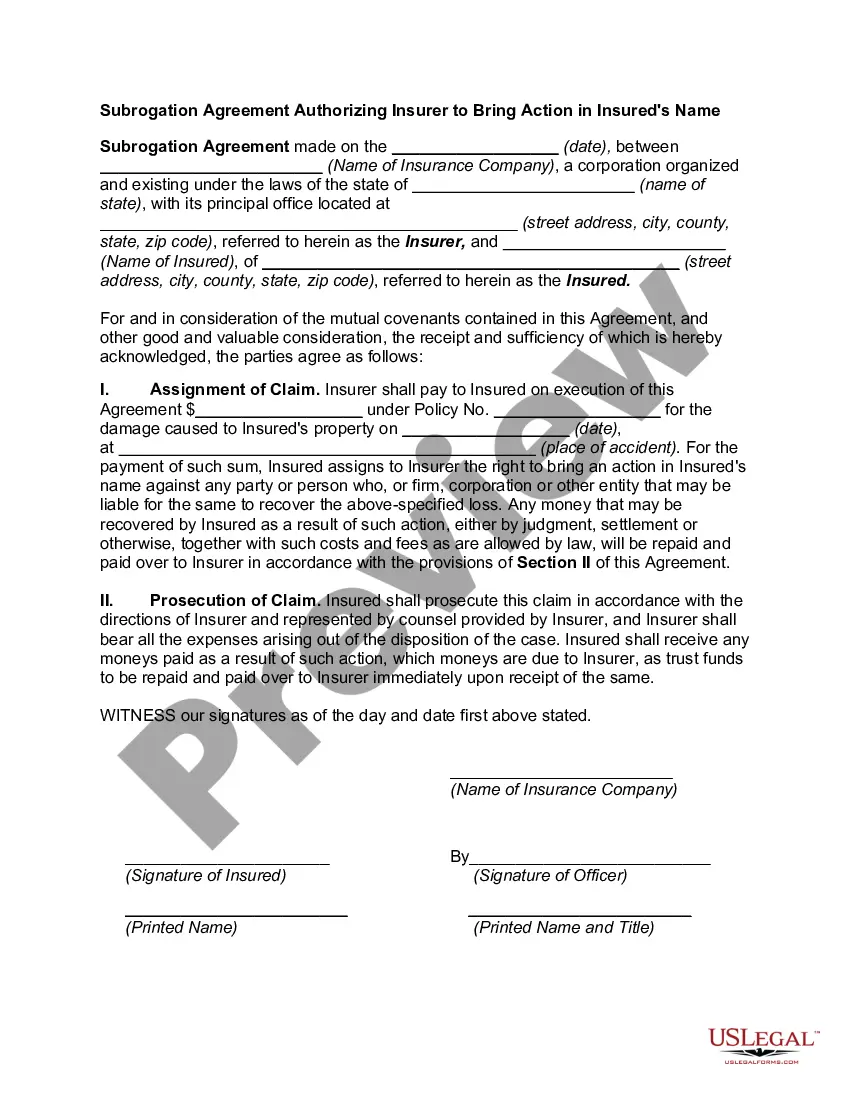

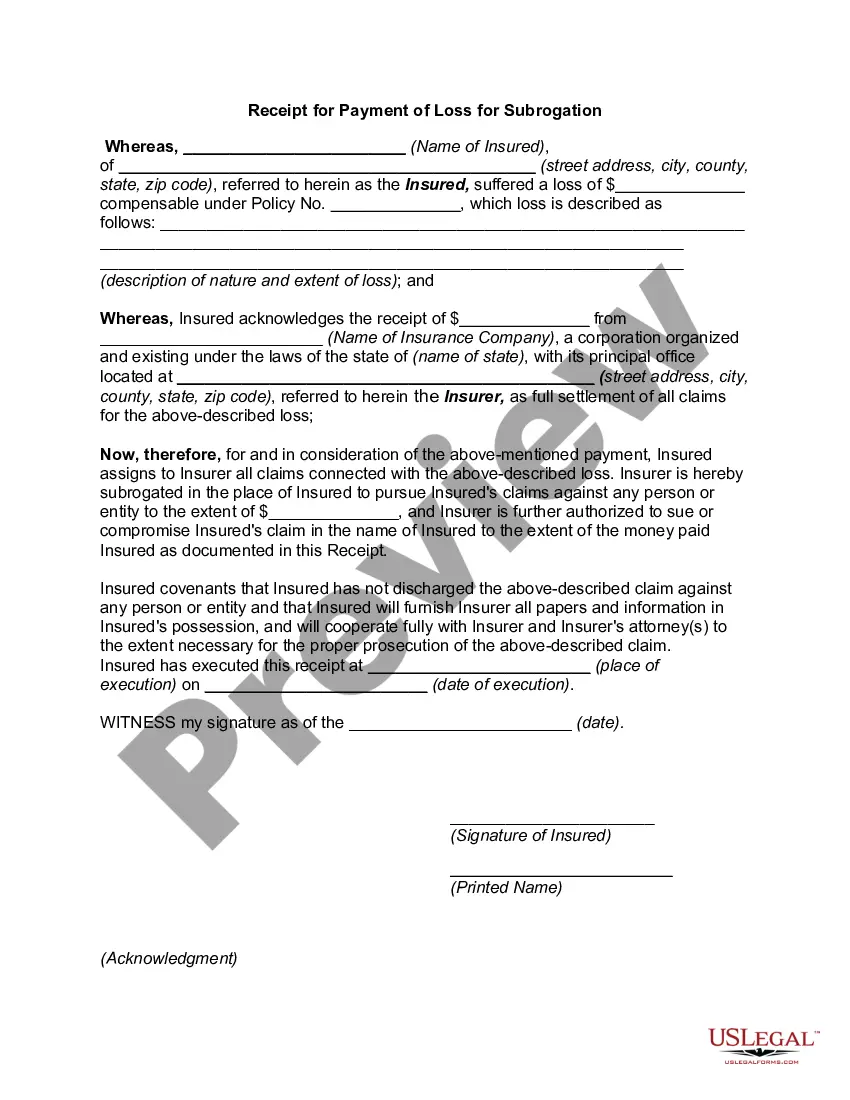

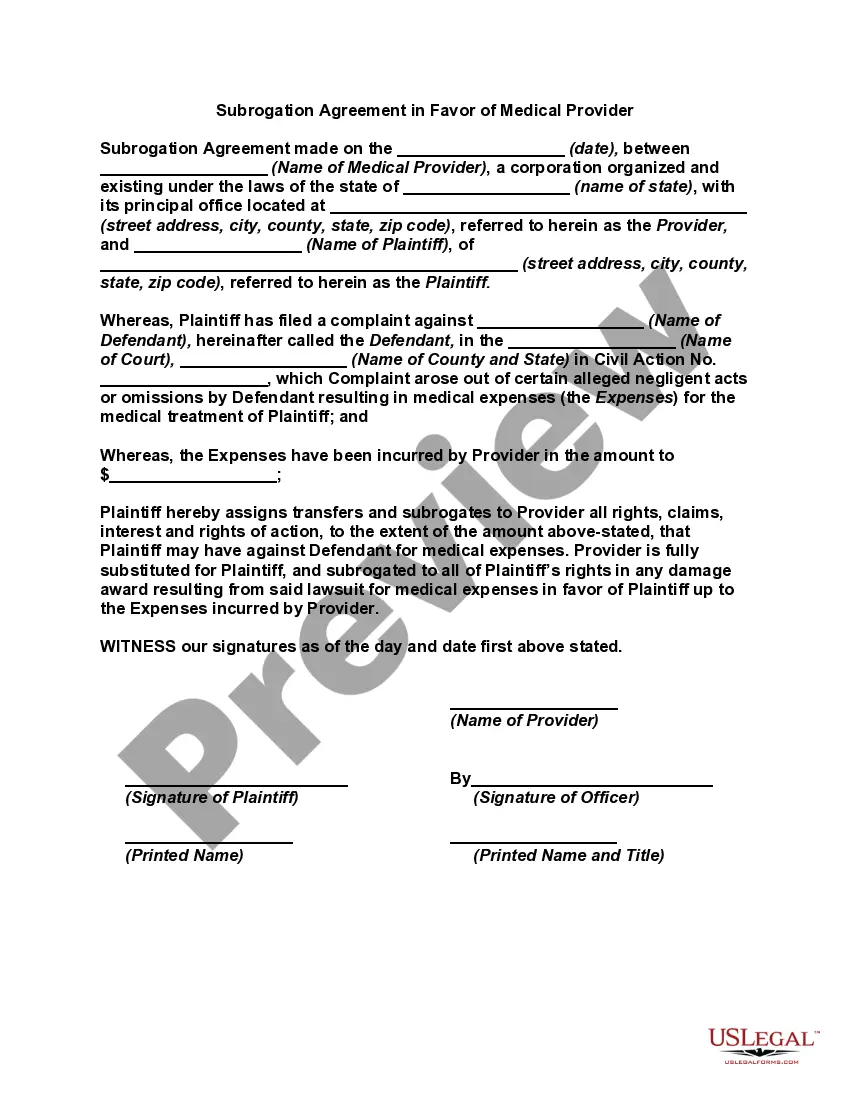

Pennsylvania Subrogation Agreement between Insurer and Insured

Description

How to fill out Subrogation Agreement Between Insurer And Insured?

Are you in the placement the place you need files for either organization or individual reasons just about every day? There are tons of legal document web templates available on the net, but locating versions you can rely is not simple. US Legal Forms gives a huge number of kind web templates, much like the Pennsylvania Subrogation Agreement between Insurer and Insured, that happen to be published to meet federal and state demands.

Should you be already familiar with US Legal Forms web site and possess a free account, merely log in. Next, you may obtain the Pennsylvania Subrogation Agreement between Insurer and Insured web template.

If you do not have an accounts and wish to begin to use US Legal Forms, abide by these steps:

- Find the kind you need and ensure it is for the proper town/state.

- Utilize the Review button to check the form.

- Read the information to ensure that you have selected the correct kind.

- When the kind is not what you are seeking, make use of the Search industry to discover the kind that meets your requirements and demands.

- Once you find the proper kind, click Buy now.

- Choose the costs plan you desire, fill out the desired details to make your account, and pay money for your order utilizing your PayPal or credit card.

- Decide on a practical file format and obtain your version.

Find every one of the document web templates you may have purchased in the My Forms food selection. You can obtain a additional version of Pennsylvania Subrogation Agreement between Insurer and Insured whenever, if possible. Just click on the needed kind to obtain or produce the document web template.

Use US Legal Forms, by far the most considerable assortment of legal forms, in order to save some time and stay away from errors. The service gives appropriately created legal document web templates that you can use for a range of reasons. Generate a free account on US Legal Forms and start making your way of life a little easier.

Form popularity

FAQ

An insurer may attempt to subrogate against an additional insured for completed operations injuries caused by the insured if the additional insured endorsement provides coverage only for ongoing operations injuries.

At Hiscox, the additional named insured and the named insured both have full rights under the policy. The named insured is the one who is responsible for paying the premiums, and who can cancel the policy. The additional named insured doesn't have those obligations to the insurer.

If an injured worker prevails in their third-party case, the employer's workers' compensation carrier may collect repayment for the benefits it paid out in a process called subrogation. Damages awarded to the injured employee by the workers' compensation insurer can be partly recuperated.

Insurance companies argue that the additional insured endorsement is designed to cover only that vicarious liability. If the general contractor was independently negligent, insurance companies argue that the liability for that independent negligence should not be covered by the additional insured endorsement.

"Subrogation," or "subro" for short, refers to the right your insurance company holds under your policy ? after they've paid a covered claim ? to request reimbursement from the at-fault party. This reimbursement often comes from the at-fault party's insurance company.

An additional insured extends liability insurance coverage beyond the named insured to include other individuals or groups. An additional insured endorsement protects the additional insured under the named insurer's policy allowing them to file a claim if sued.

An insurance company may not subrogate against its own insured or a co-insured. However, when a party claiming to be a co-insured is merely a loss payee to which no liability coverage is afforded, subrogation is permissible.