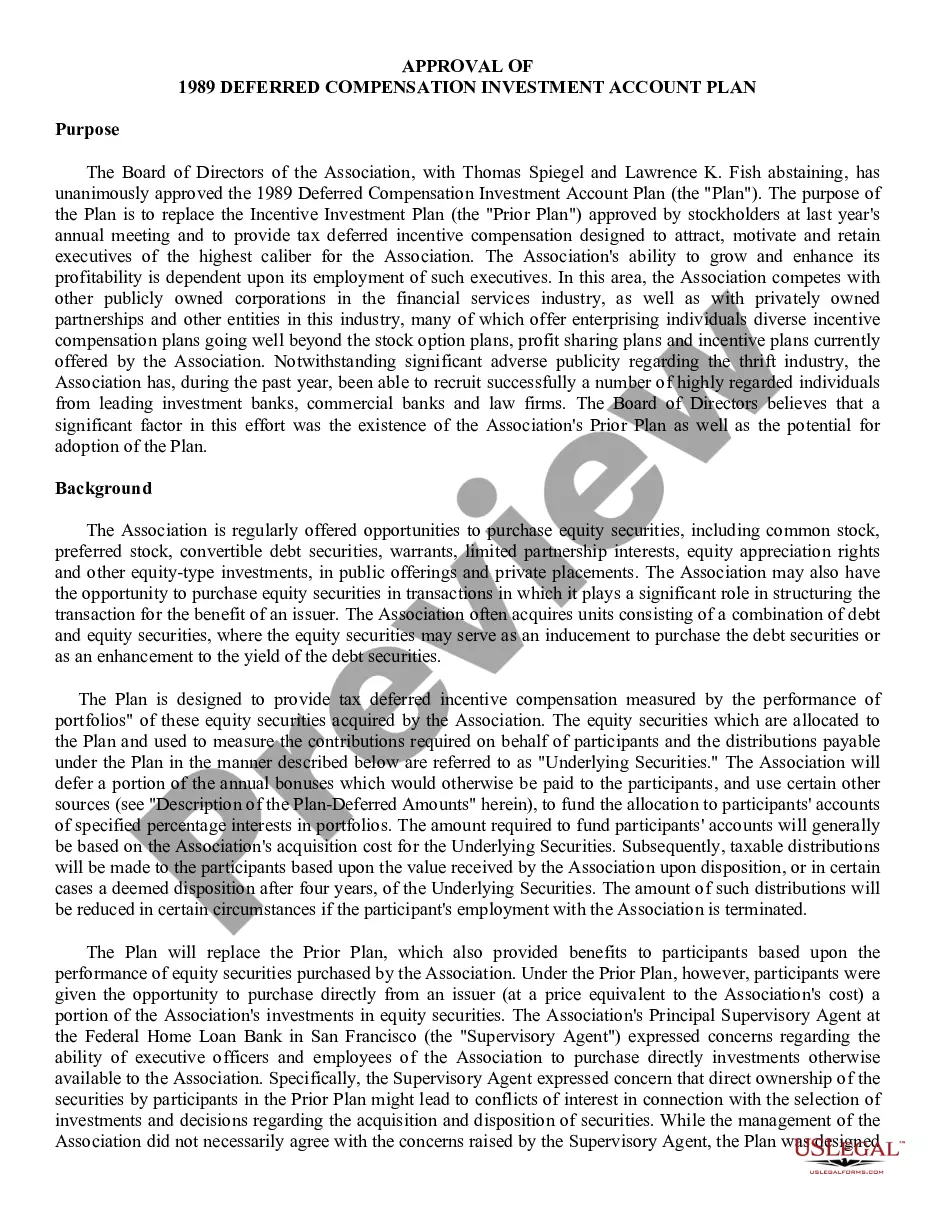

20-146 20-146 . . . Deferred Compensation Investment Account Plan under which Board of Directors of Savings and Loan Association allocates a portion of annual bonuses which would otherwise be paid to selected officers and employees to a separate account. The deferred compensation in such account is deemed, for purposes of Plan only, to represent specified percentages of Association's investments in certain portfolios of equity securities, and it is increased or decreased to same extent as performance of such securities

Tennessee Deferred Compensation Investment Account Plan

State:

Multi-State

Control #:

US-CC-20-146

Format:

Word;

Rich Text

Instant download

Description

Free preview

How to fill out Deferred Compensation Investment Account Plan?

Choosing the right legal papers design can be quite a have difficulties. Of course, there are plenty of themes available on the net, but how would you obtain the legal develop you want? Make use of the US Legal Forms internet site. The service provides thousands of themes, for example the Tennessee Deferred Compensation Investment Account Plan, which can be used for organization and personal requires. All the kinds are checked by pros and meet up with state and federal specifications.

In case you are presently authorized, log in for your accounts and then click the Down load key to get the Tennessee Deferred Compensation Investment Account Plan. Make use of accounts to search from the legal kinds you have purchased formerly. Visit the My Forms tab of your own accounts and get yet another backup in the papers you want.

In case you are a fresh consumer of US Legal Forms, listed below are simple directions for you to comply with:

- Very first, make sure you have chosen the proper develop for your town/area. You are able to examine the form utilizing the Review key and look at the form explanation to guarantee it is the right one for you.

- In case the develop is not going to meet up with your preferences, utilize the Seach area to find the correct develop.

- Once you are certain the form is acceptable, select the Purchase now key to get the develop.

- Pick the prices prepare you desire and enter in the needed details. Design your accounts and pay for an order with your PayPal accounts or Visa or Mastercard.

- Pick the data file file format and download the legal papers design for your system.

- Comprehensive, change and print out and indicator the received Tennessee Deferred Compensation Investment Account Plan.

US Legal Forms will be the largest local library of legal kinds that you can discover a variety of papers themes. Make use of the service to download appropriately-made paperwork that comply with express specifications.

Form popularity

FAQ

That flaw resulted in companies and agencies across the U.S. experiencing a security breach. On June 26, TCRS said the security breach had affected 171,836 retirees and their beneficiaries. They released a statement about the security breach, available below.

Assets in a 457(b) plan can be rolled over into most other retirement accounts, including into a traditional IRA, a Roth IRA, another 457(b) plan, a 403(b), a 401(a) or a 401(k) plan.

Additional savings opportunity As an added benefit, the State of Tennessee offers the ability to save through a 457 deferred compensation plan. The 457 has the same investment options as the 401(k) and does not share a contribution limit with other retirement plans.

The ORP is a deferred compensation plan that lets you take control of your retirement by contributing to investment options of your choice. You are immediately vested in the ORP and can decide how your money should be invested given your individual goals, risk tolerance, and timeline.

Cons of 457(b) plans: Fewer investing options than 401(k)s (Not as common today) Only available to certain employees employed by state or local governments or qualifying nonprofits. Employer contributions count toward the annual limit. Non-governmental 457(b) plans are riskier.

Plans of deferred compensation described in IRC section 457 are available for certain state and local governments and non-governmental entities tax exempt under IRC Section 501. They can be either eligible plans under IRC 457(b) or ineligible plans under IRC 457(f).

The 457 plan is a retirement savings plan and you generally cannot withdraw money while you are still employed. When you leave employment, you may withdraw funds; leave them in place; transfer them to a 457, 403(b) or 401(k) of a new employer; or roll them into an Individual Retirement Account (IRA).

Investment options available in 457(b) plans are generally limited to annuities and mutual funds. You can't buy exchange-traded funds (ETFs) or individual stocks in a 457(b) account, for instance.