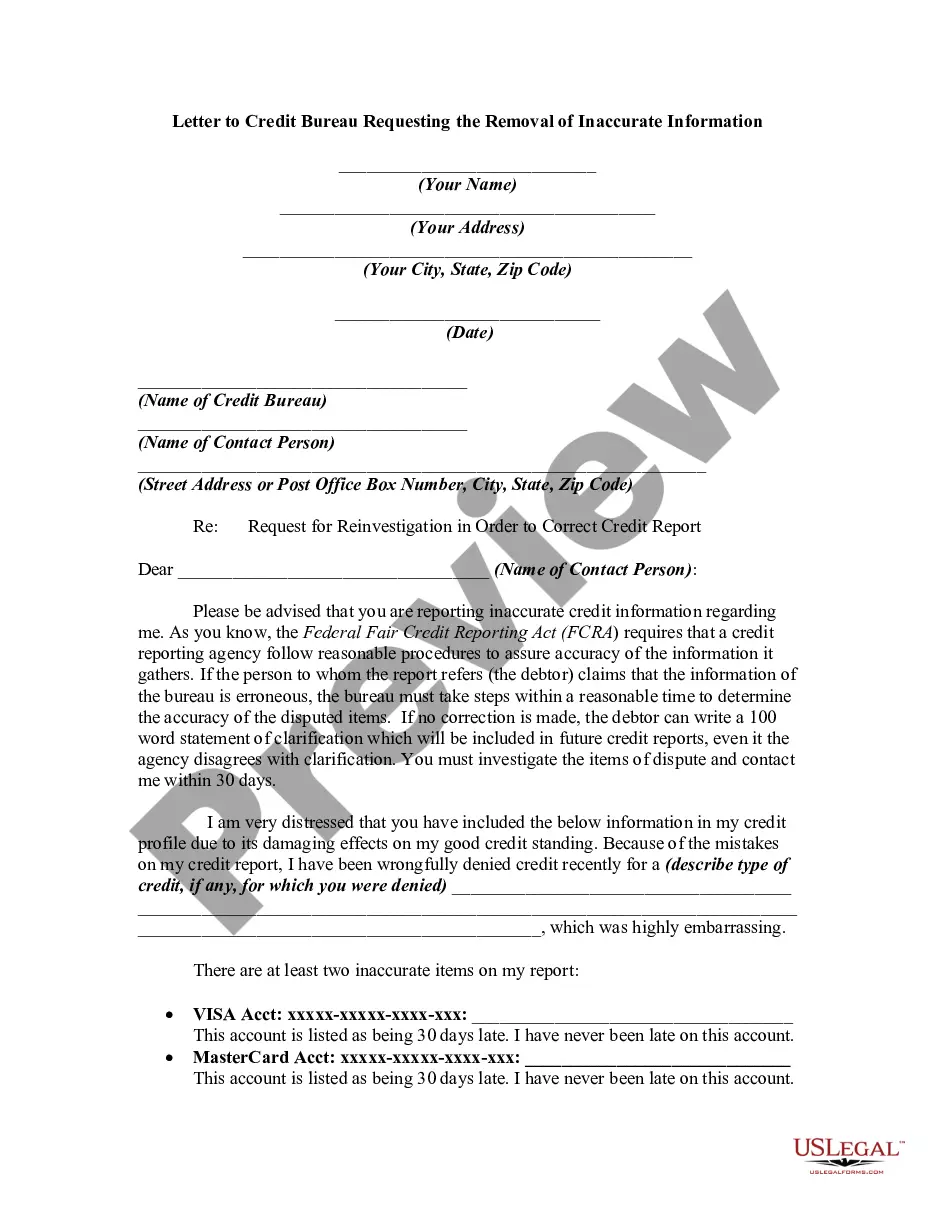

Some information obtained by credit reporting bureaus is based on statements made by persons, such as neighbors who were interviewed by the bureau's investigator. Needless to say, these statements are not always correct and are sometimes the result of gossip. In any event, such statements may go on the records of the bureau without further verification and may be furnished to a client of the bureau who will regard the statements as accurate. A person has the limited right to request an agency to disclose the nature and substance of the information possessed by the bureau to see if the information is accurate. If the person claims that the information of the bureau is erroneous, the bureau must take steps within a reasonable time to determine the accuracy of the disputed items.

Pennsylvania Letter from Consumer to Credit Reporting Agency Disputing Information in File

Description

How to fill out Letter From Consumer To Credit Reporting Agency Disputing Information In File?

You can spend time on-line attempting to find the legal papers web template which fits the state and federal specifications you need. US Legal Forms provides a large number of legal varieties that are evaluated by specialists. It is simple to download or print out the Pennsylvania Letter from Consumer to Credit Reporting Agency Disputing Information in File from our assistance.

If you already possess a US Legal Forms bank account, you are able to log in and then click the Down load option. After that, you are able to complete, modify, print out, or indicator the Pennsylvania Letter from Consumer to Credit Reporting Agency Disputing Information in File. Every single legal papers web template you acquire is yours for a long time. To have an additional copy of the obtained type, check out the My Forms tab and then click the related option.

If you use the US Legal Forms internet site the very first time, keep to the straightforward directions under:

- Very first, be sure that you have chosen the best papers web template for the state/town that you pick. Read the type information to make sure you have picked the correct type. If readily available, take advantage of the Review option to look throughout the papers web template at the same time.

- In order to locate an additional edition from the type, take advantage of the Research industry to get the web template that suits you and specifications.

- After you have found the web template you want, click on Acquire now to proceed.

- Choose the pricing plan you want, key in your qualifications, and register for a merchant account on US Legal Forms.

- Total the transaction. You may use your bank card or PayPal bank account to purchase the legal type.

- Choose the formatting from the papers and download it to your device.

- Make changes to your papers if needed. You can complete, modify and indicator and print out Pennsylvania Letter from Consumer to Credit Reporting Agency Disputing Information in File.

Down load and print out a large number of papers templates utilizing the US Legal Forms web site, which offers the greatest assortment of legal varieties. Use skilled and state-certain templates to tackle your organization or individual requirements.

Form popularity

FAQ

Asked by: Mr. Jillian Rau | Last update: February 9, 2022 Score: 4.1/5 (71 votes) Section 623 of the FRCA allows you to dispute any inaccurate information on your credit report directly with the original creditor, as long as you've already completed the process with the credit bureau.

The 623 dispute method allows you to dispute any inaccurate information on your credit report directly with the original creditor.

A 609 dispute letter points out some inaccurate, negative, or erroneous information on your credit report, forcing the credit company to change them. You'll find countless 609 letter templates online; however, they do not always promise that your dispute will be successful.

2) Do dispute letters work? Dispute letters are the most effective way to correct errors on your credit report. It also makes the credit bureau obligated by law to investigate your issue. Yet, a dispute letter doesn't ensure that your credit score will improve unless you have strong evidence backing your claim.

But they have different purposes, and only Section 609 will support a dispute letter. Under the FCRA, Section 604 defines the circumstances under which a consumer reporting agency may furnish a consumer report. This section is titled ?Permissible purposes of consumer reports.?

A business uses a 623 credit dispute letter when all other attempts to remove dispute information have failed. It refers to Section 623 of the Fair Credit Reporting Act and contacts the data furnisher to prove that a debt belongs to the company.

I am requesting that this item be removed [or request another specific change to correct the information]. [List and describe any other items you are disputing.] Enclosed is documentation supporting my request: [describe the documents you're sending, for instance: my credit report, with the disputed items circled.]

Are 609 letters effective? There's no evidence to suggest a 609 letter is more or less effective than the usual process of disputing an error on your credit report?it's just another method of gathering information and seeking verification of the accuracy of the report.