Oklahoma Closing Statement

Understanding this form

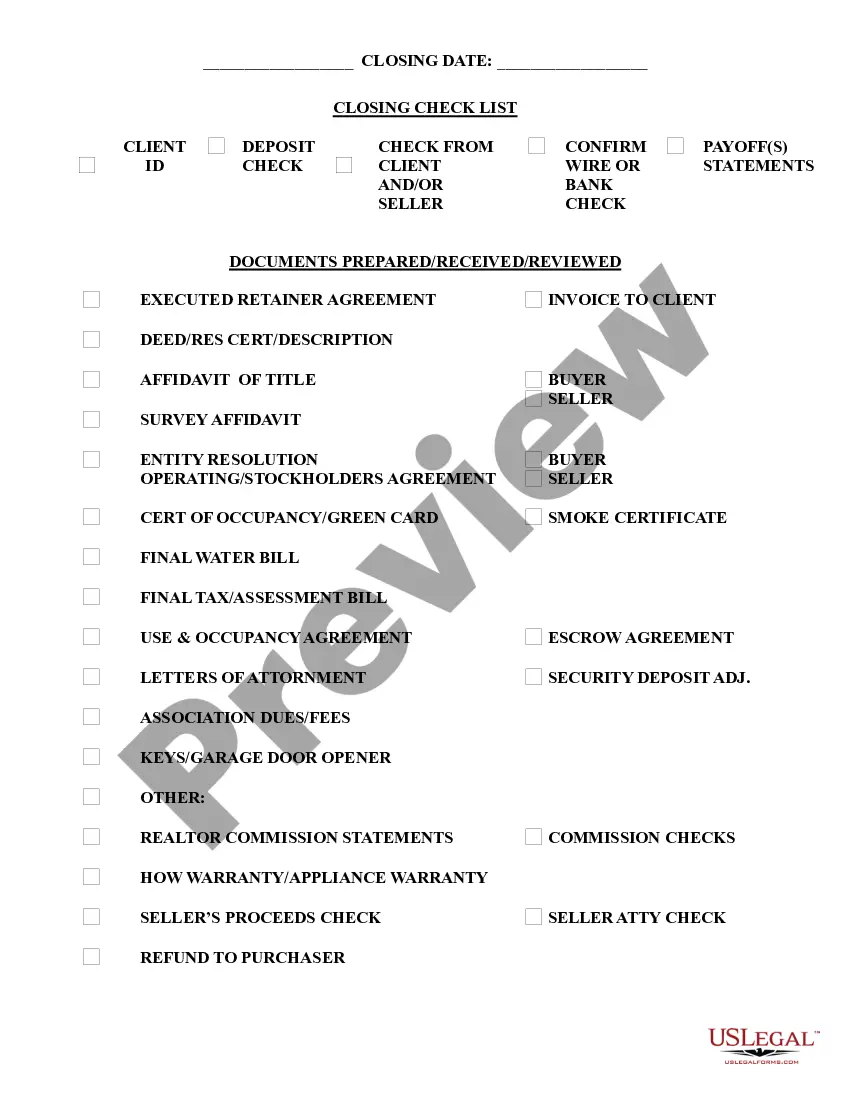

The Closing Statement is an essential document for real estate transactions, particularly when the sale is conducted as a cash transaction or involves owner financing. This form serves to summarize all financial aspects of the sale, detailing expenses, adjustments, and the final amounts due between the buyer and seller. Unlike other real estate documents, the Closing Statement is specifically focused on the financial settlement of the transaction and requires signatures from both parties to verify its accuracy and finality.

Key components of this form

- Balance calculations for both seller and buyer.

- Detailed listing of expenses such as title search, recording fees, and attorney fees.

- Pro rata adjustments for county and city taxes.

- Total adjustment calculations that reflect changes in the financial balance.

- Certification section where both parties confirm the accuracy of the statement.

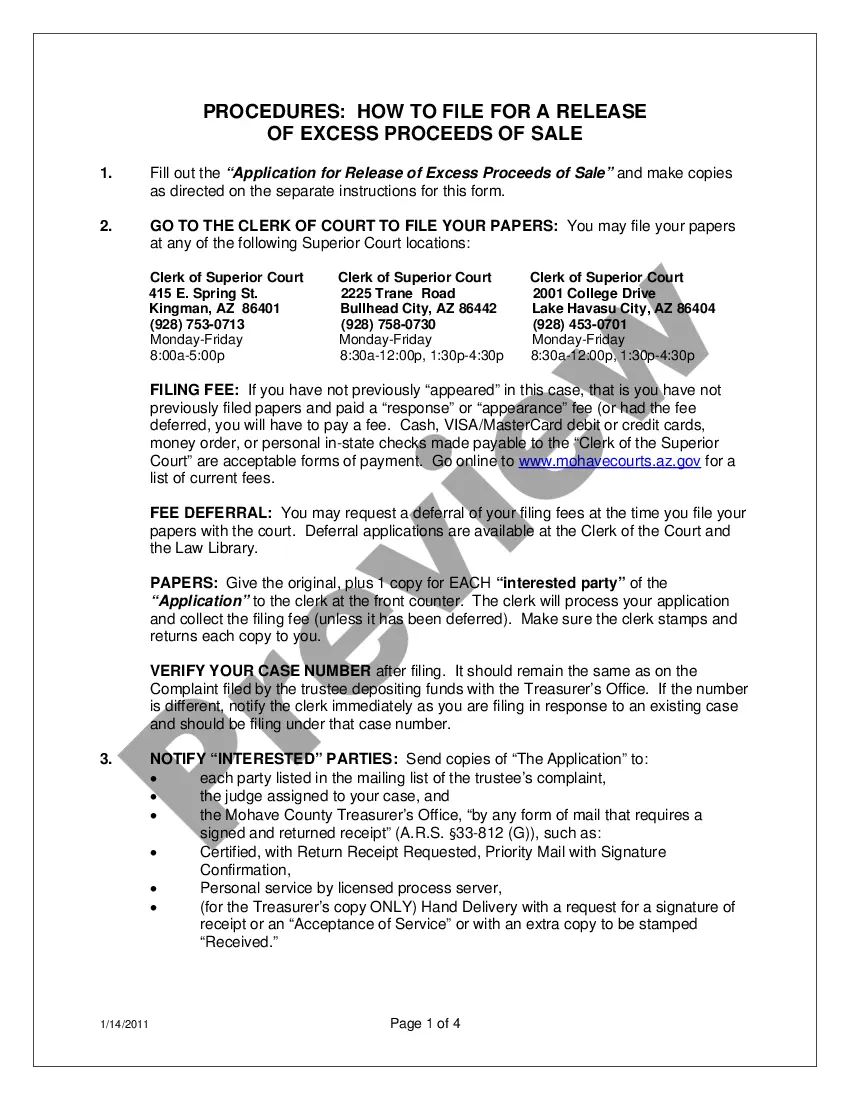

When this form is needed

This Closing Statement should be used during the finalization of a real estate sale, particularly when the transaction is a cash sale or involves owner financing. It is often used at the closing meeting, where buyers and sellers finalize their agreement and settle financial obligations. This form ensures all financial details are transparent and agreed upon before the transaction is completed.

Who should use this form

This form is intended for:

- Property sellers and buyers engaged in a cash sale or owner financing arrangement.

- Real estate professionals, such as agents and brokers, assisting clients through the transaction process.

- Attorneys representing either the buyer or seller during real estate transactions.

Steps to complete this form

- Identify the parties involved in the transaction, including the seller and the buyer.

- List all expenses associated with the sale, such as title search and recording fees, in their respective fields.

- Calculate total expenses and adjustments to determine the final balance due to or from each party.

- Ensure all parties review the statement for accuracy and sign the certification section.

- Keep a copy of the completed statement for your records after signing.

Is notarization required?

This document requires notarization to meet legal standards. US Legal Forms provides secure online notarization powered by Notarize, allowing you to complete the process through a verified video call, available 24/7.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Typical mistakes to avoid

- Forgetting to include all relevant expenses leading to an inaccurate total.

- Failing to double-check calculations for balance, leading to potential disputes.

- Omitting signatures from one or both parties on the certification section.

- Not keeping copies of the signed document for personal records.

Why complete this form online

- Convenient downloadable format allows for quick access when needed.

- Editability lets users customize the form according to their specific transaction needs.

- Reliability ensured by documents prepared with input from licensed attorneys.

Summary of main points

- The Closing Statement summarizes all financial details of a real estate transaction.

- It is crucial for both parties to sign and certify the accuracy of the document.

- Using this form helps ensure transparency and prevents future disputes over financial obligations.

Looking for another form?

Form popularity

FAQ

The Mortgage Promissory Note. The Mortgage / Deed of Trust / Security Instrument. The deed (for property transfer). The Closing Disclosure. The initial escrow disclosure statement. The transfer tax declaration (in some states)

A settlement statement is also known as a HUD-1 form or a closing statement. Until 2015, when the rules changed, this form was provided twice. First, within three business days of applying for a mortgage loan, the borrower receives one in the mail with the person's estimated closing costs.

A closing agent prepares the closing statement, which is settlement sheet. It's a comprehensive list of every expense that the buyer and seller must pay to complete the real estate transaction. Fees listed on this sheet include commissions, mortgage insurance, and property tax deposits.

The HUD-1 settlement statement. The closing agent prepares this accounting of all the money involved in the transaction. Certificate of title. The deed. Loan payoff. Mechanic's liens. Bill of sale. Statement of closing costs. Statement of information.

The most important originals are the purchase agreement, deed, and deed of trust or mortgage. In the event originals are destroyed, you might be able to get certified copies of these documents from the lender or closing company, but you don't want to rely on others' recordkeeping systems unless you have to.

Double-check the loan amount, loan type, loan term, interest rate, monthly payment amount, whether there is a prepayment penalty, whether you are paying points or receiving credits, and other key details. Compare the Annual Percentage Rate (APR) on the Closing Disclosure to the APR listed on your Loan Estimate.

If you live where a title or escrow company agent handles closing and there are two meetings, it's likely that the seller and the seller's agent or attorney will sign paperwork at one meeting and the buyer, accompanied by her agent or attorney, will sign at a separate meeting.

The Deed: public record of the ownership of the property It often includes a description of the property and signed by both parties. Deeds are the most important documents in your closing package because they contain the statement that the seller transfers all rights and stakes in the property to the buyer.

Keys, codes, and garage door openers to the house. Cashier's checks for closing costs and repair credits. Personal checkbook. Time, date, and location of the closing. Government-issued identification. Your writing hand (and maybe your lucky pen)