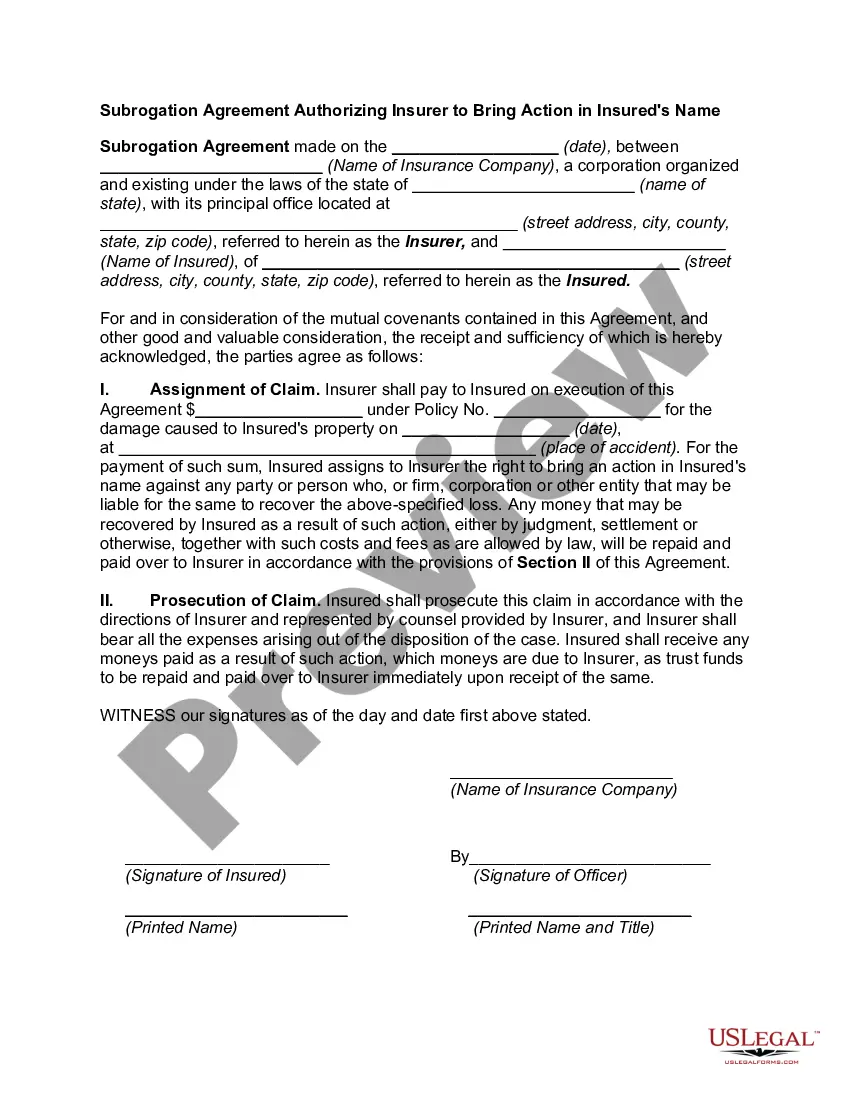

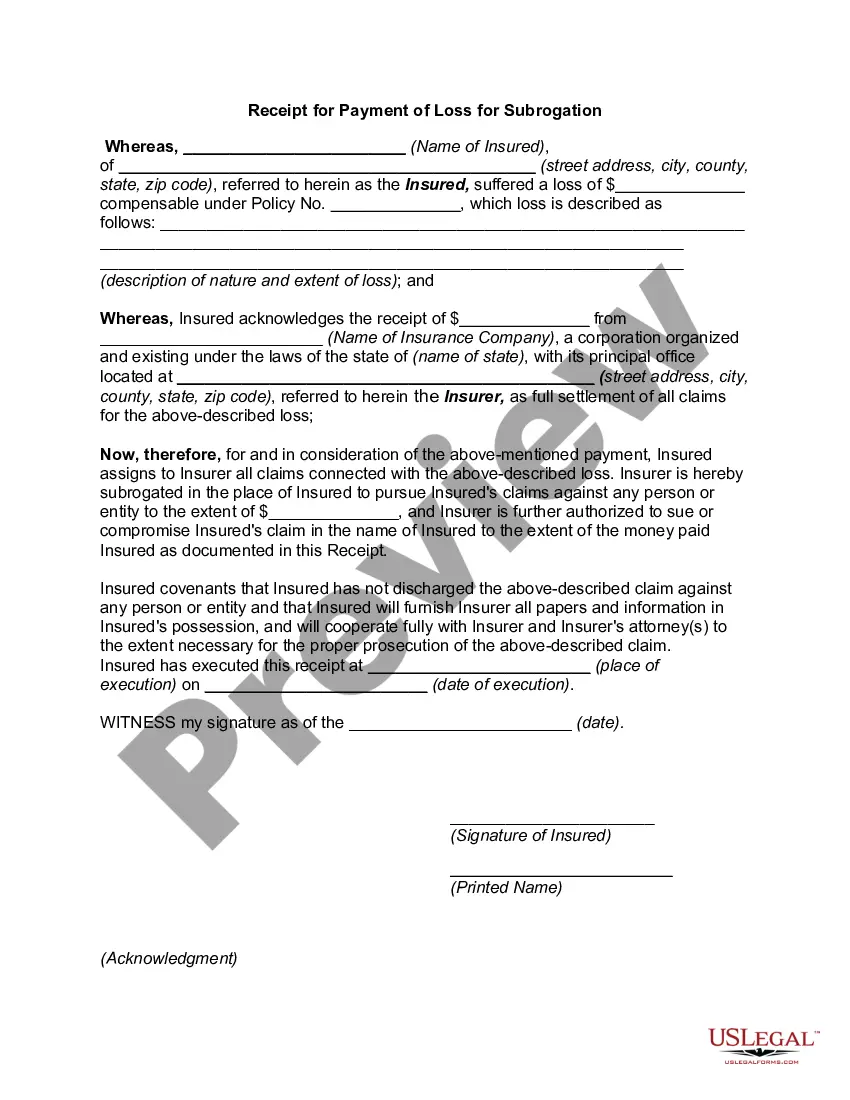

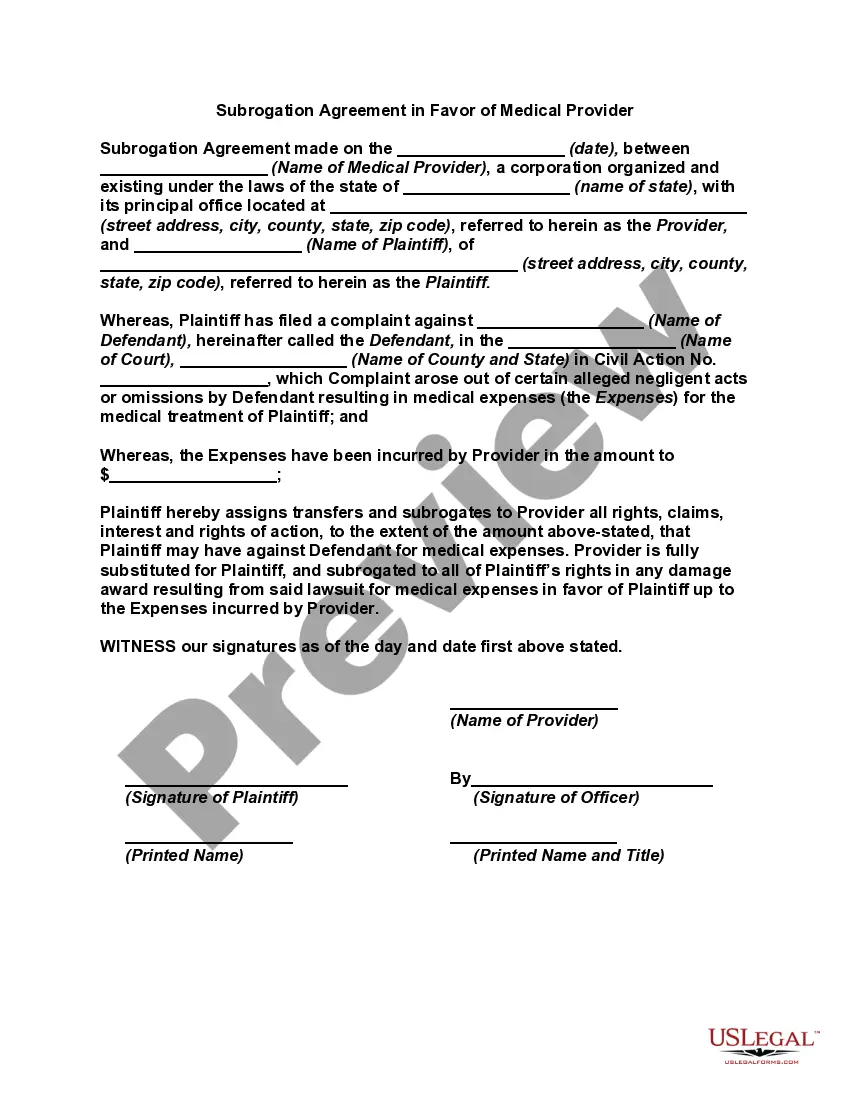

Oregon Subrogation Agreement between Insurer and Insured

Description

How to fill out Subrogation Agreement Between Insurer And Insured?

Have you been in the position where you need to have papers for sometimes enterprise or individual purposes nearly every day? There are a variety of legitimate document themes accessible on the Internet, but finding kinds you can rely is not easy. US Legal Forms offers thousands of kind themes, just like the Oregon Subrogation Agreement between Insurer and Insured, which can be composed to fulfill federal and state demands.

When you are previously acquainted with US Legal Forms web site and possess an account, simply log in. Following that, you may acquire the Oregon Subrogation Agreement between Insurer and Insured template.

Unless you offer an bank account and need to start using US Legal Forms, abide by these steps:

- Obtain the kind you will need and ensure it is to the right area/region.

- Make use of the Review button to check the form.

- Look at the description to ensure that you have selected the appropriate kind.

- When the kind is not what you`re trying to find, use the Research area to find the kind that meets your requirements and demands.

- Whenever you obtain the right kind, click on Get now.

- Select the pricing prepare you want, complete the required information and facts to generate your account, and purchase the order using your PayPal or Visa or Mastercard.

- Select a handy document file format and acquire your version.

Locate every one of the document themes you possess bought in the My Forms menu. You can aquire a additional version of Oregon Subrogation Agreement between Insurer and Insured any time, if necessary. Just go through the needed kind to acquire or print the document template.

Use US Legal Forms, the most considerable variety of legitimate varieties, to save lots of time as well as avoid mistakes. The assistance offers skillfully created legitimate document themes which you can use for a variety of purposes. Create an account on US Legal Forms and start making your way of life easier.

Form popularity

FAQ

This right is called subrogation and is an equitable doctrine. A person can satisfy his/her loss that is created by the wrongful act or omission of another person by stepping into the shoes of another and recovering on the claim from the wrongdoer.

An insurer may attempt to subrogate against an additional insured for completed operations injuries caused by the insured if the additional insured endorsement provides coverage only for ongoing operations injuries.

O.R.S. § 742.538 is the ?subrogation statute.? This traditional right of recovery by subrogation is available only if the auto policy contains the necessary subrogation language, the insurer has not elected to recover by lien under § 742.536, above, and the inter-insurer reimbursement is not available under O.R.S.

An insurance company may not subrogate against its own insured or a co-insured. However, when a party claiming to be a co-insured is merely a loss payee to which no liability coverage is afforded, subrogation is permissible.

"Subrogation," or "subro" for short, refers to the right your insurance company holds under your policy ? after they've paid a covered claim ? to request reimbursement from the at-fault party. This reimbursement often comes from the at-fault party's insurance company.

Simply put, subrogation protects you and your insurer from paying for losses that aren't your fault. It's common in auto, health insurance and homeowners policies. It lets your insurer pursue the person at fault to recover the money paid out for a claim that wasn't your fault.

Subrogation, in the legal context, refers to when one party takes on the legal rights of another, especially substituting one creditor for another. Subrogation can also occur when one party takes over another's right to sue.

When factoring comparative negligence and improper referrals, the recovery rate should be somewhere in the range of 85-90%. This requires adjusters properly identifying subrogation, assessing comparative negligence and pursuing only what they are entitled to.