Request for Extension of Loan Closing Date

Understanding this form

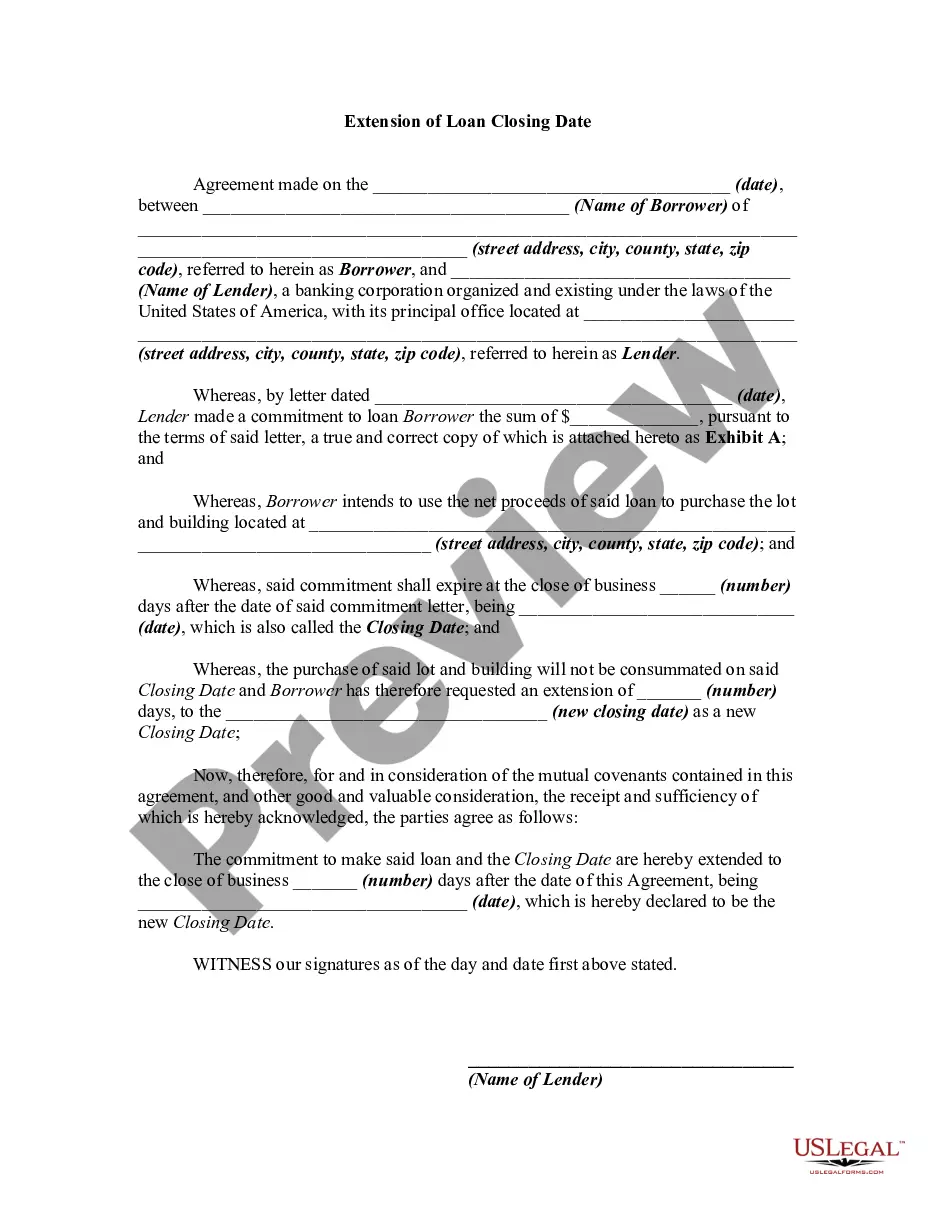

The Request for Extension of Loan Closing Date is a legal document used by loan applicants to request additional time to finalize the closing of a real estate transaction. This form differs from standard loan agreements by specifically addressing the need for an extension of the closing date, ensuring that applicants can secure their loan and property without losing their deposit or incurring penalties for late closure.

Key parts of this document

- Property address: Detailed information about the property involved in the loan.

- Loan number: Identification of the specific loan for which the extension is requested.

- Original closing date: The date initially agreed upon for the loan's closing.

- Request for extension duration: The number of additional days requested for closing.

- Extension fee: The amount included as a certified check or money order as part of the request.

- Supporting documentation: A checklist of required documents to justify the extension request.

Common use cases

This form should be used when loan applicants are unable to meet the originally scheduled closing date due to unforeseen circumstances, such as delays in obtaining financing, completion of inspections, or issues in the property title. It is a proactive measure to ensure that the transaction can proceed smoothly without jeopardizing the purchase or incurring unnecessary costs.

Who can use this document

- Homebuyers who need extra time to close on their property.

- Individuals or entities applying for a mortgage or loan secured by real estate.

- Real estate agents and brokers assisting clients with closing processes.

Completing this form step by step

- Identify the property: Fill in the complete address of the real estate involved in the transaction.

- Enter loan details: Provide the loan number and the date of application for the loan.

- Specify the original closing date: Indicate the date that closing was initially scheduled.

- State the requested extension: Write the number of additional days sought for the closing.

- Include payment: Attach the certified check or money order for the extension fee.

- Attach supporting documents: Ensure all required documents are included for a successful request.

Does this document require notarization?

Notarization is not commonly needed for this form. However, certain documents or local rules may make it necessary. Our notarization service, powered by Notarize, allows you to finalize it securely online anytime, day or night.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Mistakes to watch out for

- Failing to provide accurate property address details.

- Not including the required supporting documentation.

- Missing the loan number or application date.

- Omitting the extension fee payment.

Benefits of using this form online

- Convenient access to fill out and download the form anytime.

- Editable fields allow users to customize the form according to their specific situation.

- Reliable templates drafted by licensed attorneys ensure compliance with legal standards.

Key takeaways

- The Request for Extension of Loan Closing Date allows borrowers to formally request extra time for closing.

- It is crucial to provide all necessary documentation and follow proper procedures to avoid delays.

- Using this form online simplifies the process and ensures that all requirements are met efficiently.

Looking for another form?

Form popularity

FAQ

When the closing date was originally determined and the contract signed by both parties, that contract is binding. When the buyer misses the closing date, the seller has the right to terminate the contract and re-list the house for sale or contact other parties who had previously made offers on the property.

If your lender delays closing, you have two options: Do nothing. Request to cancel escrow or serve a Notice to Perform.

Depending on your purchase contract and whose fault the delay is, you may have to pay the seller a penalty for every day the closing is late. The seller could also refuse to extend the closing date, and the whole deal could fall through.

There are many different parties involved in closing escrow.Depending on your purchase contract and whose fault the delay is, you may have to pay the seller a penalty for every day the closing is late. The seller could also refuse to extend the closing date, and the whole deal could fall through.

Typically, lenders will allow a 30-day rate lock at no cost. If your buyer needs a 60 or 90-day rate lock to meet your closing schedule, that is going to cost money.If you are looking for an abnormally long closing time, you may even want to offer concessions for the buyer to purchase a long-term rate lock.

Every property purchase also has to be reviewed by a title company, and scheduling a time for that can delay the closing date.It's up to the seller to pay the liens (or fight them in court), which can delay closing by weeks, if not months. Personal issues can also delay a closing, Hardy notes.

Most closing dates are open to negotiation, but some are set in stone, so check your contract to see if you can even make a change.That means a final closing date is set, but there's room in the contract for either the buyer or seller to ask the other party for some wiggle room.

Review the details in the contract to see what the allowable time is for a delay on the part of the seller. Usually a 30-day window is applicable. However, if the house closing delayed by the seller moves beyond the allowable window, the seller could be liable for financial losses incurred by the buyer due to a delay.

Asking for 90 days in our market would never happen unless you guaranteed the Seller the EMD if the deal falls through, or put a limited time clause in the contract saying the Seller can still have it listed as active and if they get another offer you have X amount of days to move forward and close now.