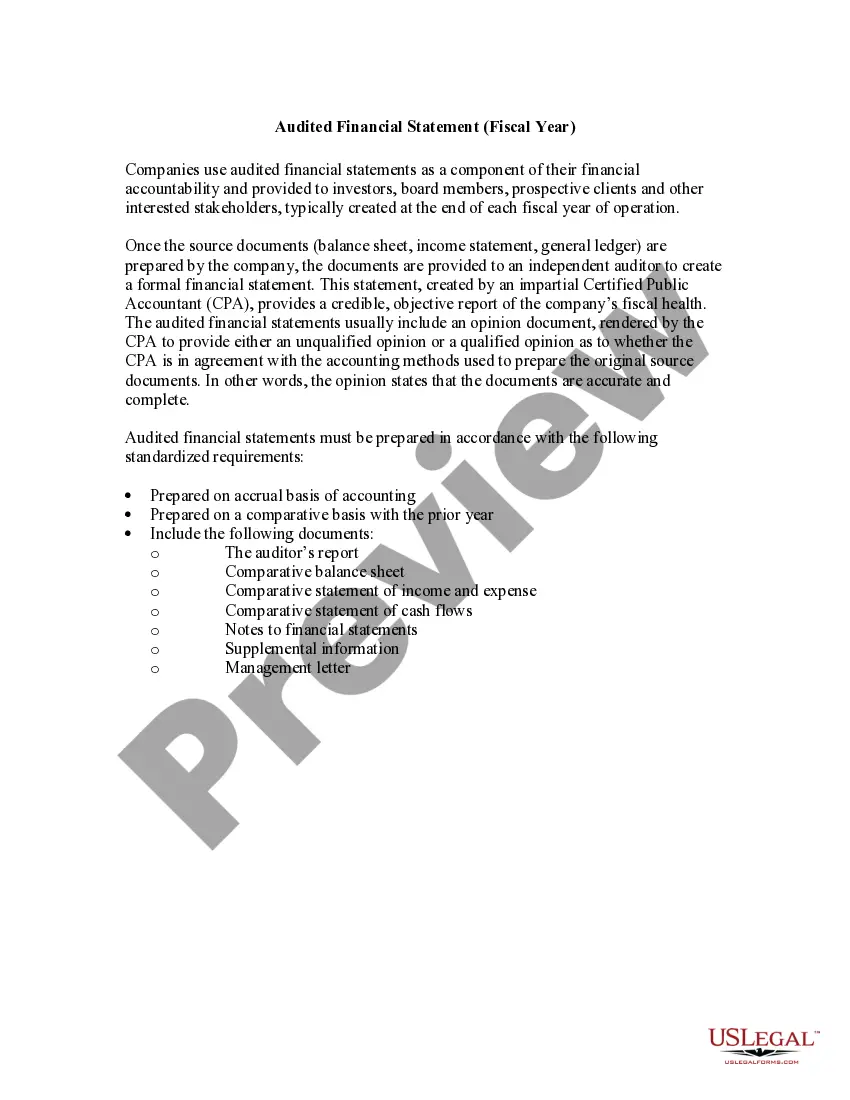

As most commonly used in legal settings, an audit is an examination of financial records and documents and other evidence by a trained accountant. Audits are conducted of records of a business or governmental entity, with the aim of ensuring proper accounting practices, recommendations for improvements, and a balancing of the books. An audit performed by employees is called "internal audit," and one done by an independent (outside) accountant is an "independent audit." Auditors may refuse to sign the audit to guarantee its accuracy if only limited records are produced.

South Carolina Report of Independent Accountants after Audit of Financial Statements

Category:

State:

Multi-State

Control #:

US-01939BG

Format:

Word

Instant download

Description

How to fill out Report Of Independent Accountants After Audit Of Financial Statements?

Are you in a situation where you require documents for either business or personal reasons almost all the time.

There are numerous legal document templates accessible online, but finding versions you can trust is not simple.

US Legal Forms offers thousands of form templates, such as the South Carolina Report of Independent Accountants after Audit of Financial Statements, which are designed to meet federal and state requirements.

Once you find the right form, click on Buy now.

Choose the pricing plan you prefer, complete the required details to set up your account, and pay for the transaction using your PayPal or credit card. Select a convenient file format and download your copy.

- If you are already familiar with the US Legal Forms website and have your account, simply Log In.

- Then, you can download the South Carolina Report of Independent Accountants after Audit of Financial Statements template.

- If you do not have an account and wish to start using US Legal Forms, follow these instructions.

- Obtain the template you need and ensure it is for the correct city/county.

- Use the Preview button to examine the form.

- Check the description to confirm you have selected the right template.

- If the form is not what you are looking for, use the Search field to find a form that meets your needs.

Form popularity

FAQ

Whether you need to file audited financial statements depends on various factors such as the size of your business and your specific industry regulations. Many organizations benefit greatly from producing the South Carolina Report of Independent Accountants after Audit of Financial Statements, as it can satisfy regulatory requirements and improve accountability. If your business seeks funding or partnerships, audited financials can provide the necessary assurance to potential investors. Using US Legal Forms, you can easily find the right templates and guidance for filing these documents.

The main reason for a financial statement audit by an independent CPA is to ensure transparency and reliability in your financial reporting. This process culminates in the South Carolina Report of Independent Accountants after Audit of Financial Statements. An independent CPA examines your financials to identify any discrepancies, ensuring that stakeholders can trust the information presented. This level of scrutiny not only boosts investor confidence but also helps you make informed business decisions.

Yes, an accountant can perform an audit, but they must be a certified public accountant with the appropriate credentials and certifications. Not all accountants have the training required to conduct audits effectively. In the context of the South Carolina Report of Independent Accountants after Audit of Financial Statements, it is crucial to select an accountant with audit experience. Doing so ensures that the audit meets industry standards and provides trustworthy results.

Only qualified professionals, such as certified public accountants (CPAs) or independent auditors, can audit financial statements. These individuals possess the necessary education and credentials to perform audits effectively. Regarding the South Carolina Report of Independent Accountants after Audit of Financial Statements, it is essential to engage someone with the right qualifications. This qualification assures stakeholders of the reliability and integrity of the financial statements.

The responsibility for auditing financial statements typically falls on independent auditors or certified public accountants. These professionals are trained to apply auditing standards to evaluate financial documents critically. For the South Carolina Report of Independent Accountants after Audit of Financial Statements, understanding this responsibility is key for organizations preparing for an audit. Their expertise helps ensure compliance and accuracy in financial reporting.

An independent accountant is a professional who conducts financial audits without any conflicts of interest. These accountants evaluate financial statements and ensure compliance with regulations. Their role is crucial in producing the South Carolina Report of Independent Accountants after Audit of Financial Statements, which requires objectivity and expertise. Their insights not only confirm accuracy but also enhance stakeholders' confidence in the financial reporting.

An effective audit report typically includes an introduction, management's responsibilities, the auditor's responsibilities, the audit results, and a conclusion. In the context of the South Carolina Report of Independent Accountants after Audit of Financial Statements, each section plays a vital role in conveying essential information. The introduction provides the context, while the conclusion sums up the overall findings. Detailed contents ensure that users understand the results of the audit clearly.

The function of an independent audit is to provide an objective evaluation of an organization's financial statements, ensuring accuracy and integrity. This process helps build trust among stakeholders, as it serves as a safeguard against fraud or misrepresentation. Therefore, the South Carolina Report of Independent Accountants after Audit of Financial Statements plays a vital role in enhancing transparency and accountability across various sectors.

An independent CPA becomes associated with financial statements when they conduct an audit or review of those statements. This association is crucial as it lends credibility to the financial reports, serving stakeholders’ needs for assurance. The resulting South Carolina Report of Independent Accountants after Audit of Financial Statements reflects this relationship, indicating that the CPA has evaluated the financial records thoroughly.

An independent audit report is generally focused on providing an unbiased opinion of an organization’s financial statements, while a statutory audit report is a legal requirement for certain companies, ensuring they comply with local regulations. Both serve distinct purposes, yet the South Carolina Report of Independent Accountants after Audit of Financial Statements can fall under one or both categories, depending on the context of the audit.