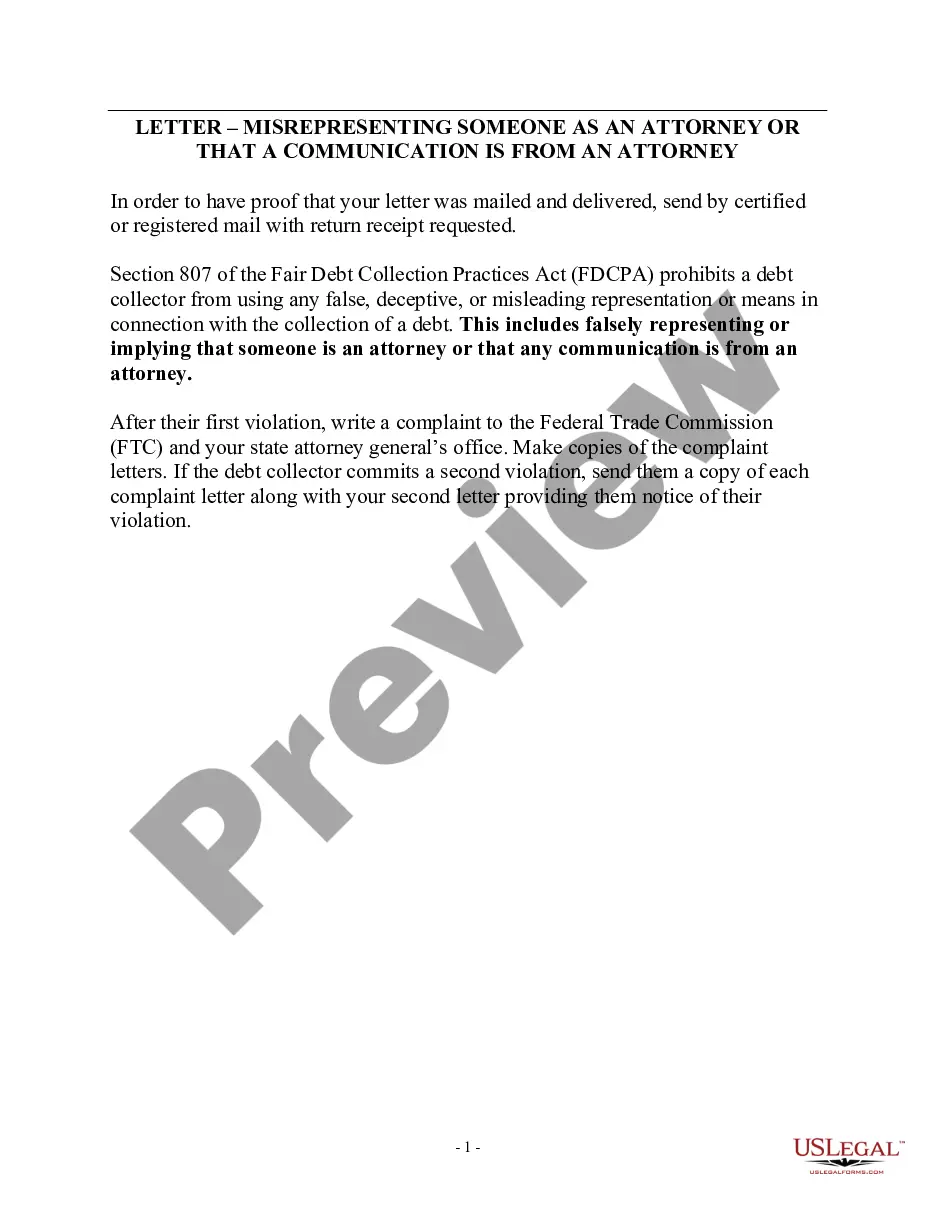

Tennessee Notice of Violation of Fair Debt Act - Creditor Misrepresented Himself

Description

How to fill out Notice Of Violation Of Fair Debt Act - Creditor Misrepresented Himself?

US Legal Forms - one of the largest repositories of legal documents in the United States - provides a vast selection of legal document templates you can download or create.

While navigating the website, you can discover thousands of forms for business and personal purposes, organized by categories, states, or keywords. You will find the latest versions of forms such as the Tennessee Notice of Violation of Fair Debt Act - Creditor Misrepresented Himself in mere moments.

If you hold a subscription, Log In to acquire Tennessee Notice of Violation of Fair Debt Act - Creditor Misrepresented Himself from the US Legal Forms library. The Download button will appear on every form you review. You have access to all previously downloaded forms in the My documents section of your account.

Process the transaction. Utilize your Visa or Mastercard or PayPal account to complete the transaction.

Select the format and download the form to your device. Edit. Complete, modify, and print and sign the downloaded Tennessee Notice of Violation of Fair Debt Act - Creditor Misrepresented Himself. Each template you add to your account has no expiration date and is yours indefinitely. Therefore, if you wish to download or generate another copy, simply navigate to the My documents section and click on the form you desire.

- Ensure you have selected the correct form for your city/state.

- Click the Review button to examine the form's content.

- Check the form details to confirm you have selected the right form.

- If the form does not suit your needs, use the Lookup field at the top of the screen to find the appropriate one.

- If you are satisfied with the form, confirm your choice by clicking the Purchase now button.

- Then, select the pricing plan you prefer and provide your information to register for the account.

Form popularity

FAQ

For most debts, the time limit is 6 years since you last wrote to them or made a payment. The time limit is longer for mortgage debts. If your home is repossessed and you still owe money on your mortgage, the time limit is 6 years for the interest on the mortgage and 12 years on the main amount.

If a debt collector violates the FDCPA, you may sue that collector in state or federal court. You can even sue in small claims court. You must do this within one year from the date on which the violation occurred.

If you make a payment (even as small as $5), the debt collector will be given the right to sue you again, leading to possible wage garnishment. In Tennessee the statute of limitations on debt is as follows: Mortgage debt: 6 years. Medical debt: 6 years.

7 Most Common FDCPA ViolationsContinued attempts to collect debt not owed.Illegal or unethical communication tactics.Disclosure verification of debt.Taking or threatening illegal action.False statements or false representation.Improper contact or sharing of info.Excessive phone calls.

Debt collectors cannot harass or abuse you. They cannot swear, threaten to illegally harm you or your property, threaten you with illegal actions, or falsely threaten you with actions they do not intend to take. They also cannot make repeated calls over a short period to annoy or harass you.

Among the insider tips, Ulzheimer shared with the audience was this: if you are being pursued by debt collectors, you can stop them from calling you ever again by telling them '11-word phrase'. This simple idea was later advertised as an '11-word phrase to stop debt collectors'.

Your credit card debt, auto loans, medical bills, student loans, mortgage, and other household debts are covered under the FDCPA.

There is a statute of limitations on debt in Tennessee which is 6 years. This means that if the debt does not get closed out in six years, a lender is not eligible to sue the person to collect the debt.

Tennessee judgments are good for 10 years. Rule 69.04, amended by the Tennessee Supreme Court in 2016, makes the process now even easier to extend the life of a judgment.

In California, the statute of limitations on most debts is four years. With some limited exceptions, creditors and debt buyers can't sue to collect debt that is more than four years old. When the debt is based on a verbal agreement, that time is reduced to two years.