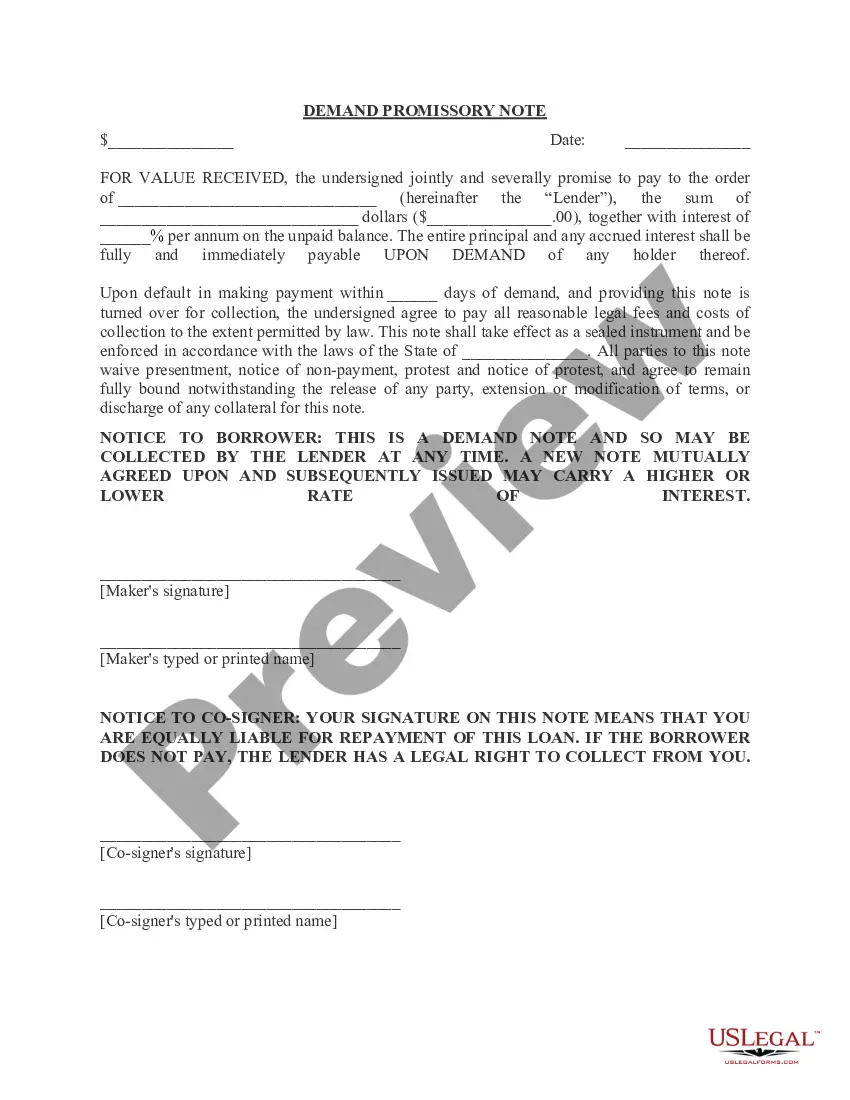

Promissory Note with no Payment Due Until Maturity and Interest to Compound Annually

Understanding this form

The Promissory Note with no payment due until maturity and interest to compound annually is a legal document in which the borrower agrees to repay a specific sum of money to the lender at a future date. This type of promissory note defers all principal and interest payments until maturity, making it distinct from notes that require periodic payments. It is useful for both parties who wish to formalize a loan agreement and understand the terms of repayment in a clear manner.

Key components of this form

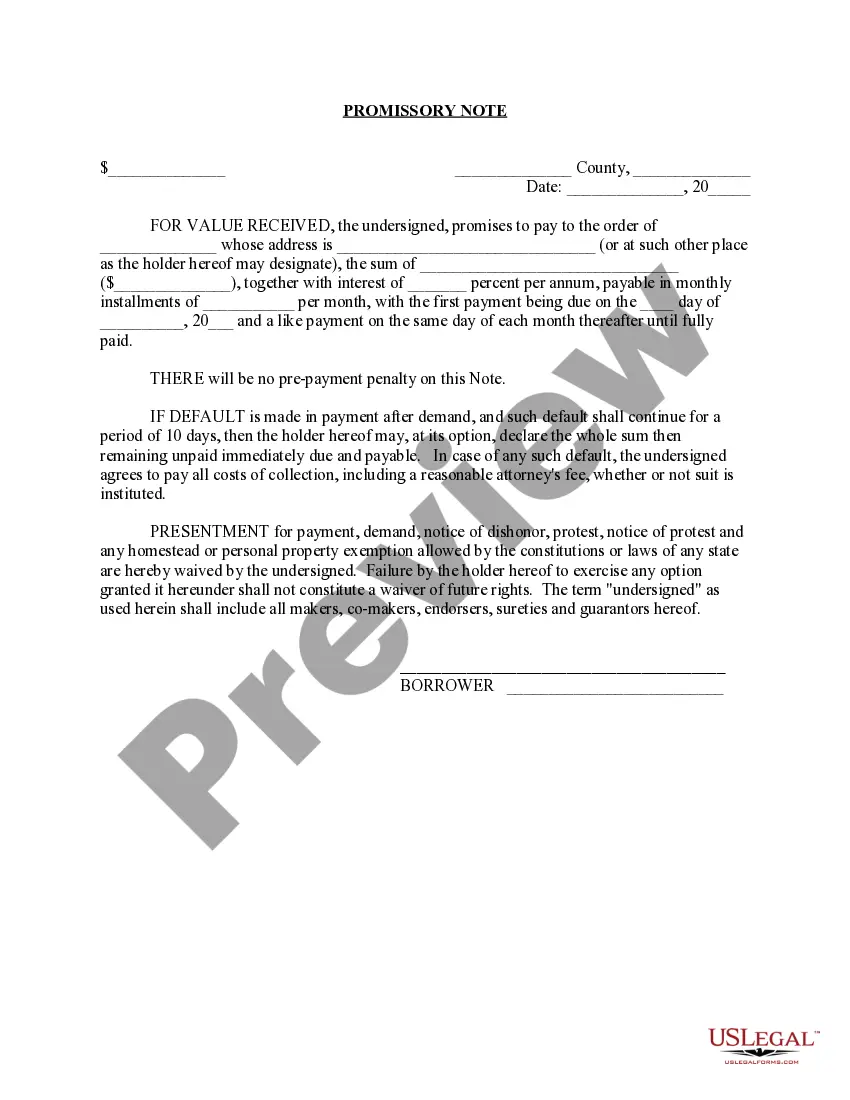

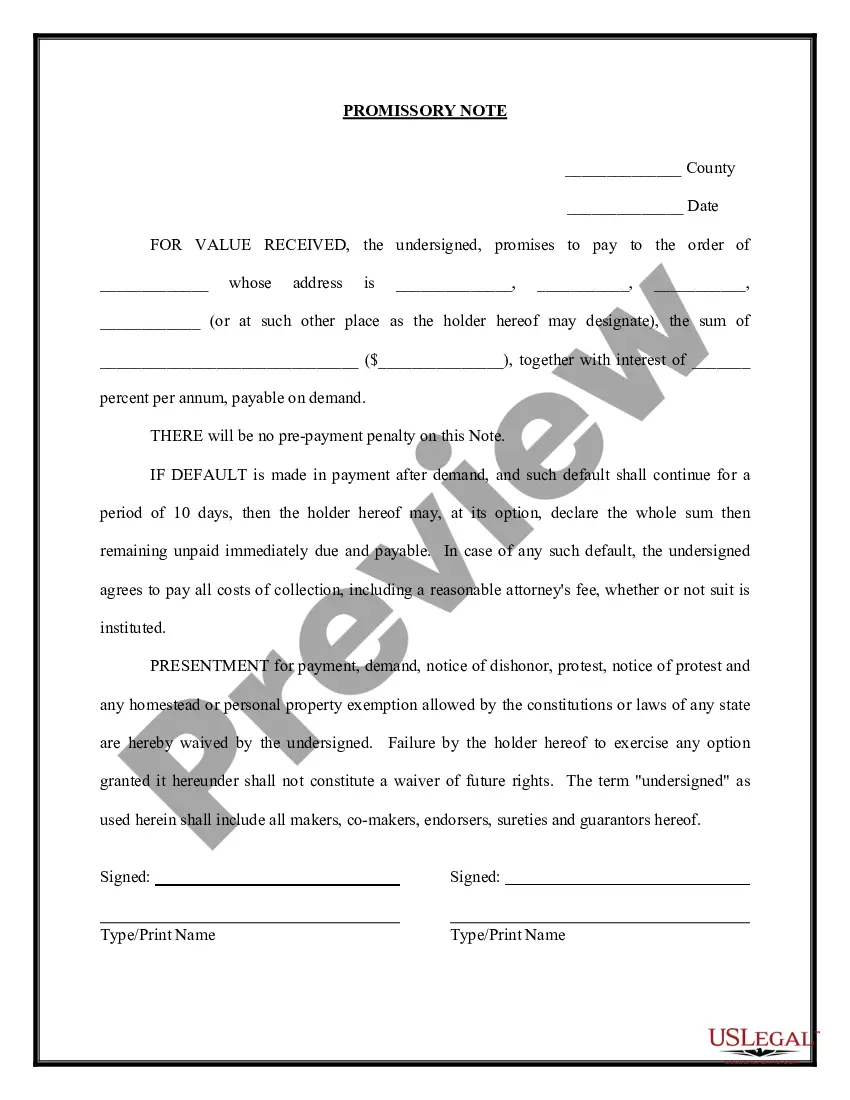

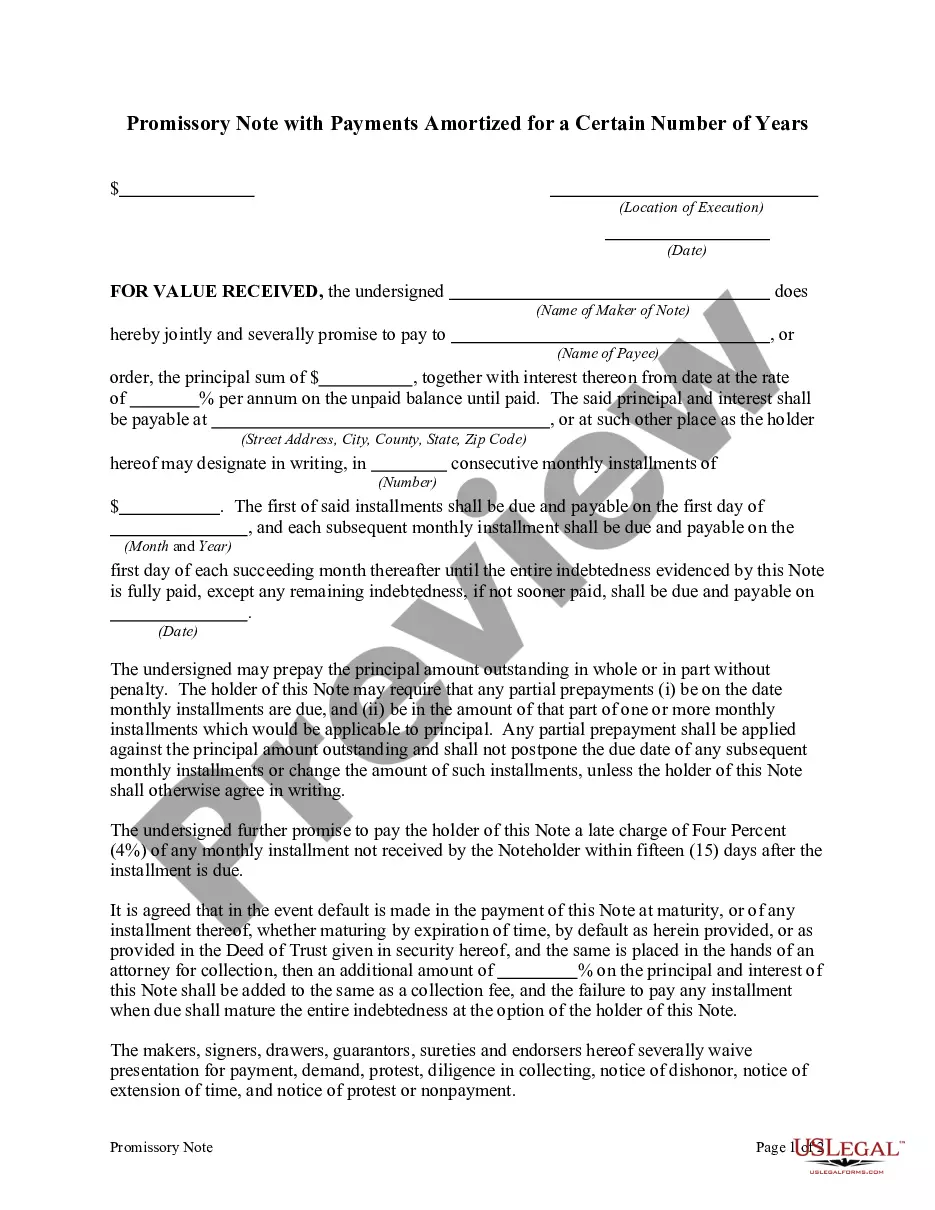

- Principal Amount: The total amount borrowed that the debtor promises to repay.

- Interest Rate: The annual interest percentage on the unpaid balance.

- Maturity Date: The date on which the total amount including interest is due.

- Payment Location: The address where payments should be sent.

- Default Clause: Terms outlining the fees and consequences of late payment.

- Prepayment Option: A provision allowing for early repayment without penalty.

Common use cases

This form is typically used when a borrower desires to take a loan and the lender agrees to defer all payments until a predetermined maturity date. It is suitable for personal loans, business financing, or any situation where detailed terms of repayment are necessary to protect the interests of both the lender and borrower.

Who needs this form

- Individuals seeking personal loans from family or friends.

- Small business owners requiring delayed payments on loans.

- Investors providing loans to entities or individuals.

- Borrowers and lenders looking for clear documentation of loan terms.

Steps to complete this form

- Identify the parties involved by entering the full names and addresses of both the borrower and lender.

- Specify the principal amount of the loan in numerical figures.

- Enter the interest rate that will apply to the loan.

- Set the maturity date when the total payment is due.

- Indicate the address where payments are to be sent.

- Both parties must sign and date the form to finalize the agreement.

Notarization guidance

To make this form legally binding, it must be notarized. Our online notarization service, powered by Notarize, lets you verify and sign documents remotely through an encrypted video session.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Avoid these common issues

- Failing to specify the interest rate, which can lead to misunderstandings.

- Not including the maturity date, which is critical for repayment terms.

- Omitting locations for payments, causing confusion about where to send funds.

- Not signing the document, rendering it unenforceable.

Benefits of using this form online

- Convenience of immediate access and download from any location.

- Editability allows users to tailor the form to their specific needs easily.

- Reliability of professionally drafted templates verified by licensed attorneys.

Legal use & context

- The promissory note is legally enforceable as long as it includes clear terms and both parties consent to the agreement.

- Interest rates must comply with applicable laws to avoid usury claims.

- It's advisable to document any default procedures to enforce the terms effectively.

What to keep in mind

- A promissory note allows a borrower to delay payments until a specified maturity date.

- It's essential to clearly define all terms, including interest rates and payment locations.

- This form can provide a formal agreement in personal, business, or familial lending scenarios.

Looking for another form?

Form popularity

FAQ

A simple promissory note might be for a lump sum repayment on a certain date. For example, you lend your friend $1,000 and he agrees to repay you by December 1. The full amount is due on that date, and there is no payment schedule involved.

Promissory notes are commonly written by banks, lenders and attorneys, but a promissory note written properly can be just as legal when entered into by two individuals.

A promissory note typically contains all the terms pertaining to the indebtedness, such as the principal amount, interest rate, maturity date, date and place of issuance, and issuer's signature.In effect, promissory notes can enable anyone to be a lender.

Step 1 Agree to Terms. Before both parties sit down to write an agreement, the following should be verbally agreed upon: Step 2 Run a Credit Report. Step 3 Security and Co-Signer(s) Step 4 Writing the Promissory Note. Step 5 Paying Back the Borrowed Money.

The borrower and the lender execute the promissory note, and as a result, the borrower becomes legally bound to repay the loan to the lender. If the borrower does not repay the loan, the lender can pursue legal action. If the borrower does fully repay the loan, the lender should mark the promissory note paid in full.

Amount or principal : State the face amount of the money borrowed. Interest rate : If the loan involves interest, the promissory note should include the interest rate charged.For a promissory note to be legally enforceable, the document needs the signature of each party.

Demand promissory notes are notes that do not carry a specific maturity date, but are due on demand of the lender. Usually the lender will only give the borrower a few days' notice before the payment is due. Promissory notes may be used in combination with security agreements.

Calculating Compound InterestCompound interest uses a more complicated formula: You must add 1 to the interest rate (for example, a 5 percent interest rate would mean 1 + 0.05 = 1.05) and then raise the total to the power of whatever the number of periods is for repayment.