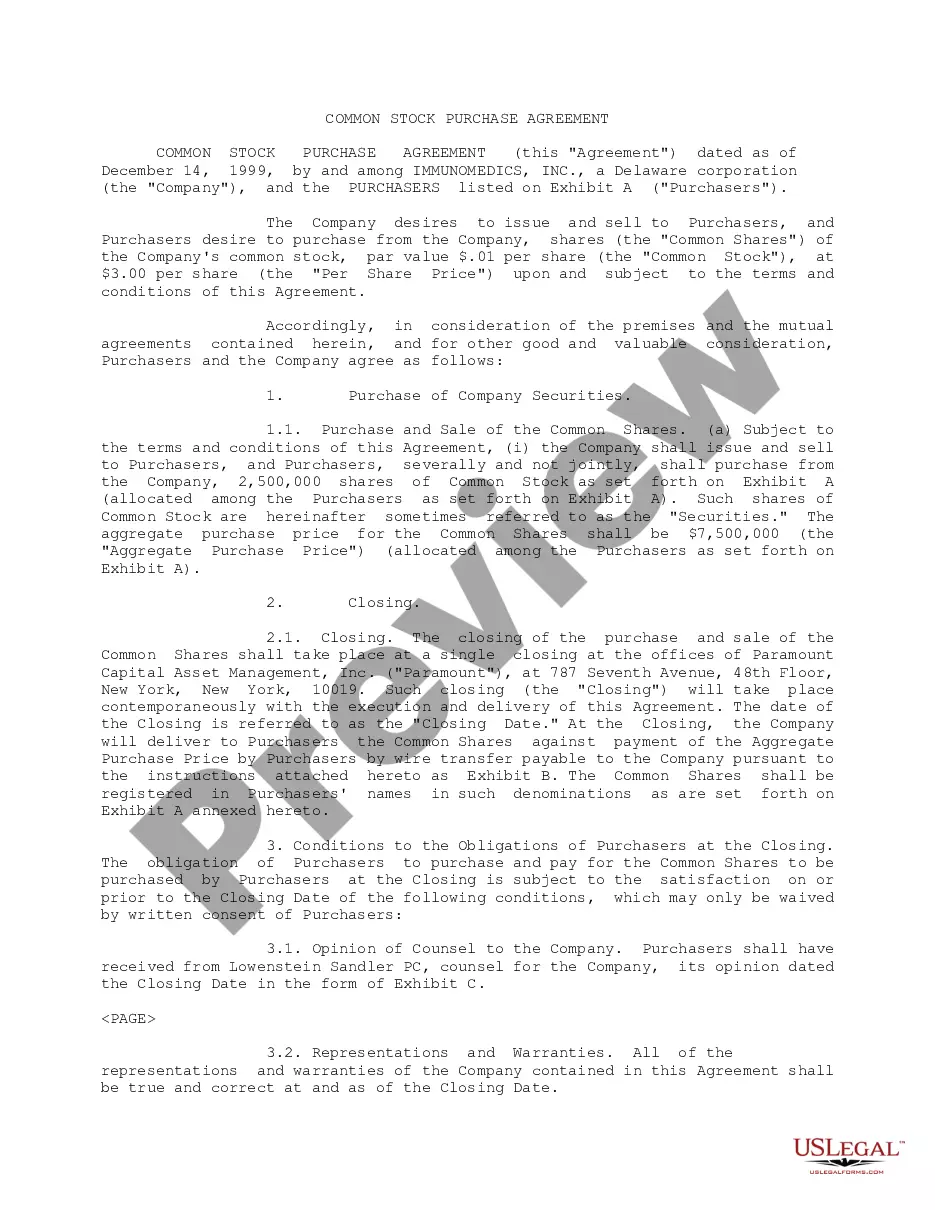

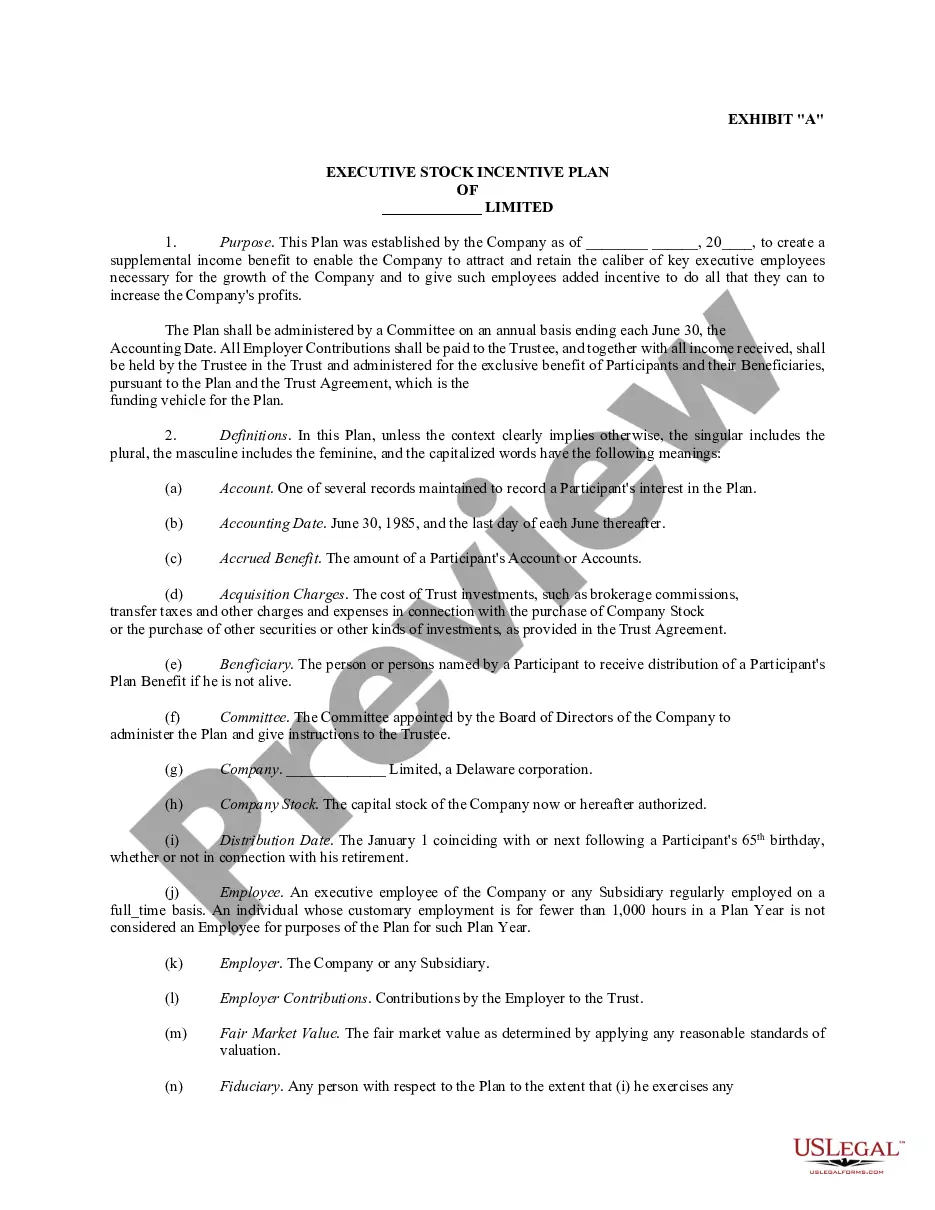

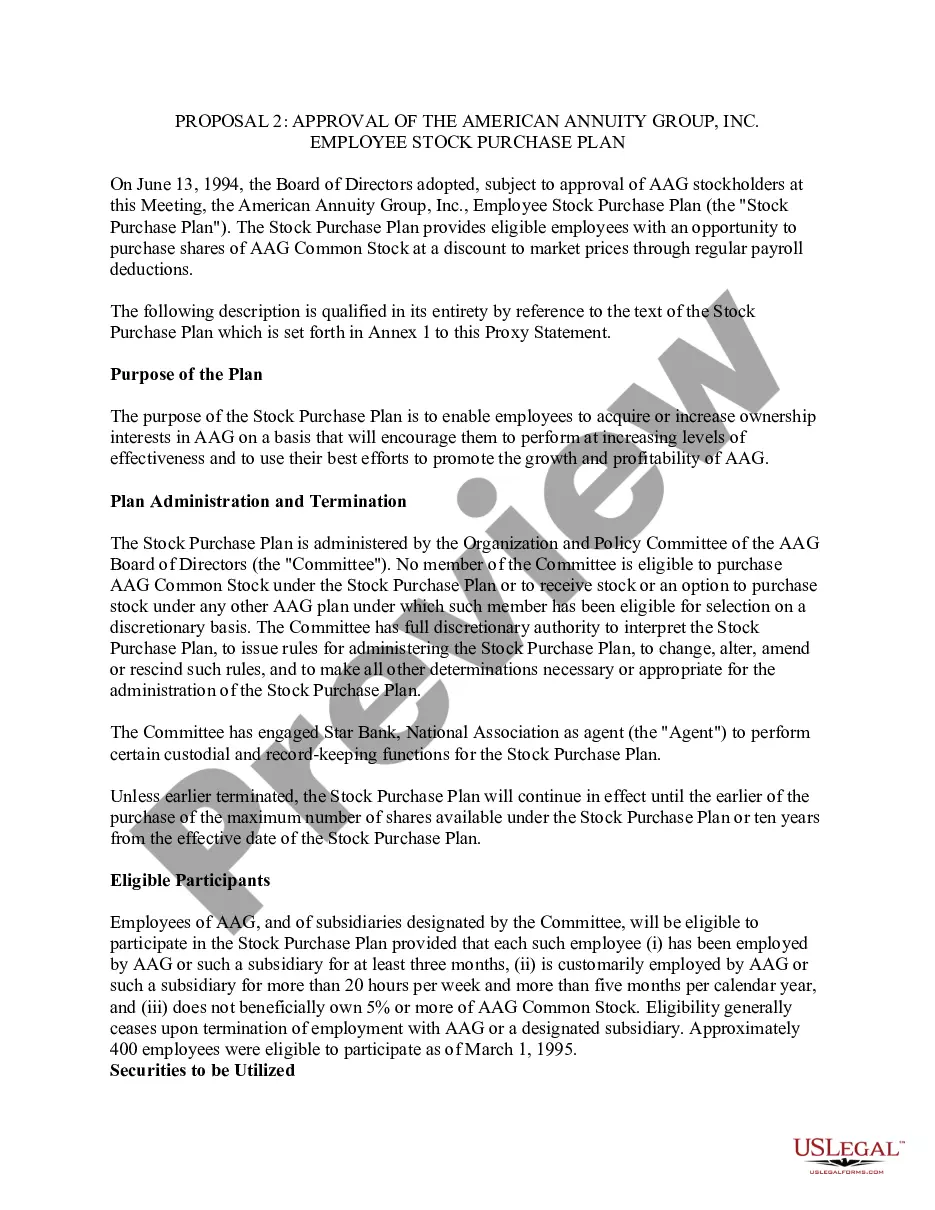

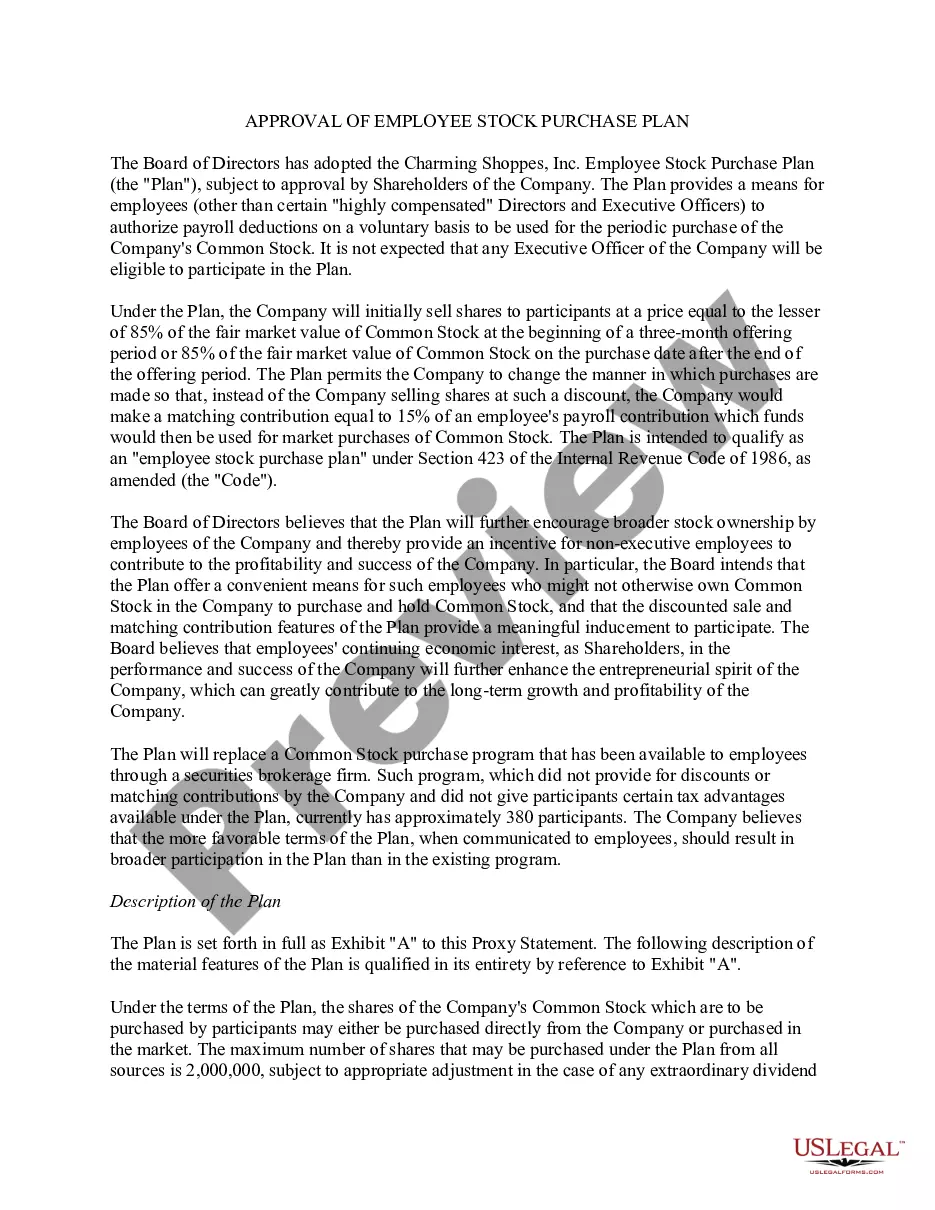

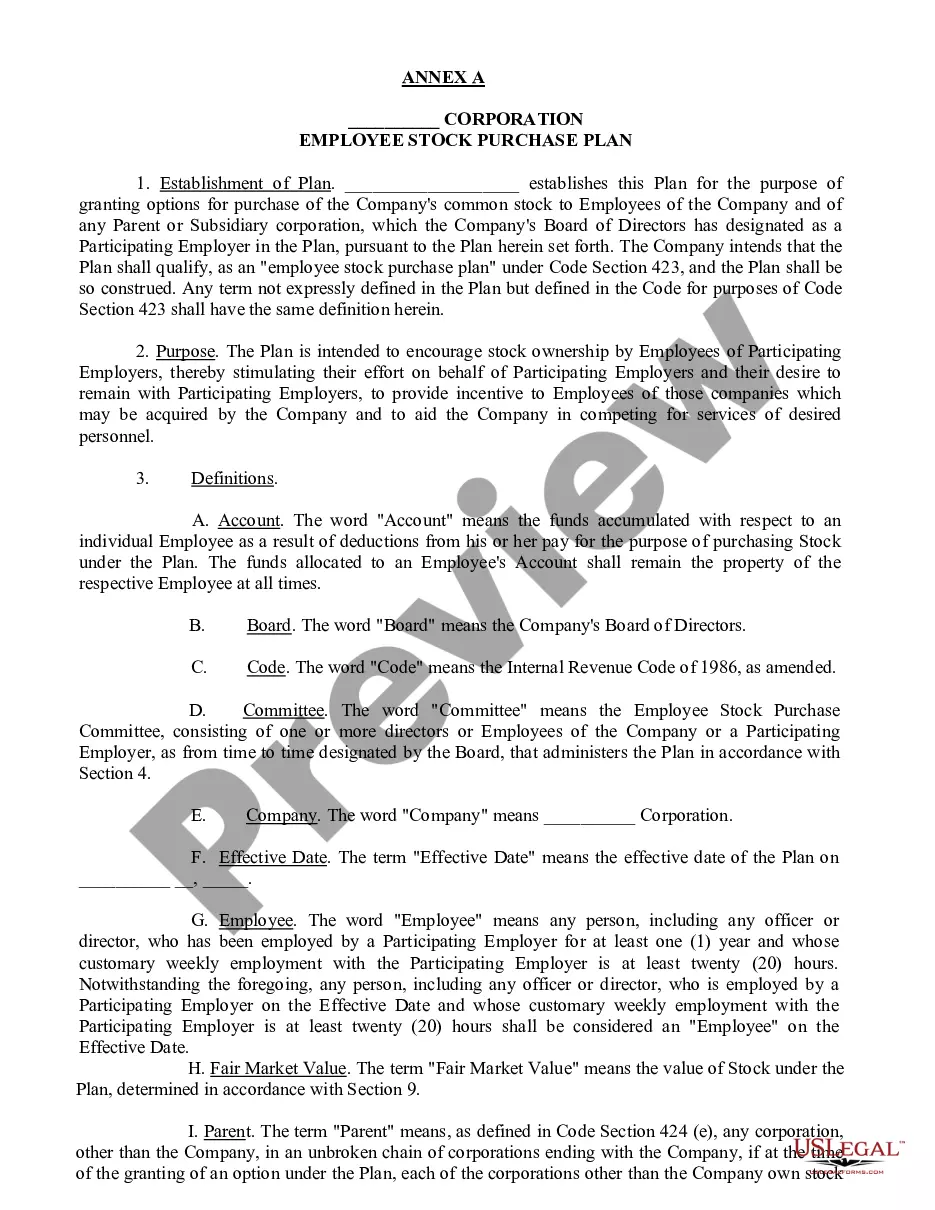

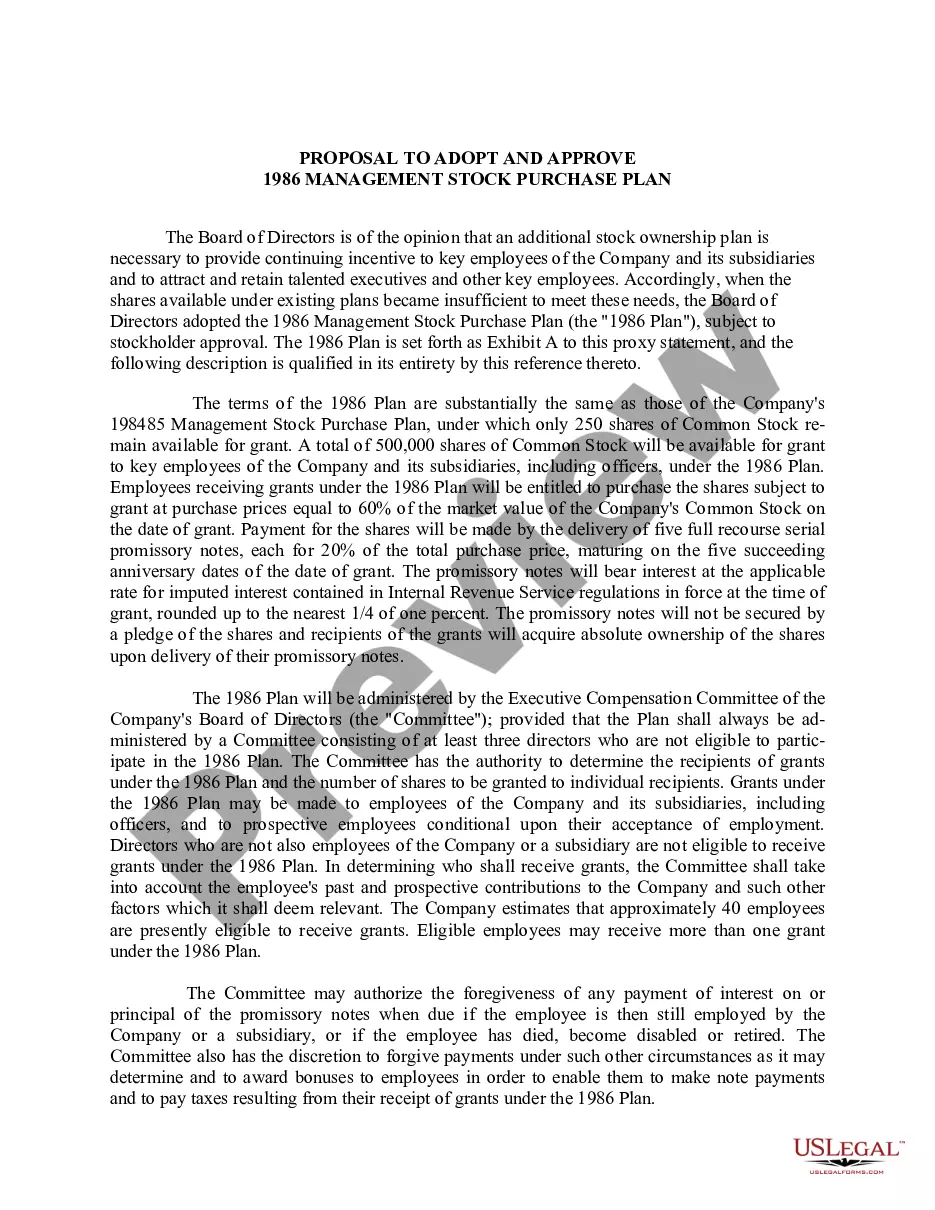

Pennsylvania Approval of Company Employee Stock Purchase Plan

Description

How to fill out Approval Of Company Employee Stock Purchase Plan?

You are able to commit hours on the Internet trying to find the legal document design which fits the federal and state requirements you want. US Legal Forms provides a large number of legal varieties that happen to be analyzed by pros. You can actually acquire or produce the Pennsylvania Approval of Company Employee Stock Purchase Plan from my assistance.

If you already have a US Legal Forms bank account, you may log in and then click the Down load switch. Following that, you may total, revise, produce, or signal the Pennsylvania Approval of Company Employee Stock Purchase Plan. Every single legal document design you acquire is yours forever. To acquire another copy for any obtained kind, proceed to the My Forms tab and then click the corresponding switch.

Should you use the US Legal Forms website initially, adhere to the easy directions listed below:

- Initial, ensure that you have selected the best document design for that state/town of your choice. Browse the kind outline to ensure you have chosen the right kind. If offered, make use of the Preview switch to appear through the document design as well.

- If you wish to find another variation in the kind, make use of the Lookup field to get the design that meets your needs and requirements.

- Once you have identified the design you would like, simply click Acquire now to carry on.

- Find the pricing program you would like, type in your credentials, and sign up for a merchant account on US Legal Forms.

- Complete the deal. You may use your charge card or PayPal bank account to purchase the legal kind.

- Find the structure in the document and acquire it to the gadget.

- Make modifications to the document if needed. You are able to total, revise and signal and produce Pennsylvania Approval of Company Employee Stock Purchase Plan.

Down load and produce a large number of document layouts utilizing the US Legal Forms Internet site, which offers the greatest collection of legal varieties. Use skilled and state-specific layouts to tackle your business or individual needs.

Form popularity

FAQ

Employee Stock Purchase Plan: Qualified or Non-qualified Now, we can have a look at the key difference between the two types. An ESPP qualified plan is designed and operates ing to Internal Revenue Section (IRS) 423 regulations, whereas a non-qualified ESPP does not meet those criteria.

Employee Stock Purchase Plans (ESPPs) are widely regarded as one of the most simple and straightforward equity compensation strategies available to businesses today. There are two major types of ESPP: 1) Qualified ESPP offering tax advantages and 2) Non-qualified ESPP offering flexibility.

Qualifying disposition: You sold the stock at least two years after the offering (grant date) and at least one year after the exercise (purchase date). If so, a portion of the profit (the ?bargain element?) is considered compensation income (taxed at regular rates) on your Form 1040.

If your company offers a tax-qualified ESPP and you decide to participate, the IRS will only allow you to purchase a maximum of $25,000 worth of stock in a calendar year. Any contributions that exceed this amount are refunded back to you by your company.

Section 423 of the Code permits a plan to exclude employees who have been employed for less than two years or who are employed for less than 20 hours per week or five months per year. Also, owners of 5% or more of the common stock of a company by statute are not permitted to participate.

Below are our 10 key steps for creating, building and maintaining an ESPP: Determine the plan's purpose. ... Conduct external and internal research. ... Establish a budget. ... Pick the right components for the company. ... Seek stakeholder buy-in. ... Prepare early for shareholder approval. ... Select a provider. ... Create a robust implementation plan.

Once approved by the stockholders, an ESPP does not need to be approved by the stockholders again unless there is an amendment to the ESPP that would be considered the ?adoption of a new plan.? As a practical matter, this means a change in the number of shares reserved for issuance or a change in the related ...

Below are our 10 key steps for creating, building and maintaining an ESPP: Determine the plan's purpose. ... Conduct external and internal research. ... Establish a budget. ... Pick the right components for the company. ... Seek stakeholder buy-in. ... Prepare early for shareholder approval. ... Select a provider. ... Create a robust implementation plan.

An ESPP (employee stock purchase plan) allows employees to use after-tax wages to acquire their company's shares, usually at a discount of up to 15%. Quite commonly, companies offer a ''lookback'' feature in addition to the discount offered to make the plan more attractive.

Yes, you can sell stock purchased through your ESPP plan immediately if you want to guarantee that you profit from your discount. Otherwise, the value of the stock may go up, which increases your profit, or it may go down, causing you to lose money.