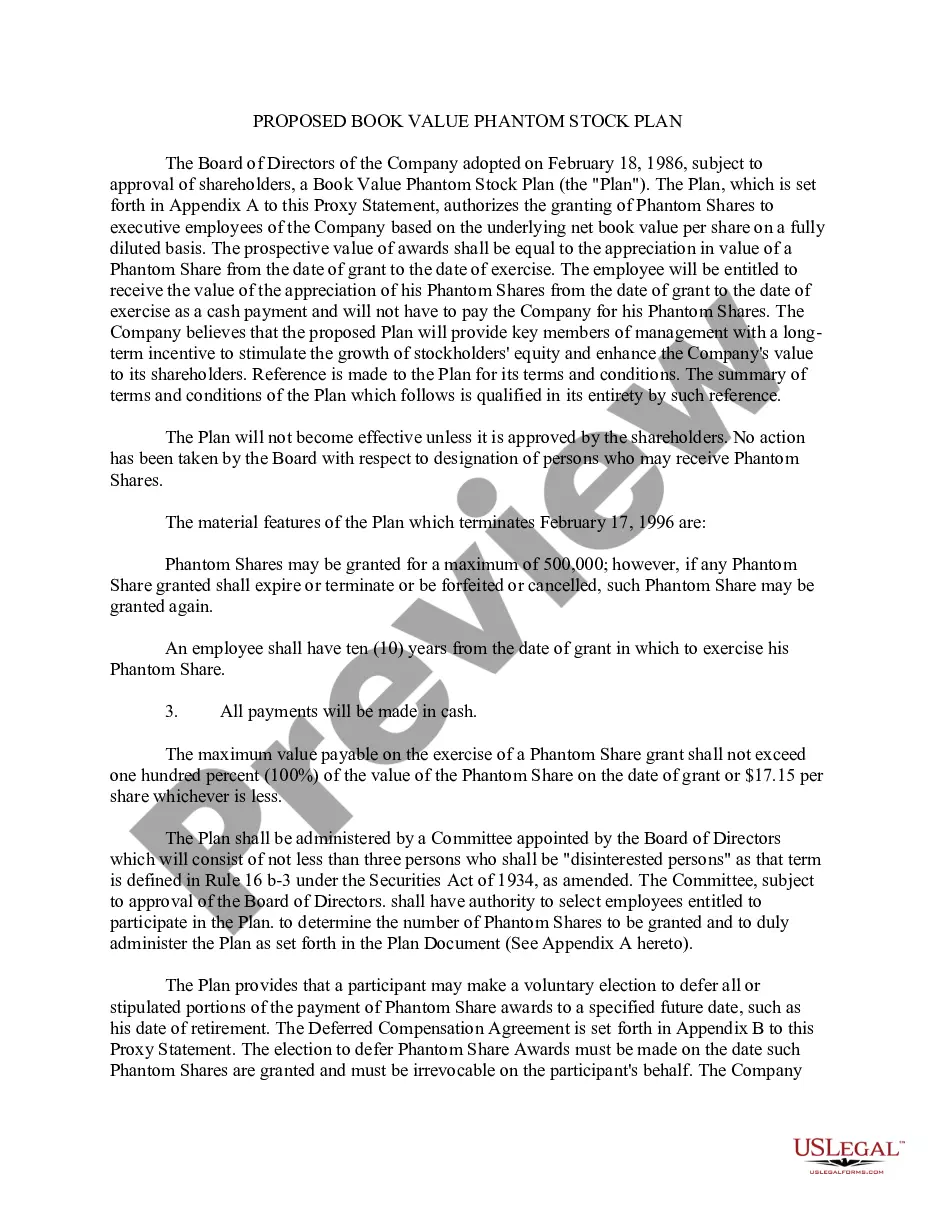

20-162A 20-162A . . . Book Value Phantom Stock Plan under which Committee of Board of Directors may, from time to time, grant quantity of phantom shares to selected employees, each share being equivalent to one share of corporation common stock. Phantom shares may be exercised at any time within ten years of date of grant (subject to certain limitations in event of termination of employment) Upon exercise, employee is paid cash equal to increase in underlying net book value per share on fully diluted basis of shares between date of grant and date of exercise

Oregon Book Value Phantom Stock Plan of First Florida Banks, Inc.

State:

Multi-State

Control #:

US-CC-20-162A

Format:

Word;

Rich Text

Instant download

Description

Free preview

How to fill out Book Value Phantom Stock Plan Of First Florida Banks, Inc.?

Are you currently inside a place that you require documents for possibly company or personal uses nearly every time? There are a variety of legal document themes available on the Internet, but getting versions you can depend on isn`t effortless. US Legal Forms offers a huge number of type themes, just like the Oregon Book Value Phantom Stock Plan of First Florida Banks, Inc., that happen to be written to meet state and federal needs.

In case you are currently acquainted with US Legal Forms web site and possess a merchant account, just log in. Afterward, it is possible to acquire the Oregon Book Value Phantom Stock Plan of First Florida Banks, Inc. template.

If you do not come with an account and wish to begin using US Legal Forms, abide by these steps:

- Discover the type you will need and make sure it is for the right city/area.

- Make use of the Review switch to examine the form.

- Read the explanation to ensure that you have chosen the appropriate type.

- In case the type isn`t what you are trying to find, use the Look for discipline to discover the type that meets your requirements and needs.

- If you obtain the right type, click on Get now.

- Choose the prices plan you would like, fill out the necessary information to make your bank account, and buy the transaction making use of your PayPal or Visa or Mastercard.

- Pick a convenient paper formatting and acquire your backup.

Discover each of the document themes you possess purchased in the My Forms food list. You can get a further backup of Oregon Book Value Phantom Stock Plan of First Florida Banks, Inc. whenever, if necessary. Just click on the essential type to acquire or print out the document template.

Use US Legal Forms, the most extensive selection of legal varieties, to save time as well as stay away from blunders. The support offers skillfully created legal document themes that can be used for an array of uses. Generate a merchant account on US Legal Forms and commence producing your daily life easier.

Form popularity

FAQ

How Phantom Stock Plans Are Taxed. Payments from phantom stock plans are subject to typical income taxes, not capital gains taxes. In turn, companies can deduct phantom plan payouts the year the employee reports the income.

The answer involves two variables: (a) the presumed value of the company, and (b) the number of shares to be used in the plan. Once these two answers are known, the phantom share price is calculated as the former (the value) divided by the latter (the number of shares).

Phantom stock plans are considered ?liability awards? for accounting purposes (assuming they will be settled in cash rather than stock).

Phantom stock plans are considered ?liability awards? for accounting purposes (assuming they will be settled in cash rather than stock). As such, the sponsoring company must recognize the plan expense ratably over the vesting period. Varying accrual schedules can be found in the market.

A cash payment from Company A as the difference between the current common share price and phantom stock issue price: ($70 ? $50) x 500 = $10,000; or. A cash payment from Company A equal to the current common share price: $50 x 500 = $25,000.

Qualified plans, such as 401(k) programs, are subject to all of the rules and restrictions of ERISA. Nonqualified plans, including most phantom stock plans, are not.

Phantom shares are usually paid out when the company gets acquired or IPOes. The phantom shares are paid out in cash for their corresponding value.

As a default, this form plan provides for forfeiture of all unvested phantom stock units upon a participant's termination of employment (subject to the terms of the award agreement).

The definition of Exit Event used in this form phantom plan complies with Section 409A as the plan is designed so that awards are settled upon an Exit Event or, if earlier, a termination of a participant's employment, which is also a permissible payment event for purposes of Section 409A.

If a business is sold, employees that own phantom stock receive money that is equal to the amount they would have received had they owned actual stock in the company. For that reason, it's financially beneficial to employees to own phantom stock, as they don't need to worry about dilution.