Pennsylvania Split-Dollar Life Insurance

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Split-Dollar Life Insurance?

US Legal Forms - one of many most significant libraries of authorized varieties in the States - delivers an array of authorized document layouts you may download or produce. Using the internet site, you can get a huge number of varieties for business and individual functions, categorized by categories, states, or keywords.You can get the most up-to-date models of varieties such as the Pennsylvania Split-Dollar Life Insurance within minutes.

If you already have a registration, log in and download Pennsylvania Split-Dollar Life Insurance in the US Legal Forms library. The Down load key will show up on each and every form you perspective. You get access to all in the past saved varieties in the My Forms tab of your own account.

If you want to use US Legal Forms the very first time, listed below are basic directions to help you started off:

- Ensure you have picked the proper form for the metropolis/state. Click the Review key to analyze the form`s articles. Browse the form information to ensure that you have chosen the right form.

- When the form does not fit your requirements, utilize the Research industry on top of the screen to discover the one that does.

- Should you be pleased with the form, verify your option by simply clicking the Purchase now key. Then, opt for the costs plan you like and provide your credentials to sign up to have an account.

- Approach the deal. Use your credit card or PayPal account to perform the deal.

- Select the format and download the form in your gadget.

- Make changes. Load, modify and produce and signal the saved Pennsylvania Split-Dollar Life Insurance.

Each and every design you added to your money does not have an expiration date and is yours eternally. So, in order to download or produce yet another version, just check out the My Forms area and click in the form you need.

Get access to the Pennsylvania Split-Dollar Life Insurance with US Legal Forms, probably the most substantial library of authorized document layouts. Use a huge number of specialist and state-certain layouts that meet your business or individual requires and requirements.

Form popularity

FAQ

Split-limit car insurance is defined as a policy that divides liability coverage into three separate limits for bodily injury per person, bodily injury per accident, and property damage per accident. Insurance companies often write these limits as three separate numbers.

Having two or more policies instead of one is called splitting of an insurance policy. If you are very particular about buying split policies, you may buy a normal term cover for 30 years or until retirement and buy another coverage that will cover you for life.

Yes. If the policyholder would like to name multiple beneficiaries to a single policy, he or she can specify any number of ?co-beneficiaries.? When multiple beneficiaries are listed, insurance companies can split the same death benefit amongst them.

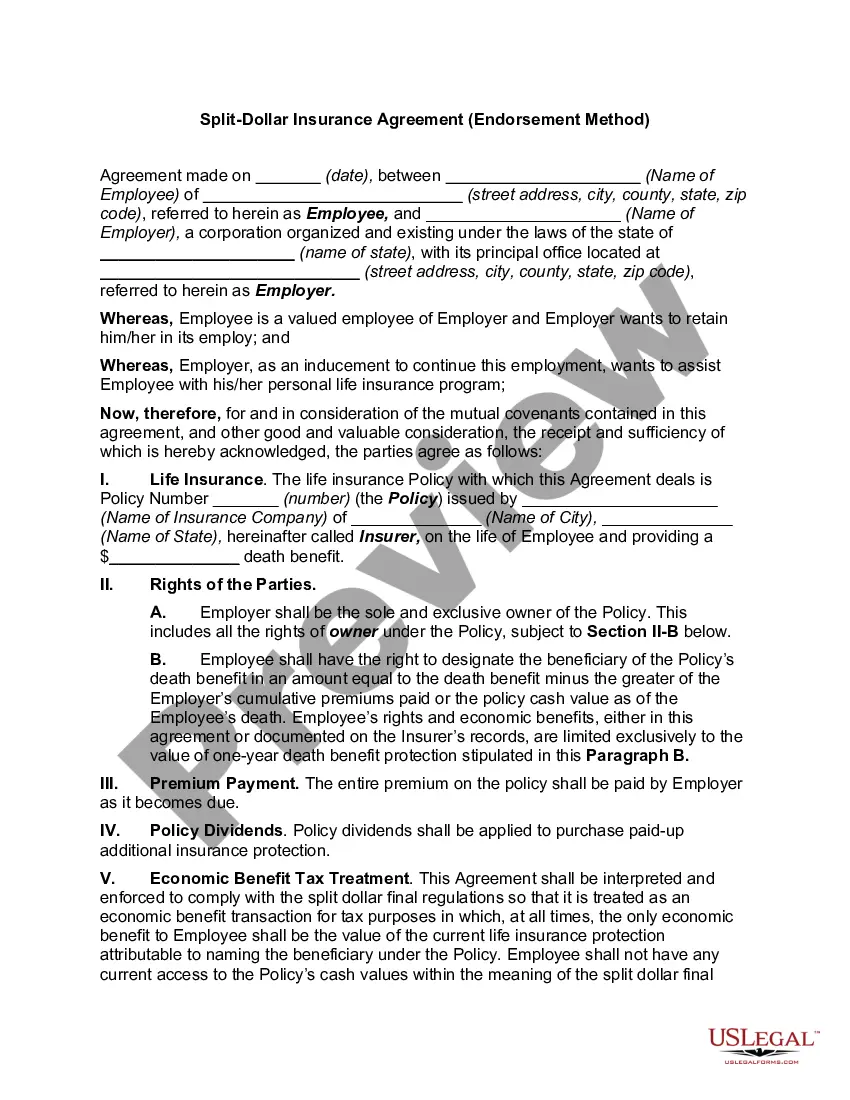

Split-dollar life insurance is an agreement where two parties ? an employer and an employee ? agree to split the benefits, and sometimes the costs, of a life insurance policy. The employer pays the life insurance premium, in whole or in part, on a cash value life insurance policy purchased on the life of the employee.

Split-dollar life insurance can be a mutually beneficial arrangement for employers and employees, with each party gaining different advantages. For example, employees receive quality life insurance for little cost and may be able to access tax-efficient income through withdrawals or loans.

dollar life insurance agreement (or ?splitdollar plan?) is a strategy generally used as an employer benefit or for estate planning involving life insurance. It's an agreement between two or more parties to share the ownership, costs, and benefits of a permanent life insurance policy, like whole life.

Split-dollar life insurance can be a mutually beneficial arrangement for employers and employees, with each party gaining different advantages. For example, employees receive quality life insurance for little cost and may be able to access tax-efficient income through withdrawals or loans.

Reverse Split-Dollar Arrangements In a reverse split-dollar arrangement, the employer owns the death benefit and the employee owns the cash value.