The Truth-in-Lending Act (TILA) is part of the Federal Consumer Credit Protection Act. The purpose of the TILA is to make full disclosure to debtors of what they are being charged for the credit they are receiving. The Act merely asks lenders to be honest to the debtors and not cover up what they are paying for the credit. Regulation Z is a federal regulation prepared by the Federal Reserve Board to carry out the details of the Act. TILA applies to consumer credit transactions. Consumer credit is credit for personal or household use and not commercial use.

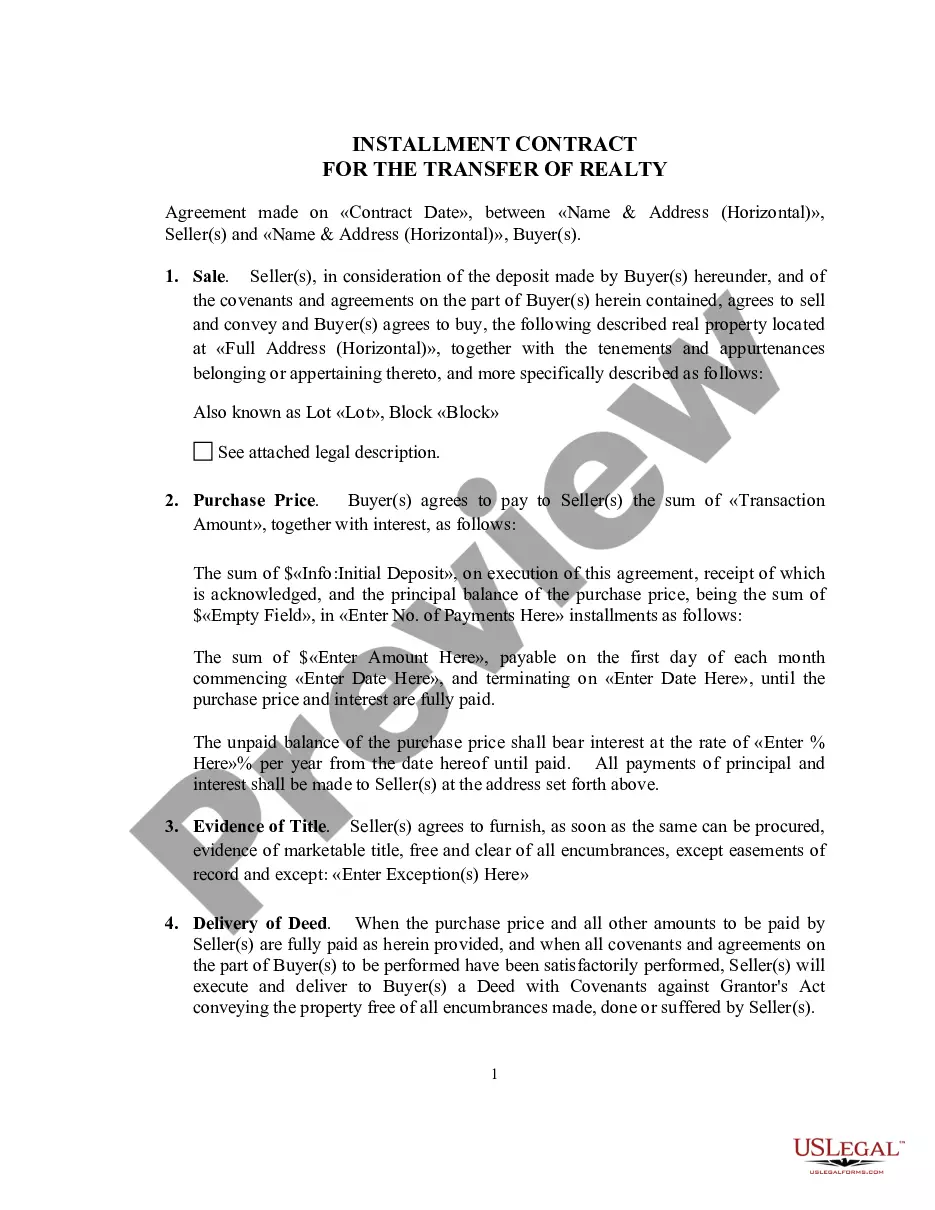

Closed-end transactions involve a fixed amount to be paid back over a period of time such as a note or a retail installment contract.

Pennsylvania General Disclosures Required By The Federal Truth In Lending Act - Retail Installment Contract - Closed End Disclosures

Category:

State:

Multi-State

Control #:

US-02514BG

Format:

Word;

PDF;

Rich Text

Instant download

Description

Free preview

How to fill out General Disclosures Required By The Federal Truth In Lending Act - Retail Installment Contract - Closed End Disclosures?

Selecting the correct licensed document template can be challenging.

Surely, there exists a wide range of designs available online, but how can you find the legal document you require.

Utilize the US Legal Forms website.

If you are a new user of US Legal Forms, here are simple instructions that you can follow.

- The platform offers numerous templates, including the Pennsylvania General Disclosures Required By The Federal Truth In Lending Act - Retail Installment Contract - Closed End Disclosures, which you can utilize for both business and personal needs.

- All documents are reviewed by experts and comply with state and federal regulations.

- If you are already registered, Log In to your account and click the Download option to obtain the Pennsylvania General Disclosures Required By The Federal Truth In Lending Act - Retail Installment Contract - Closed End Disclosures.

- Use your account to browse through the legal forms you have previously obtained.

- Visit the My documents section of your account and acquire another copy of the documents you need.

Form popularity

FAQ

You must provide the consumer with the account disclosures when they apply for a retail installment contract. This requirement, rooted in the Pennsylvania General Disclosures Required By The Federal Truth In Lending Act - Retail Installment Contract - Closed End Disclosures, ensures that consumers understand the terms and conditions of their agreement before finalizing the transaction. Timely disclosure helps consumers make informed decisions, avoiding any confusion or misunderstandings.

In Pennsylvania, a contract is considered legal when it includes an offer, acceptance, and consideration, meaning something of value is exchanged. Additionally, all parties involved must have the legal capacity to enter into the agreement, which includes being of sound mind and legal age. Understanding these elements is important for consumers navigating the Pennsylvania General Disclosures Required By The Federal Truth In Lending Act - Retail Installment Contract - Closed End Disclosures.

Regulation Z mandates that all material closed-end credit disclosures must be clearly formatted and easily understandable. Lenders are required to present this information in a conspicuous manner to avoid confusion. Meeting these standards is essential for compliance with the Pennsylvania General Disclosures Required By The Federal Truth In Lending Act - Retail Installment Contract - Closed End Disclosures.

In the Pennsylvania General Disclosures Required By The Federal Truth In Lending Act - Retail Installment Contract - Closed End Disclosures, lenders must disclose various key items. These include the annual percentage rate (APR), finance charges, total payments, and payment schedule. Transparency is crucial, as these disclosures help borrowers understand their financial commitments.

A Retail Installment Sales Financing Act is a state law that governs retail installment contracts. A retail installment contract is one where the lender maintains title to the property, such as a car, and the borrower has use of the property and makes regular installment payments toward the purchase of the property.

A retail agreement is a legal contract between a manufacturer or wholesaler of a product and the retail business that will sell the product to customers. Frequently these agreements are used to set pricing expectations and establish minimum inventory and order amounts.

Understanding a Purchase Contract. A retail installment sale is a transaction between you and a dealer to purchase a vehicle where, you agree to pay the dealer over time, paying both the value of the vehicle plus interest. A dealer can sell the retail installment contract to a lender or other party.

A retail installment sales contract agreement is slightly different from a loan. Both are ways for you to obtain a vehicle by agreeing to make payments over time. In both, you are generally bound to the agreement after signing.

A retail contract, also known as a retail purchase agreement, is an agreement outlining the details of a transaction of retail goods between a buyer and a seller.

An installment purchase agreement is a contract used to finance the acquisition of assets. Under the terms of such an agreement, the buyer pays the seller the full purchase price by making a series of partial payments over time. The payments include stated or imputed interest.