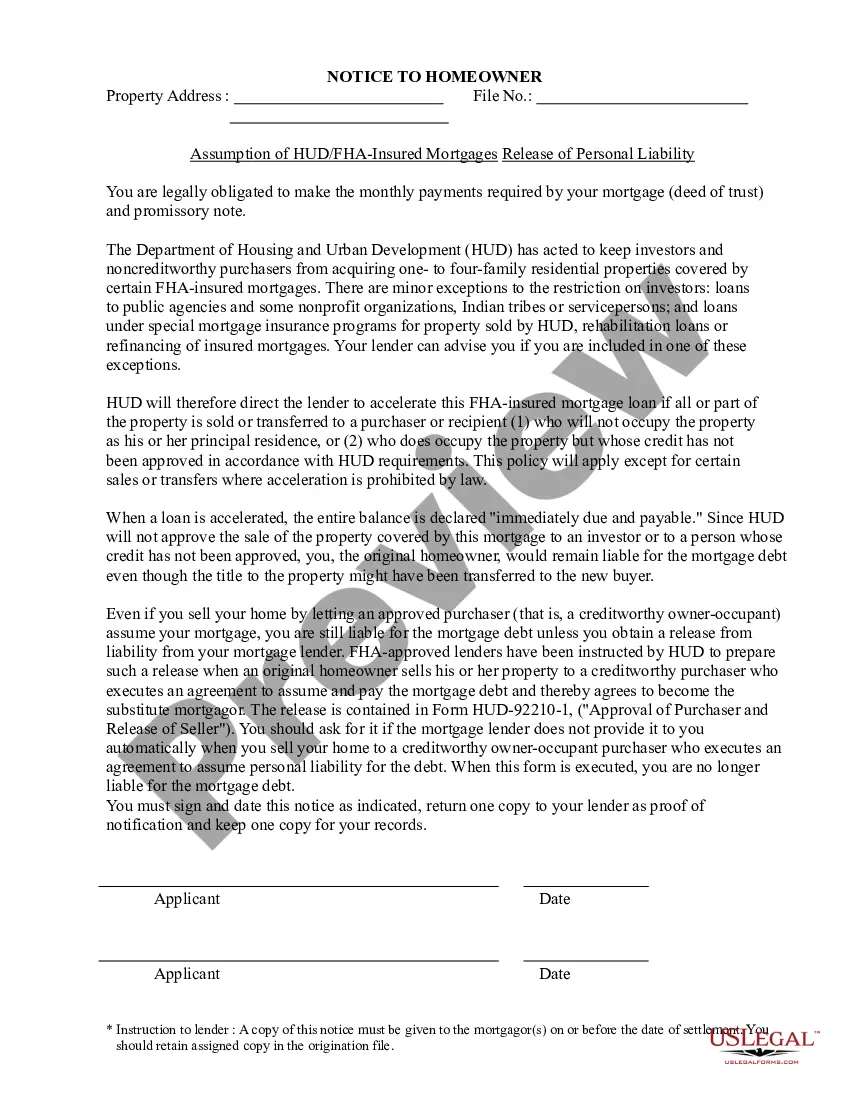

This form is for the situation where the seller is to apply for a release of liability from an assumed loan or reinstatement of VA entitlement.

Texas Addendum for Release of Liability on Assumption of FHA, VA or Conventional Loan, Restoration of Seller's Entitlement for VA Guaranteed Loan

Category:

State:

Multi-State

Control #:

US-00472-A1

Format:

Word;

Rich Text

Instant download

Description

How to fill out Addendum For Release Of Liability On Assumption Of FHA, VA Or Conventional Loan, Restoration Of Seller's Entitlement For VA Guaranteed Loan?

Are you currently in a location where you require documents for business or personal purposes nearly every day.

There are numerous legal document templates available online, but finding reliable ones can be challenging.

US Legal Forms offers thousands of form templates, such as the Texas Addendum for Release of Liability on Assumption of FHA, VA or Conventional Loan, Restoration of Seller's Entitlement for VA Guaranteed Loan, which are designed to comply with federal and state requirements.

Utilize US Legal Forms, the most comprehensive collection of legal forms, to save time and avoid errors.

The service provides professionally crafted legal document templates that you can use for various purposes. Create an account on US Legal Forms and start making your life a bit easier.

- If you are already familiar with the US Legal Forms website and have an account, simply Log In.

- Then, you can download the Texas Addendum for Release of Liability on Assumption of FHA, VA or Conventional Loan, Restoration of Seller's Entitlement for VA Guaranteed Loan template.

- If you do not have an account and wish to start using US Legal Forms, follow these steps.

- Locate the form you need and ensure it is for the correct city/state.

- Use the Review option to evaluate the form.

- Check the description to ensure that you have selected the correct form.

- If the form is not what you’re looking for, use the Search field to find the form that meets your needs and requirements.

- Once you find the correct form, click on Buy now.

- Choose the pricing plan you prefer, fill in the required information to create your account, and complete the purchase using your PayPal or credit card.

- Select a convenient file format and download your copy.

- Access all the document templates you have purchased in the My documents menu. You can obtain another copy of the Texas Addendum for Release of Liability on Assumption of FHA, VA or Conventional Loan, Restoration of Seller's Entitlement for VA Guaranteed Loan at any time if needed. Just click the desired form to download or print the document template.

Form popularity

FAQ

An FHA/VA financing addendum is attached to a purchase contract to state that a buyer with FHA/VA financing can back out of the sale if the appraised property value is less than the asking price.

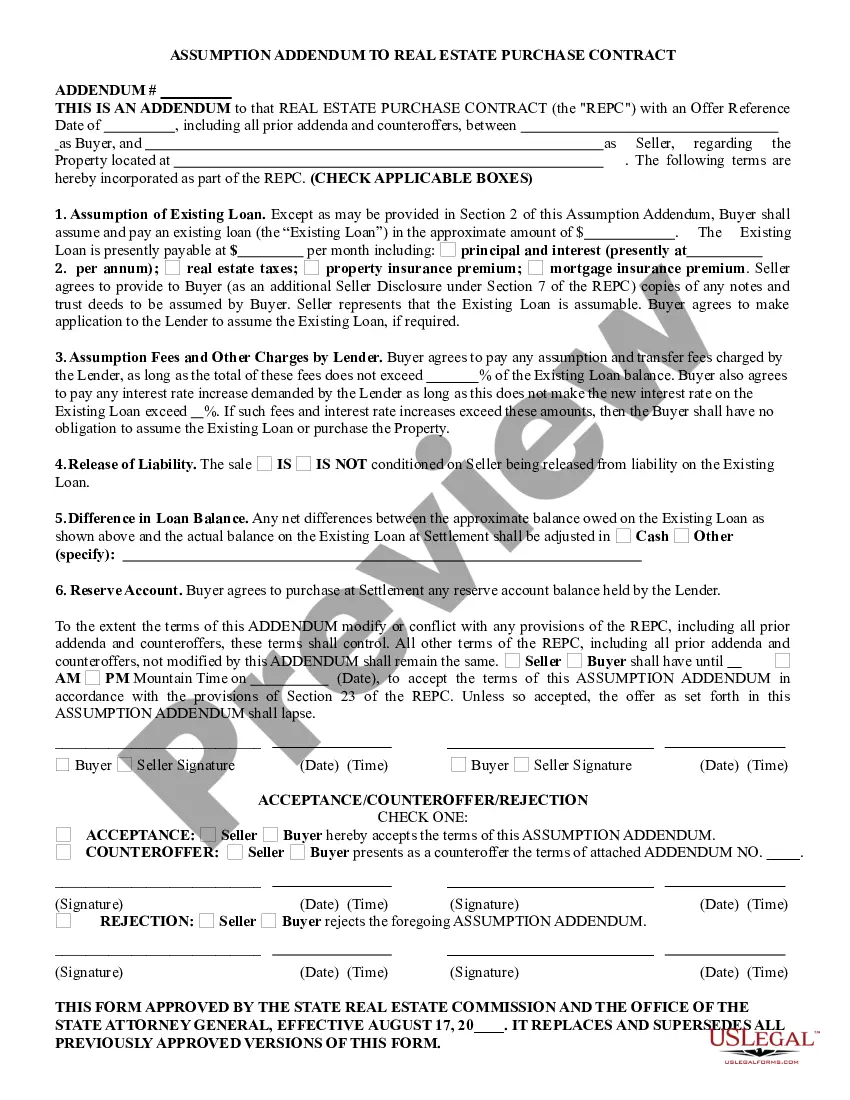

What is a Loan Assumption Agreement? A loan assumption agreement is an agreement between a lender, original borrower, and a new borrower, where the new borrower agrees to assume responsibility for the debt owed by original borrower. These agreements are commonly seen in mortgages and real estate.

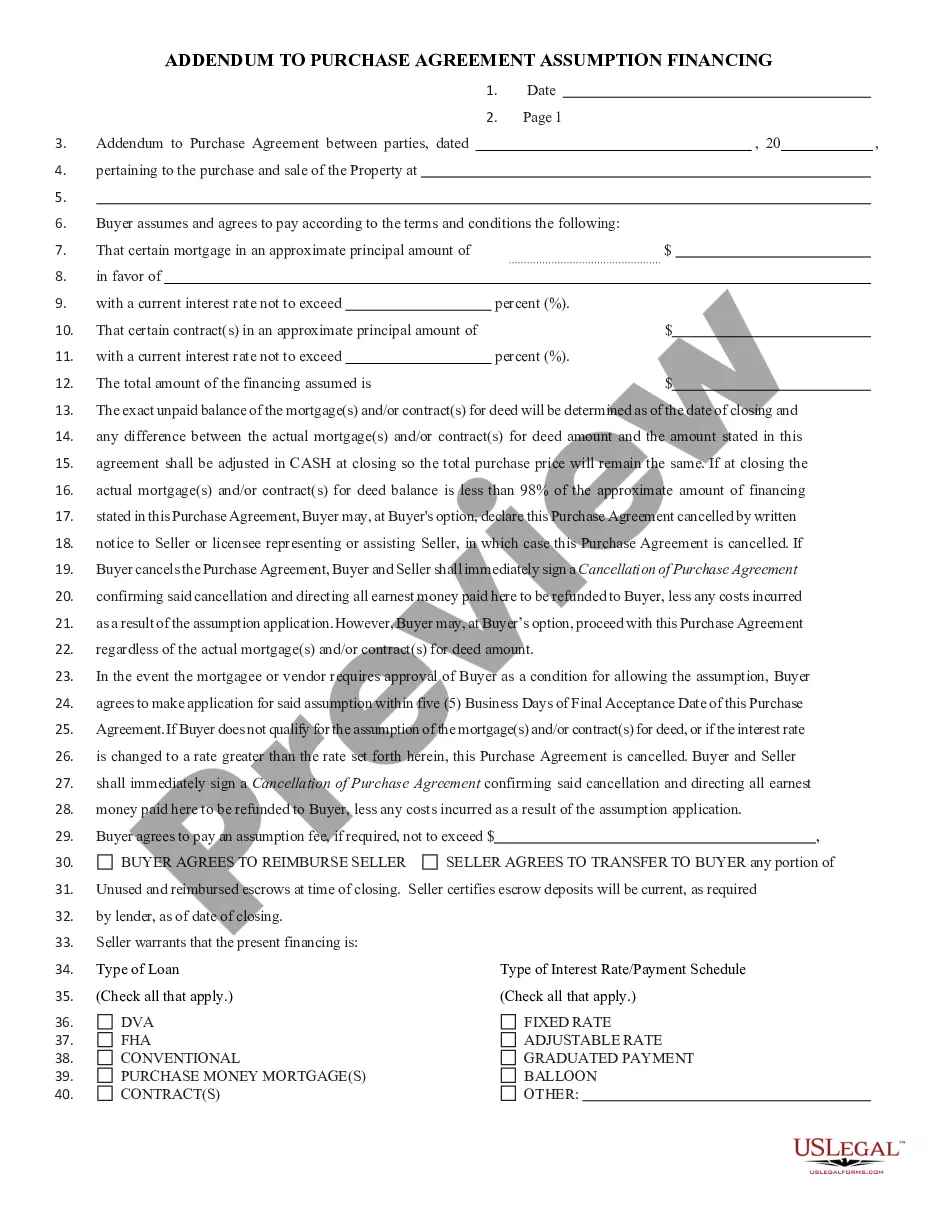

Addendum for Release of Liability on Assumed Loan and/or Restoration of Seller's VA Entitlement. Description: This Addendum is used in conjunction with the Loan Assumption Addendum if the Seller wants to be released from future liability of the loan.

The essential purpose of the FHA and VA amendatory/escape clauses is to give the buyer the right to terminate the sales contract if the sales price exceeds the appraised value of the Property. Form 2A4-T includes the prescribed wording of the FHA and VA amendatory/escape clauses.

A seller financing addendum outlines the terms under which the seller of a property agrees to loan money to the buyer in order to purchase their property.

The Bottom Line The FHA amendatory clause protects borrowers because if the appraisal comes back low, the buyer can cancel the transaction and get their earnest money back. Signing on the dotted line for a home that appraises for below the sales price could result in a bad investment for both lenders and buyers.

If the buyer cannot obtain the loan approval in time, they will need to give the seller written notice and they can terminate the contract and receive their earnest money back. The buyer can also opt to make make the contract not subject to buyer approval.

VA loans include certain contingencies that protect earnest money deposits and allow them to be refunded to the buyer under specific circumstances. Some of the most common VA contract contingencies include a home inspection contingency, financing contingency, home sale contingency and appraisal contingency.