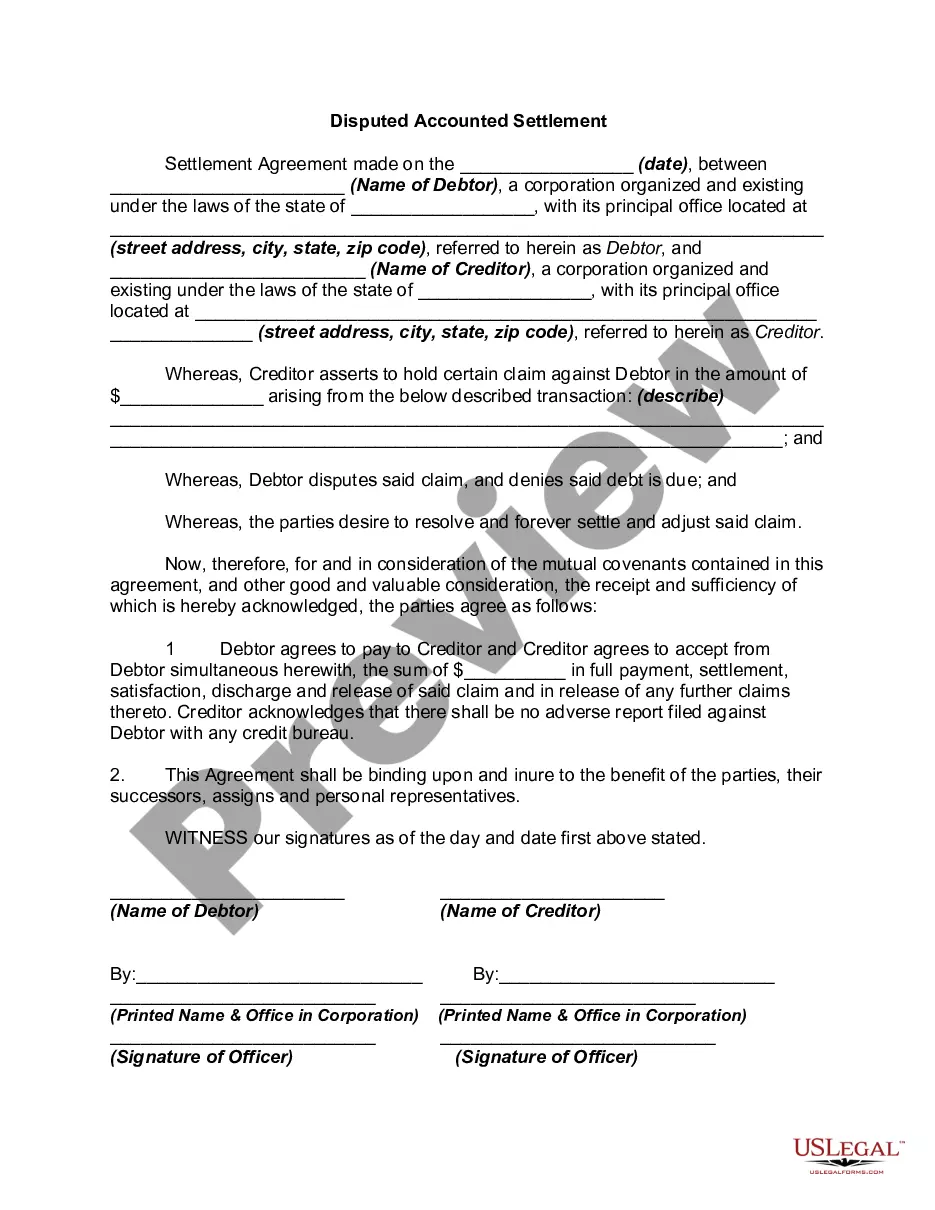

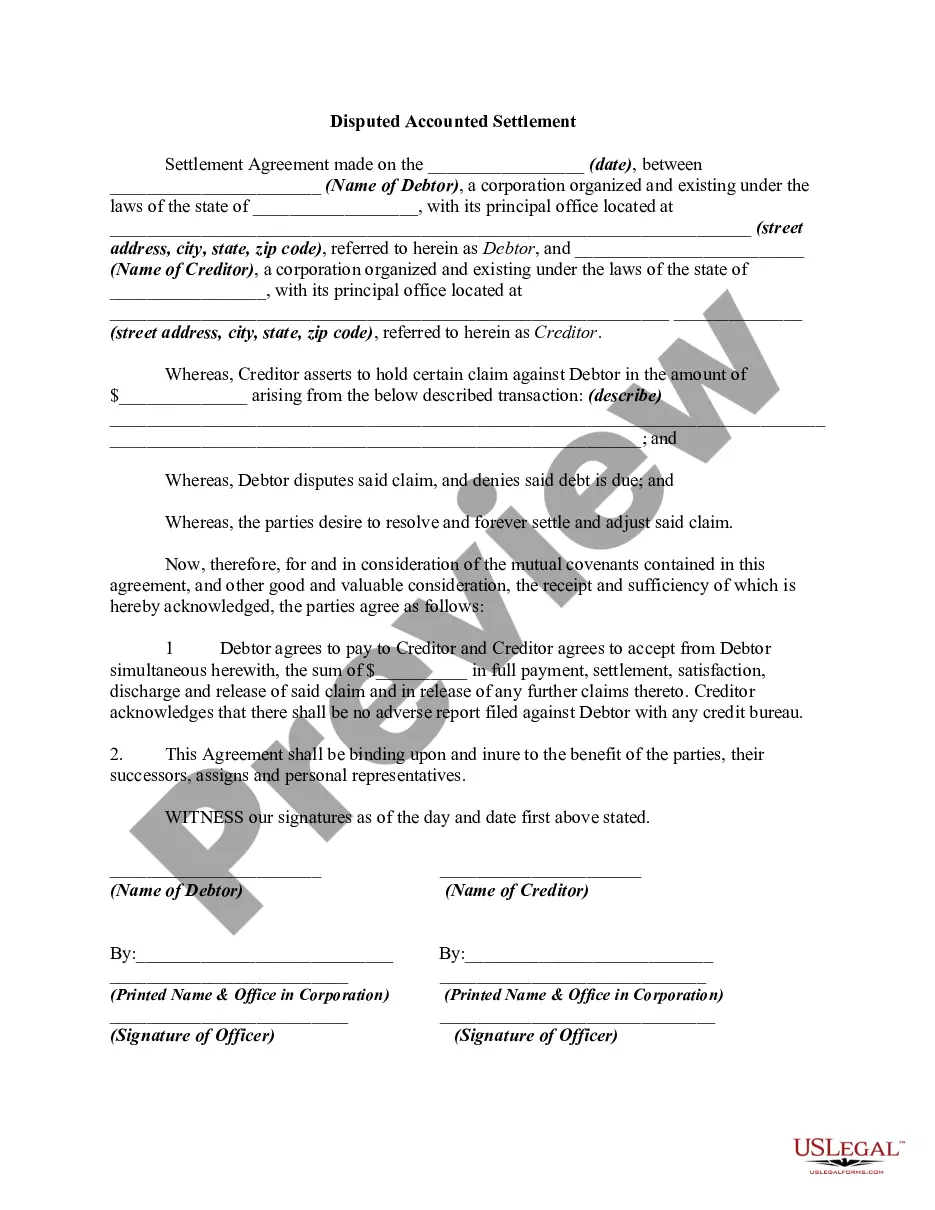

Disputed Open Account Settlement

Overview of this form

The Disputed Open Account Settlement form is a legal document used to resolve disputes between a debtor and creditor regarding claims or debts that are being contested. This form allows both parties to reach a mutual agreement to settle the disputed amount without further legal action. Unlike other types of settlement agreements, this specific form addresses open account disputes, which often involve ongoing transactions or credit extensions.

Key parts of this document

- Identification of Parties: The form requires the full names and addresses of both the creditor and debtor.

- Statement of the Dispute: A declaration that the debtor disputes the claim being made by the creditor.

- Settlement Terms: Specifies the agreed-upon settlement amount and the terms of payment.

- Release Clause: A clause stating that upon payment, the creditor releases the debtor from the disputed claim.

- Signatures and Witnesses: Spaces for the signatures of both parties along with witnesses to validate the agreement.

When to use this document

This form is typically used when a debtor and creditor disagree on the amount owed, but both parties wish to settle the matter out of court. It is particularly useful in situations where the debtor believes that the claimed debt is incorrect, yet both parties prefer to avoid lengthy legal proceedings. This form can help clarify terms and finalize the agreement efficiently.

Who can use this document

- Individuals or businesses acting as creditors seeking a resolution to a disputed claim.

- Debtors who wish to negotiate a settlement on a disputed account.

- Parties involved in ongoing credit relationships who need a documented agreement to maintain or restore business relations.

How to prepare this document

- Identify the parties by entering the names and addresses of the creditor and debtor at the top of the form.

- Clearly outline the disputed claim by detailing the amount in controversy and the nature of the transactions involved.

- Specify the agreed settlement amount that the debtor will pay to resolve the dispute.

- Both parties should date the agreement and provide their signatures in the designated areas.

- Include the signatures of any witnesses to validate the agreement.

Notarization requirements for this form

This form does not typically require notarization to be legally valid. However, some jurisdictions or document types may still require it. US Legal Forms provides secure online notarization powered by Notarize, available 24/7 for added convenience.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Mistakes to watch out for

- Failing to accurately identify the parties involved, which can lead to disputes about the agreement's validity.

- Not providing a clear description of the disputed claim and transaction history.

- Omitting signatures from both parties and any required witnesses, which can render the agreement unenforceable.

Benefits of using this form online

- Convenient access to legal documentation that can be downloaded instantly.

- Editable templates that can be customized to meet individual needs.

- Reliability of forms drafted by licensed attorneys, ensuring legal compliance.

Looking for another form?

Form popularity

FAQ

If the closed account includes negative information that's older than seven years, you can use the credit report dispute process to remove the account from your credit report.

If you have a poor and/or thin credit history, it could take 12 to 24 months from the time you settled your last debt for your credit score to recover. Either way, you'll benefit from debt settlement if that means you're no longer missing payments.

Monitor your credit report. As you begin to settle your debts, keep an eye on your credit report. Apply for new credit. Become an authorized user. Pay your bills on time and in full. Get a small loan.

Once an account has been settled or defaults it will remain on your report for six years from the date the debt was settled, written off or defaulted, whichever happened first. Live accounts will remain on your Equifax Credit Report indefinitely.

Yes, settling a debt instead of paying the full amount can affect your credit scores.Settling an account instead of paying it in full is considered negative because the creditor agreed to take a loss in accepting less than what it was owed.

Yes, settling a debt instead of paying the full amount can affect your credit scores.Settling an account instead of paying it in full is considered negative because the creditor agreed to take a loss in accepting less than what it was owed.

Try asking for pay for delete As a part of your debt settlement negotiation, you can request your creditor to remove the settlement account deleted from your report. You can suggest this in exchange by upping the amount you're offering to pay.

After finding a way to pay in full or at least some, the lender should remove the account from your credit report. Keep in mind the negative effects of the account will be removed since it is considered to be paid, but the ragged payment history will still be available on your account.

A settled account remains on your credit report for seven years from its original delinquency date.