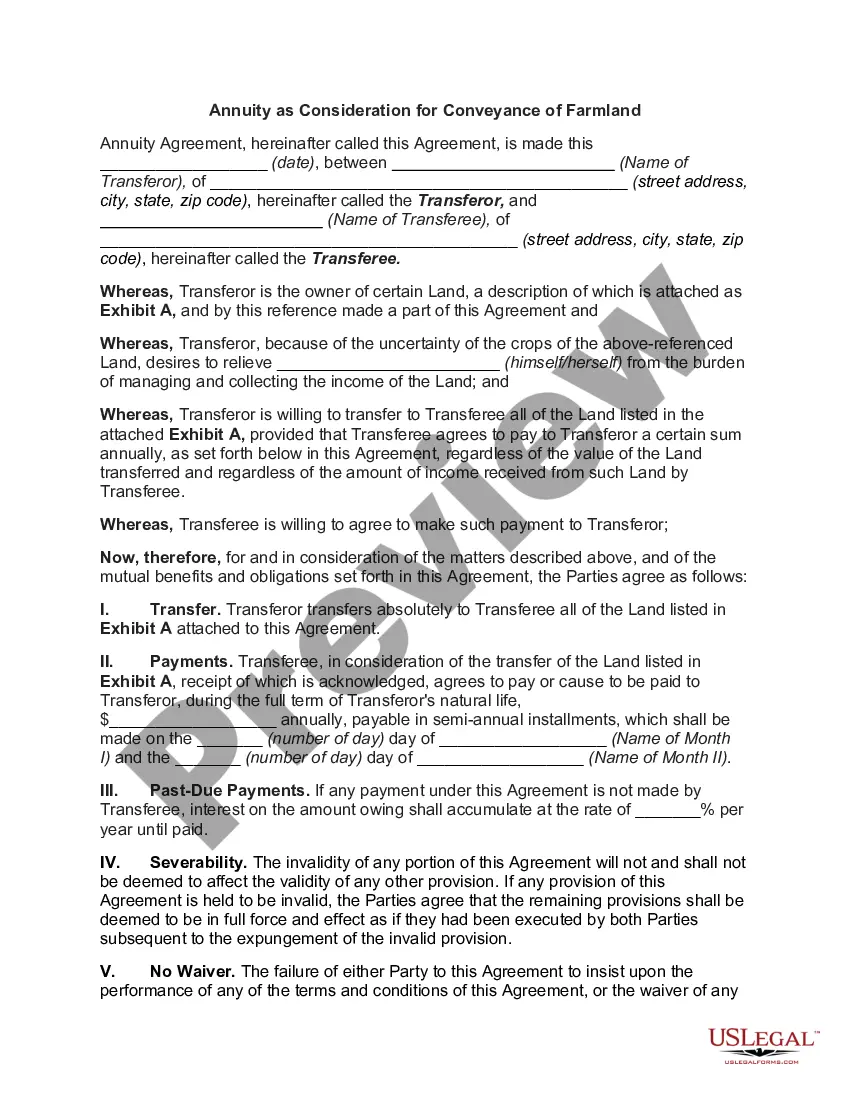

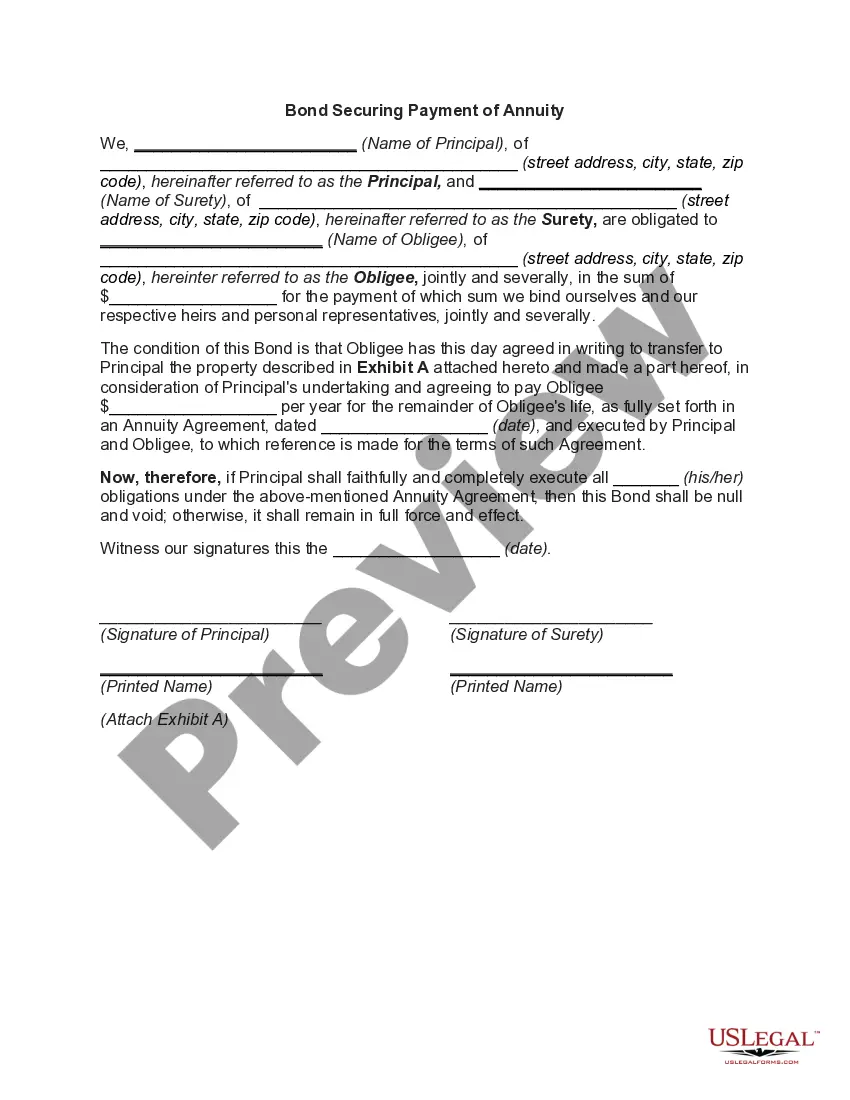

Tennessee Annuity as Consideration for Transfer of Securities

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Annuity As Consideration For Transfer Of Securities?

If you wish to obtain, secure, or print authentic document templates, utilize US Legal Forms, the largest compilation of authentic forms available online.

Employ the site’s straightforward and effective search feature to locate the documents you require.

Various templates for business and personal purposes are organized by categories and states, or by keywords. Utilize US Legal Forms to find the Tennessee Annuity as Consideration for Transfer of Securities with only a few clicks.

Every legal document template you purchase is yours indefinitely. You have access to every form you downloaded in your account.

Click the My documents section and select a form to print or download again. Complete and download, and print the Tennessee Annuity as Consideration for Transfer of Securities using US Legal Forms. There are millions of professional and state-specific forms available for your business or personal needs.

- If you are already a US Legal Forms user, Log In to your account and click on the Download option to obtain the Tennessee Annuity as Consideration for Transfer of Securities.

- You can also access forms you have previously downloaded within the My documents tab of your account.

- If you are using US Legal Forms for the first time, follow the instructions below.

- Step 1. Ensure you have selected the form for the correct state/country.

- Step 2. Use the Review option to examine the form’s content.

- Remember to read the description.

- Step 3. If you are not satisfied with the form, use the Search field at the top of the screen to find other templates in the legal form library.

- Step 4. Once you have found the form you need, select the Get now option. Choose the pricing plan you prefer and enter your credentials to register for an account.

- Step 5. Process the payment. You may use your Visa or MasterCard or PayPal account to complete the transaction.

- Step 6. Select the format of the legal form and download it to your device.

- Step 7. Complete, modify, and print or sign the Tennessee Annuity as Consideration for Transfer of Securities.

Form popularity

FAQ

Variable annuities are securities and under FINRA's jurisdiction. Annuities are often products investors consider when they plan for retirementso it pays to understand them. They also are often marketed as tax-deferred savings products.

Index Annuity Withdrawals It's actually the norm with tax-advantaged retirement accounts. Just like its fixed and variable cousins, index annuity payments are classified as either immediate or deferred. An immediate annuity will begin payments within 12 months of signing your contract.

Indexed annuities are not securities and do not earn interest based on specific investments. Rather, indexed annuity rates fluctuate in relation to a specific index, such as the S&P 500. In contrast to variable annuities, indexed annuities are guaranteed not to lose money.

Annuities can provide a reliable income stream in retirement, but if you die too soon, you may not get your money's worth. Annuities often have high fees compared to mutual funds and other investments. You can customize an annuity to fit your needs, but you'll usually have to pay more or accept a lower monthly income.

An indexed annuity may or may not be a security; however, most indexed annuities are not registered with the SEC. Fixed annuities are not securities and are not regulated by the SEC.

An annuity consideration or premium is the money an individual pays to an insurance company to fund an annuity or receive a stream of annuity payments. An annuity consideration may be made as a lump sum or as a series of payments, often referred to as contributions.

The main drawbacks are the long-term contract, loss of control over your investment, low or no interest earned, and high fees. There are also fewer liquidity options with annuities, and you have to wait until age 59.5 to withdraw any money from the annuity without penalty.

The fees for variable annuities can be extremely high. Among the biggest drawbacks of variable annuities are the recurring fees. These are to pay for the risks and costs associated with protecting your money. As an example, an annuity fee could amount to roughly 1.25% of the amount you've invested.

Unlike fixed annuities, variable annuities are considered securities and are regulated by the SEC and FINRA. Variable annuities' principal is placed in investment portfolios. The performance of the investments in the portfolios dictates the interest rates.

The main difference between this and owning stocks outright is that the portfolio is inside an annuity. Everything else is pretty much the same same asset class, same type of returns, same investment risk. But the annuity provides additional features that are not available through common stock ownership.