Basic Construction Contract

Understanding this form

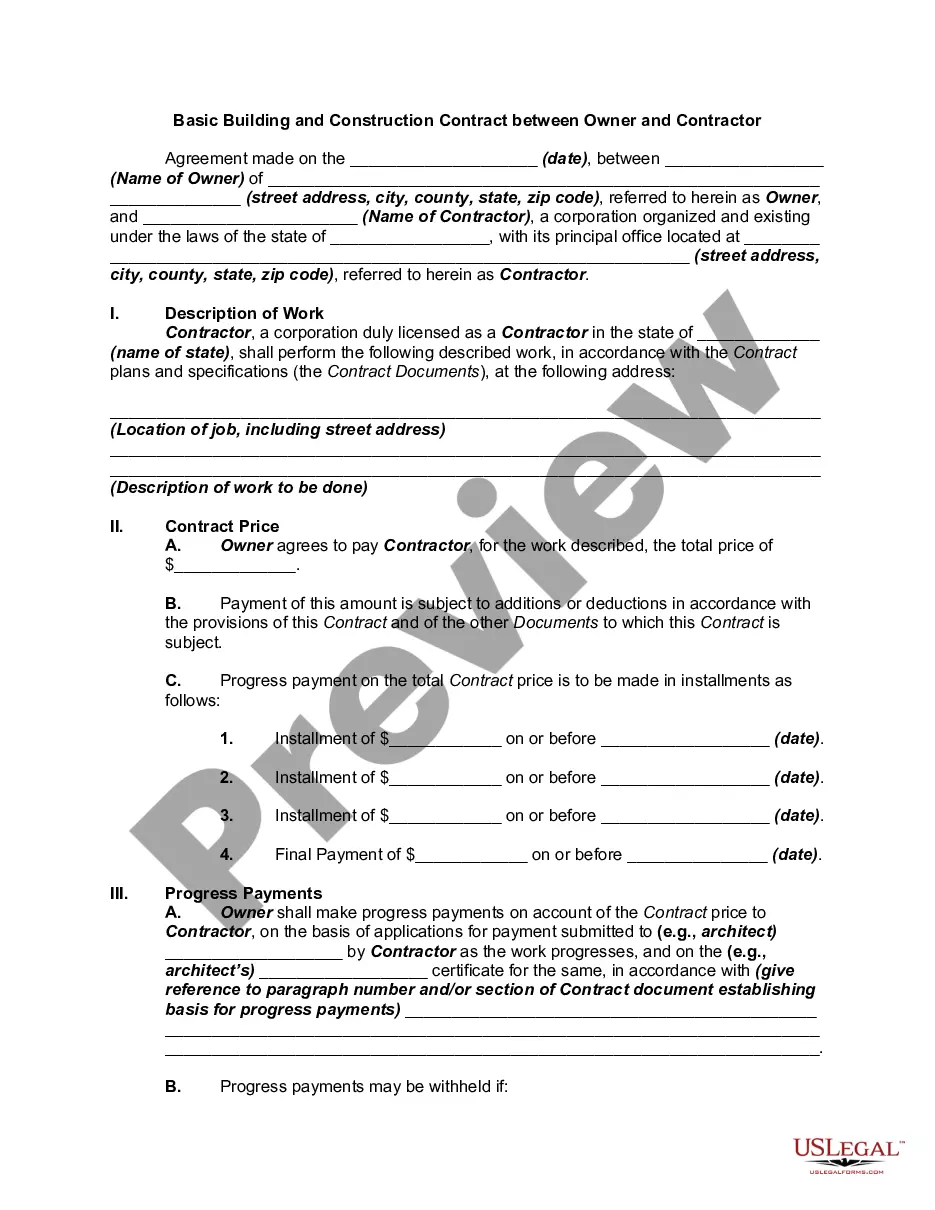

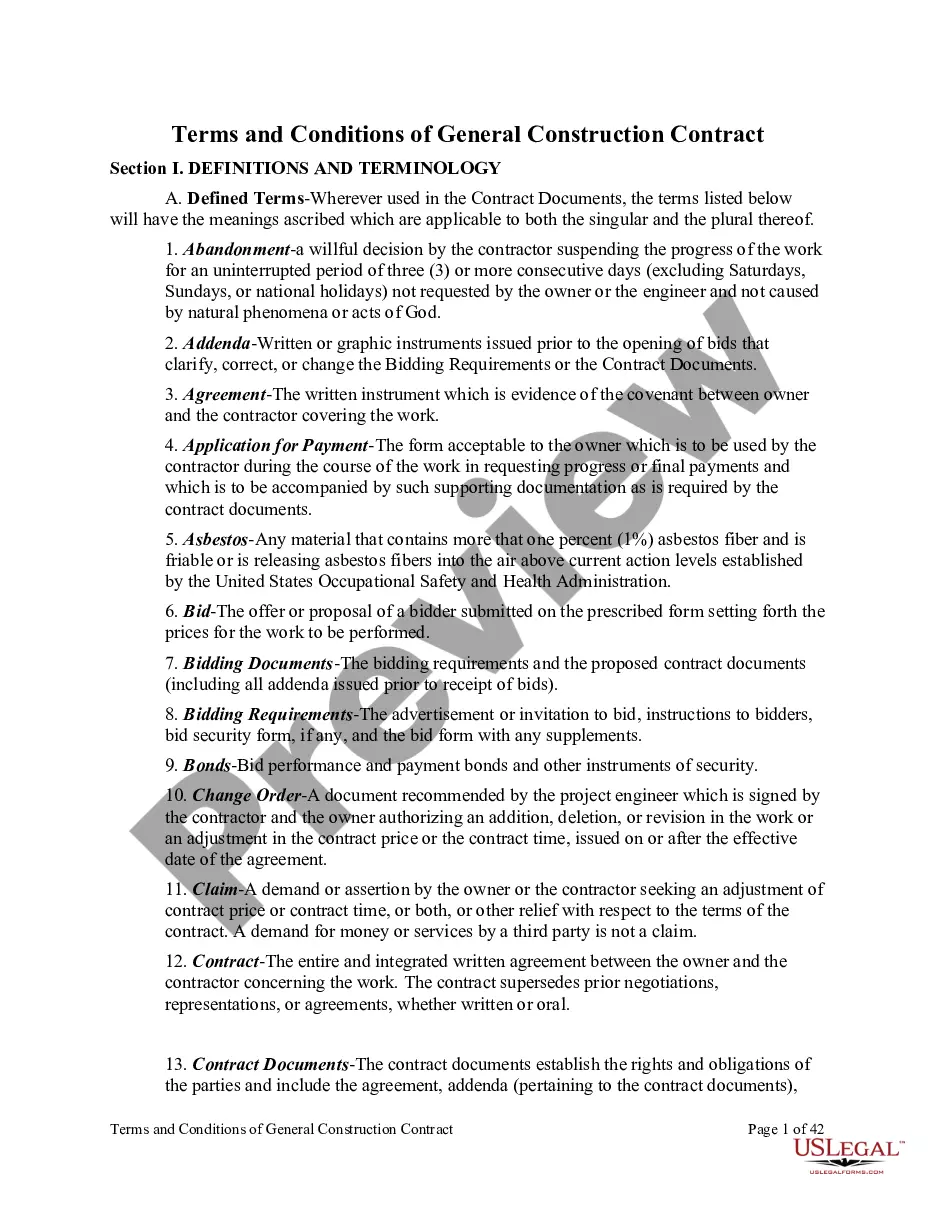

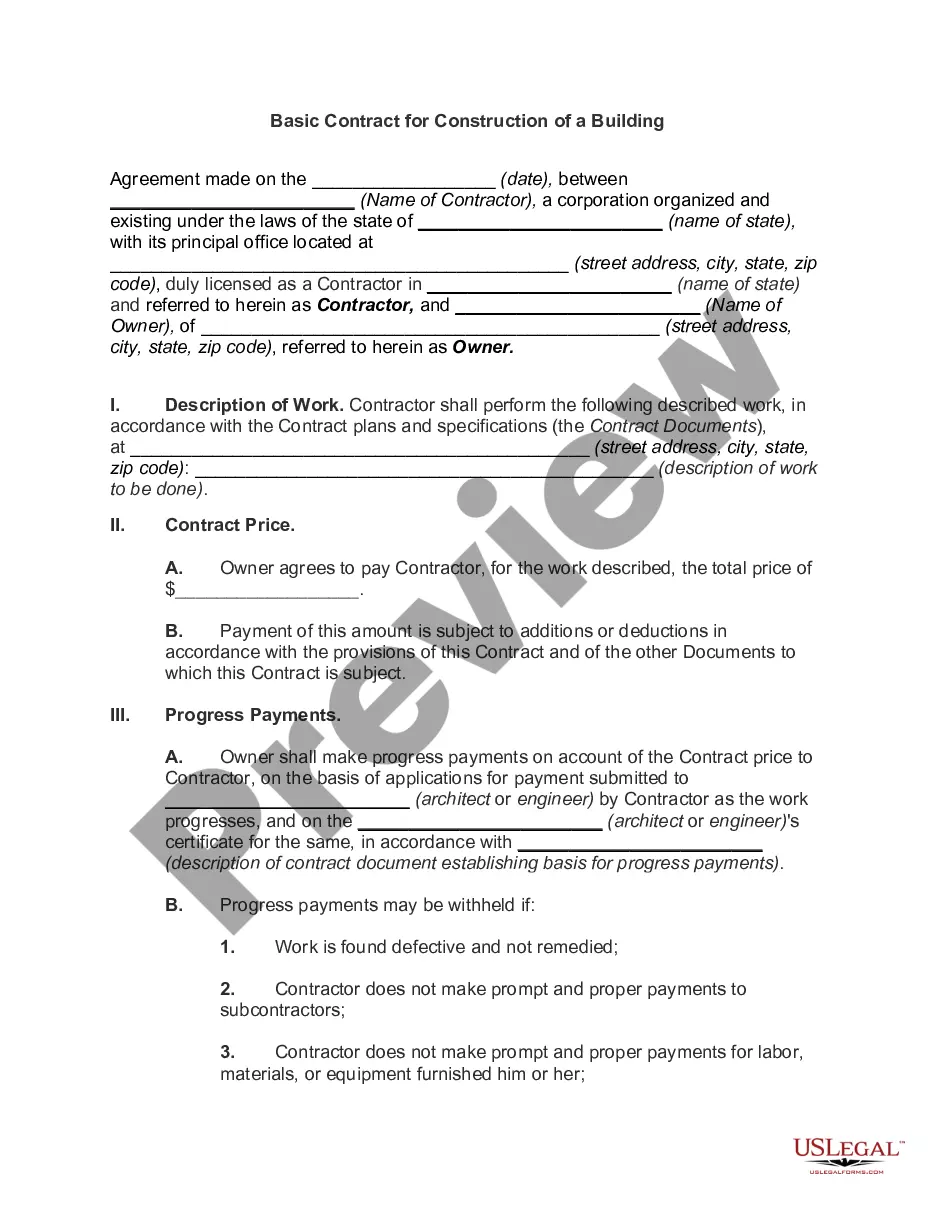

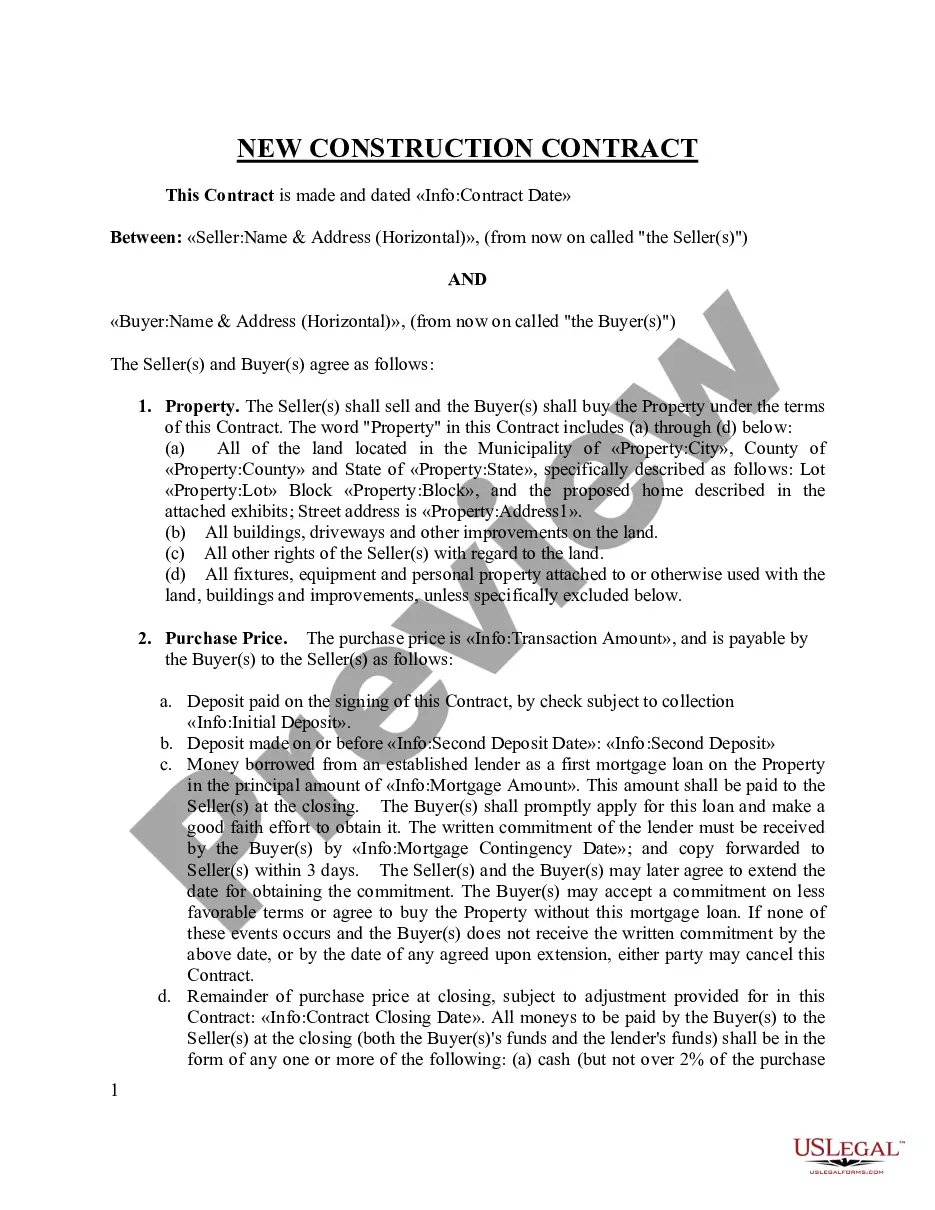

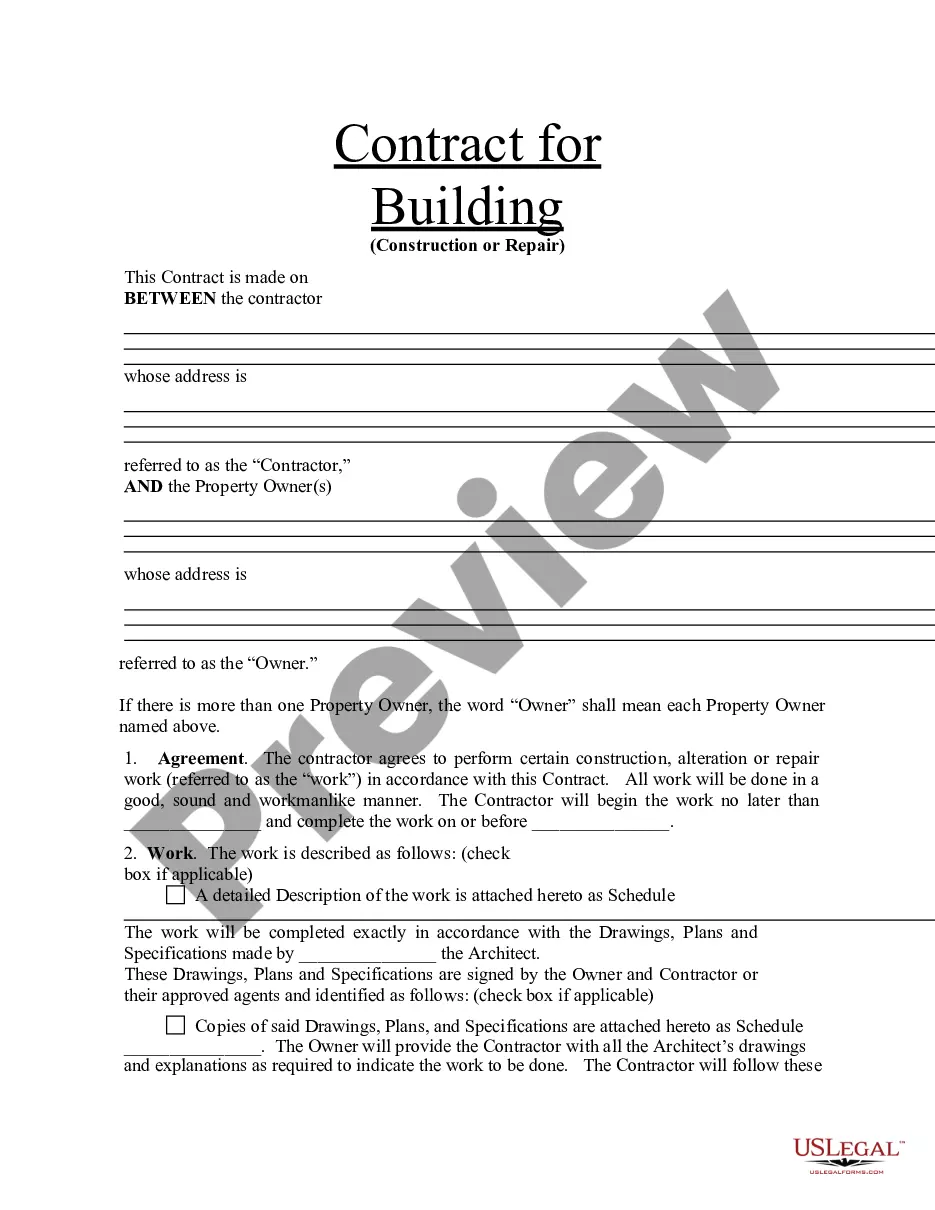

The Basic Construction Contract is a legally binding agreement between an owner and a contractor for the construction of specified work. This contract outlines the roles, responsibilities, and scope of work necessary for construction projects. It differs from other construction agreements by providing a general template that can be filled in based on the specific needs and details of the project and the parties involved.

Key components of this form

- Identification of the parties involved: Owner and Contractor.

- Scope of Work: Detailed description of the work to be completed.

- Contract Price: Amount to be paid for the completion of the work.

- Contract Time: Timeline for project completion, including the completion date.

- Change Orders: Process for handling changes to the scope, time, or price.

- Payment Procedures: Guidelines for progress payments and final payment.

- Insurance Requirements: Types of insurance that the contractor must maintain.

- Termination Clauses: Conditions under which the contract can be terminated by either party.

When to use this document

This form is used when entering into a construction project where clear terms, responsibilities, and expectations are necessary to avoid disputes. It is suitable for small to medium construction jobs, renovation projects, or any situation where formalizing the agreement between an owner and contractor is needed to ensure compliance and effective communication throughout the project.

Who can use this document

- Property owners looking to hire a contractor for construction work.

- Contractors who wish to formalize their agreement with a client.

- Individuals involved in residential or commercial construction projects.

- Those with little legal experience seeking a straightforward construction contract.

Completing this form step by step

- Identify the parties: Enter the names and addresses of the Owner and Contractor.

- Specify the property: Describe the location where the work will be performed.

- Detail the work: Clearly outline the scope of work as per Exhibit A.

- Enter the contract price: Specify the total amount to be paid for the contract completion.

- Set completion date: Provide the date by which the work is to be completed.

- Review and sign: Ensure both parties review the document, make necessary adjustments, and sign it.

Does this document require notarization?

This form usually doesn’t need to be notarized. However, local laws or specific transactions may require it. Our online notarization service, powered by Notarize, lets you complete it remotely through a secure video session, available 24/7.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Common mistakes to avoid

- Failing to clearly define the scope of work, leading to misunderstandings.

- Not including specific timelines or completion dates.

- Neglecting to outline payment procedures, which can cause cash flow issues.

- Overlooking the requirement for permits and licenses necessary for the project.

- Not obtaining signatures from both parties before starting work.

Why complete this form online

- Convenient access to legally vetted templates that save time.

- Editability allows for customization based on specific project needs.

- Reliability of documents drafted by licensed attorneys ensures legal validity.

Looking for another form?

Form popularity

FAQ

Revenue from fixed price construction contracts is recognised on the percentage of completion method, measured by reference to the percentage of labour hours incurred upto the reporting date to estimated total labour hours for each contract.

Step #1 Sort Paper Into Manageable Piles And Be Quick About It! Step #2 Simple Data Entry. Step #3 Payroll And Tax Reporting. Step #4 Reconcile Bank & Supplier Statements. Step #5 Complex Journal Entries. Step #6 Prepare Tax Reports. Step #7 Key Performance Indicators.

There are two generally accepted accounting methods used to account for construction contracts; the percentage of completion method (PC) and the completed contract method (CC).

Identifying/Contact Information. Title and Description of the Project. Projected Timeline and Completion Date. Cost Estimate and Payment Schedule. Stop Work Clause and Stop Payment Clause. Act of God Clause. Change Order Agreement. Warranty.

Accounting for a Project Under ConstructionConstruction Work-in-Progress is often reported as the last line within the balance sheet classification Property, Plant and Equipment. There is no depreciation of the accumulated costs until the project is completed and the asset is placed into service.

#1: Review Your Bid. #2: Review Complete Plans. #3: Review All Specifications. #4: Visit the Job Site. #5: Review the Job Schedule. #6: Complete a Project Checklist. #7: Verify Project Funding. #8: Read Complete Contract.

Name of contractor and contact information. Name of homeowner and contact information. Describe property in legal terms. List attachments to the contract. The cost. Failure of homeowner to obtain financing. Description of the work and the completion date. Right to stop the project.