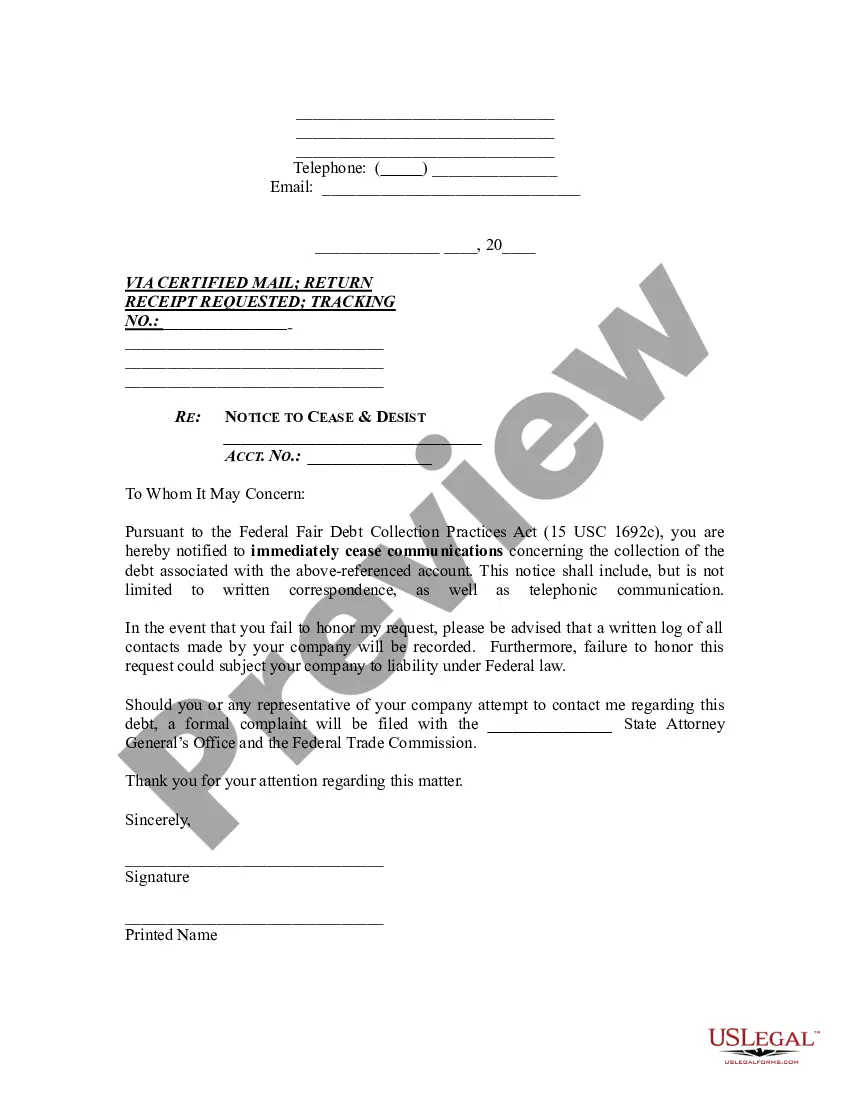

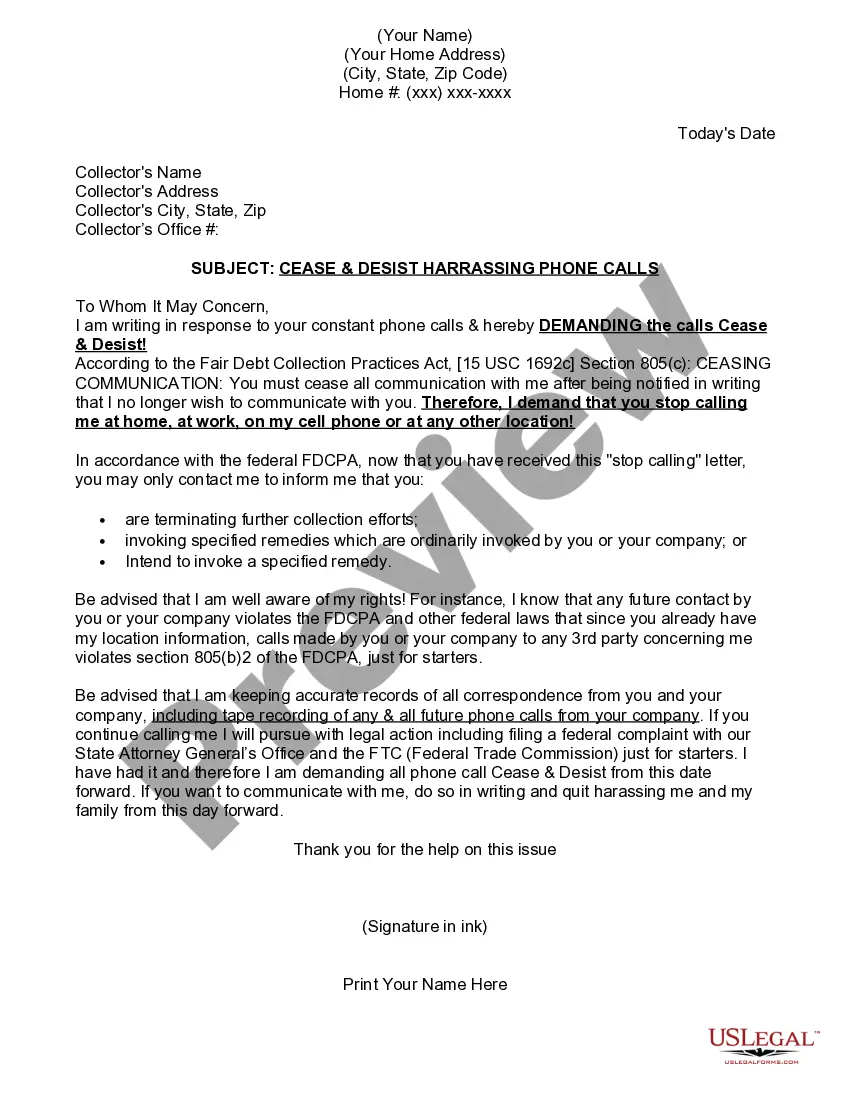

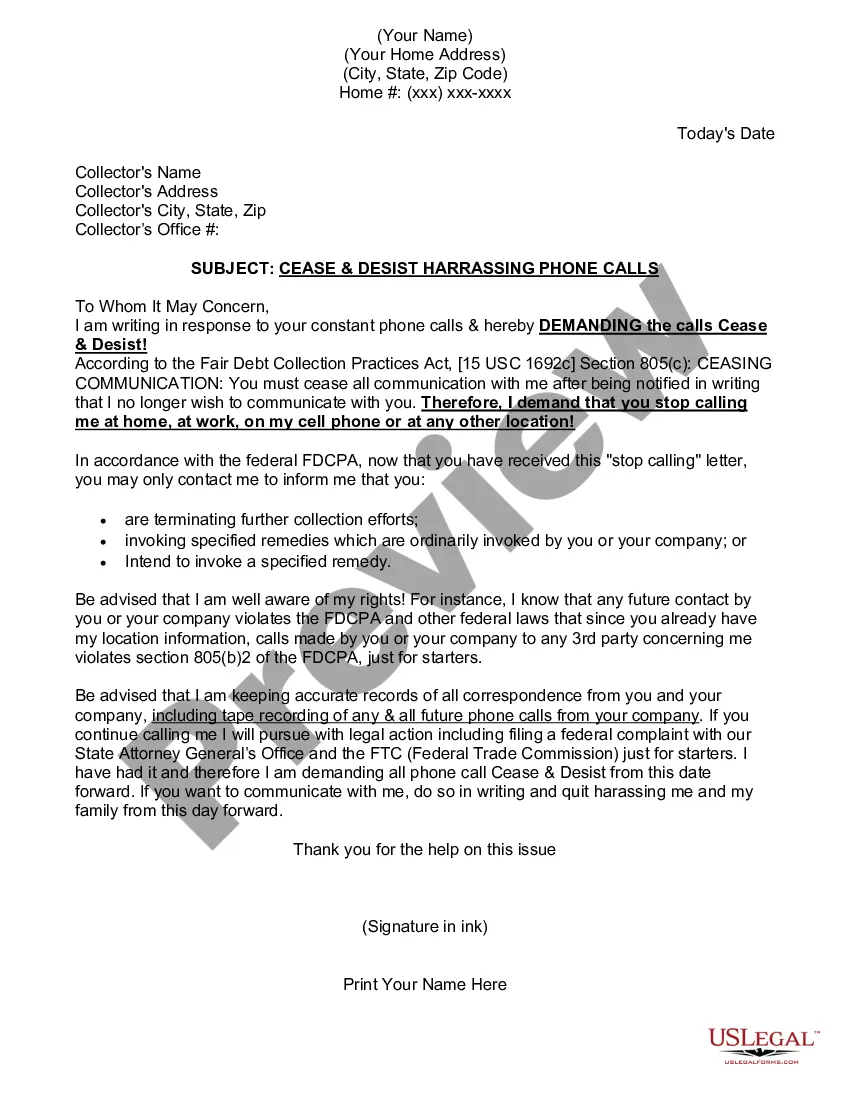

Puerto Rico Cease and Desist for Debt Collectors

Description

How to fill out Cease And Desist For Debt Collectors?

Finding the correct legal document format can be challenging. Of course, there are numerous templates available online, but how do you find the legal form you require? Utilize the US Legal Forms website. The service offers thousands of templates, including the Puerto Rico Cease and Desist for Debt Collectors, which can be used for business and personal purposes. All forms are verified by professionals and comply with state and federal regulations.

If you are already a member, sign in to your account and click the Download button to obtain the Puerto Rico Cease and Desist for Debt Collectors. Use your account to view the legal forms you have purchased previously. Visit the My documents section of your account and retrieve another copy of the document you need.

If you are a new user of US Legal Forms, here are simple instructions for you to follow: First, ensure that you have selected the correct form for your area/region. You can review the form using the Preview button and check the form description to confirm it is the right one for you. If the form does not meet your requirements, use the Search box to find the appropriate form. Once you are sure the form is suitable, click the Get now button to obtain the form. Choose the payment plan you prefer and enter the required information. Create your account and complete your purchase using your PayPal account or credit card. Select the document format and download the legal document format to your device. Finally, complete, edit, print, and sign the acquired Puerto Rico Cease and Desist for Debt Collectors.

- US Legal Forms is the largest repository of legal forms where you can find numerous document templates.

- Utilize the service to obtain professionally crafted papers that comply with state regulations.

- Access a wide variety of legal templates suitable for different needs.

- Easily manage your documents and past purchases through your account.

- Ensure compliance and accuracy with forms reviewed by experts.

- Enjoy a user-friendly platform for all your legal documentation needs.

Form popularity

FAQ

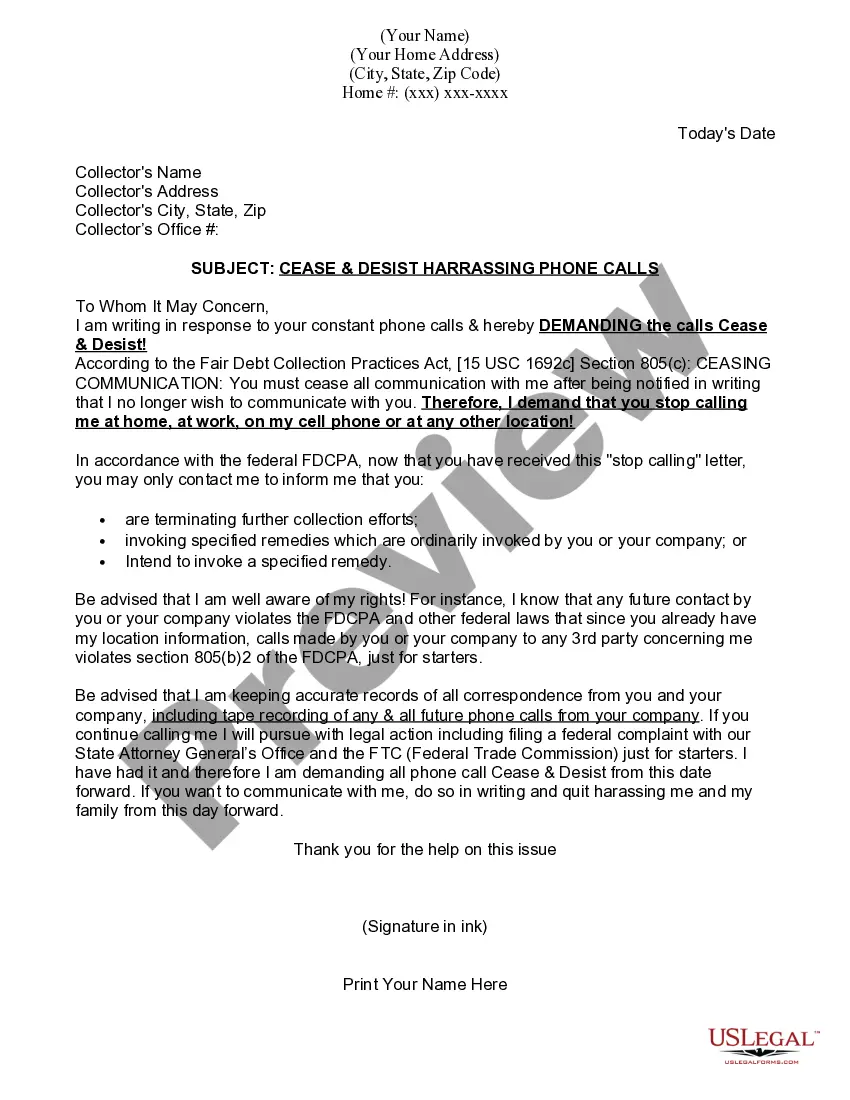

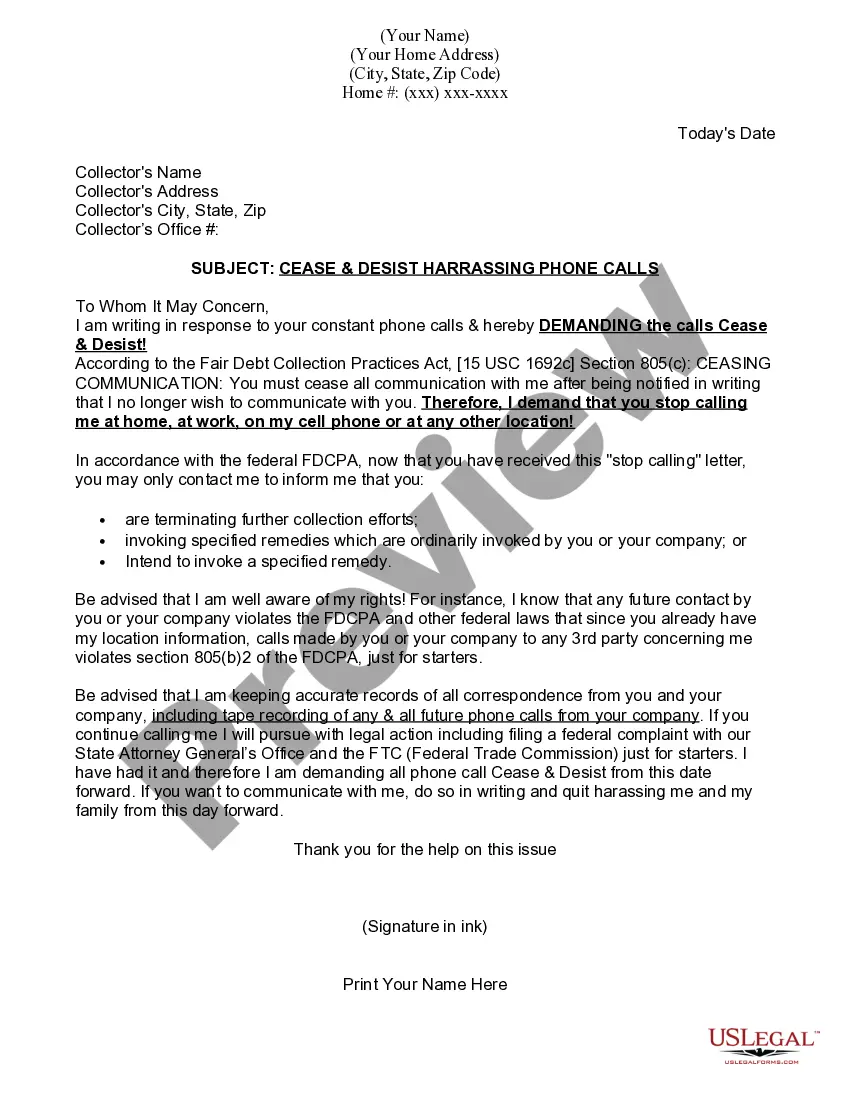

Yes, cease and desist letters can be effective in stopping communication from debt collectors. Once a collector receives your letter, they are legally obligated to cease further contact regarding the debt. This legal protection can provide you with much-needed relief and peace of mind. Utilizing resources like uslegalforms can help you craft a strong cease and desist letter tailored for Puerto Rico Cease and Desist for Debt Collectors.

When sending a cease and desist letter, you do not need to provide extensive proof; however, it helps to include any relevant documentation related to the debt. This can include previous correspondence, payment records, or any evidence that supports your position. Your goal is to make it clear to the debt collector why you believe their actions should stop. By focusing on the Puerto Rico Cease and Desist for Debt Collectors, you can protect your rights effectively.

To write an effective cease and desist letter to a debt collector, start by clearly stating your intention to stop any communication regarding the debt. Include your contact information and the specific debt in question. It is essential to request that the collector refrain from contacting you further, while mentioning your rights under the Fair Debt Collection Practices Act. Using a service like uslegalforms can simplify this process and ensure your letter is comprehensive and compliant with Puerto Rico Cease and Desist for Debt Collectors.

A 609 letter is a request for validation that you send to a debt collector. It is named after Section 609 of the Fair Credit Reporting Act, which allows consumers to ask for proof that they owe a debt. When you use this letter, you can demand that the collector provide evidence of the debt's legitimacy. This process is crucial in managing your financial situation, especially when dealing with Puerto Rico Cease and Desist for Debt Collectors.

Yes, you can send a cease and desist letter to a debt collector in Puerto Rico. This letter serves as a formal request to the collector to stop all communication regarding your debt. By using a Puerto Rico Cease and Desist for Debt Collectors, you assert your rights under the Fair Debt Collection Practices Act. Utilizing platforms like US Legal Forms can simplify this process, providing you with templates that ensure your letter is properly formatted and legally sound.

A debt becomes legally uncollectible once the statute of limitations expires, which is usually 15 years for consumer debts in Puerto Rico. After this period, creditors can no longer sue you or leverage legal means to collect the debt. If you face persistent collection efforts after this time, you can issue a Puerto Rico Cease and Desist for Debt Collectors to assert your rights. This action can effectively halt unwanted communications and provide you with peace of mind.

In Puerto Rico, the statute of limitations on most consumer debts is typically 15 years. This means that creditors have this time frame to initiate legal action to collect the owed amount. If you receive a collection notice after this period, you might consider sending a Puerto Rico Cease and Desist for Debt Collectors. Doing so can help protect your rights and prevent unjust collection efforts.

The 7 7 7 rule for collections refers to a guideline that helps consumers understand their rights regarding debt collection. Under this rule, a collector must provide written notice within seven days of contacting you, detailing the amount owed and the creditor's name. If you send a Puerto Rico Cease and Desist for Debt Collectors, you can stop further communications. This gives you time to evaluate the situation and consider your options.

Yes, you can send a cease and desist letter to a debt collector at any time. This letter formally requests that they stop all communication regarding the debt. It is important to ensure that the letter is clear and concise to avoid any confusion. Using a Puerto Rico Cease and Desist for Debt Collectors can streamline this process and help you take control of your situation.

The 11-word phrase you can use to stop debt collectors is 'I do not owe this debt and request no further contact.' This statement clearly communicates your position and invokes your rights under federal law. When delivered through a Puerto Rico Cease and Desist for Debt Collectors, it can be a powerful tool to halt unwanted communication. Be assertive in protecting your financial well-being.