in most jurisdictions if completed correctly.

- Understanding the terms of the agreement is crucial for both borrowers and lenders.

- Failure to comply with local laws may affect the validity of the note.

Summary of main points

- The Adjustable Rate Rider allows for flexible borrowing based on market conditions.

- Understanding the components of the form is essential for successful completion.

- Always stay informed about local regulations regarding adjustable-rate loans.

Looking for another form?

Form popularity

FAQ

The Adjustable Rate Rider - Variable Rate Note is a legal document that attaches to a loan to allow interest rates to change over time. It governs how often rates adjust (Change Date), what index determines the new rate (Index), how changes are calculated (Calculation of Changes), how you’re notified (Notice of Changes), and the loan cap (Maximum Rate). It’s used for borrowers seeking an adjustable-rate loan, refinancing into a variable-rate note, or lenders offering such mortgages.

In many contexts the terms are used interchangeably, but this form explicitly links the rate changes to an index and a defined Change Date. It also spells out how changes are calculated and when notices are issued, and it sets a Maximum Rate, giving practical, document-based distinctions from other loan forms.

An adjustable rate starts with an initial rate, then, on a Change Date typically every ninety days, the rate changes based on an Index plus a margin specified in the rider. The new rate drives the monthly payment calculation, and the loan may include a cap (Maximum Rate) to limit how high payments can rise.

The primary downside is payment variability: monthly payments can rise if interest rates increase and fall if rates drop. With this rider there is a defined Change Date and an Index for rate changes, plus a Maximum Rate cap. Borrowers should plan for possible increases and understand how the changes are calculated.

An adjustable rate note is a loan agreement where the interest rate may change over time based on an index. The Adjustable Rate Rider – Variable Rate Note provides the mechanics: how the rate changes are calculated, when they occur, how you’re notified, and the upper limit. It accompanies the actual note.

This form codifies rate changes tied to an index with a Change Date, and requires notices of payment changes and a Maximum Rate. A fixed-rate note keeps the same rate throughout the term, without indexed adjustments or payment fluctuation.