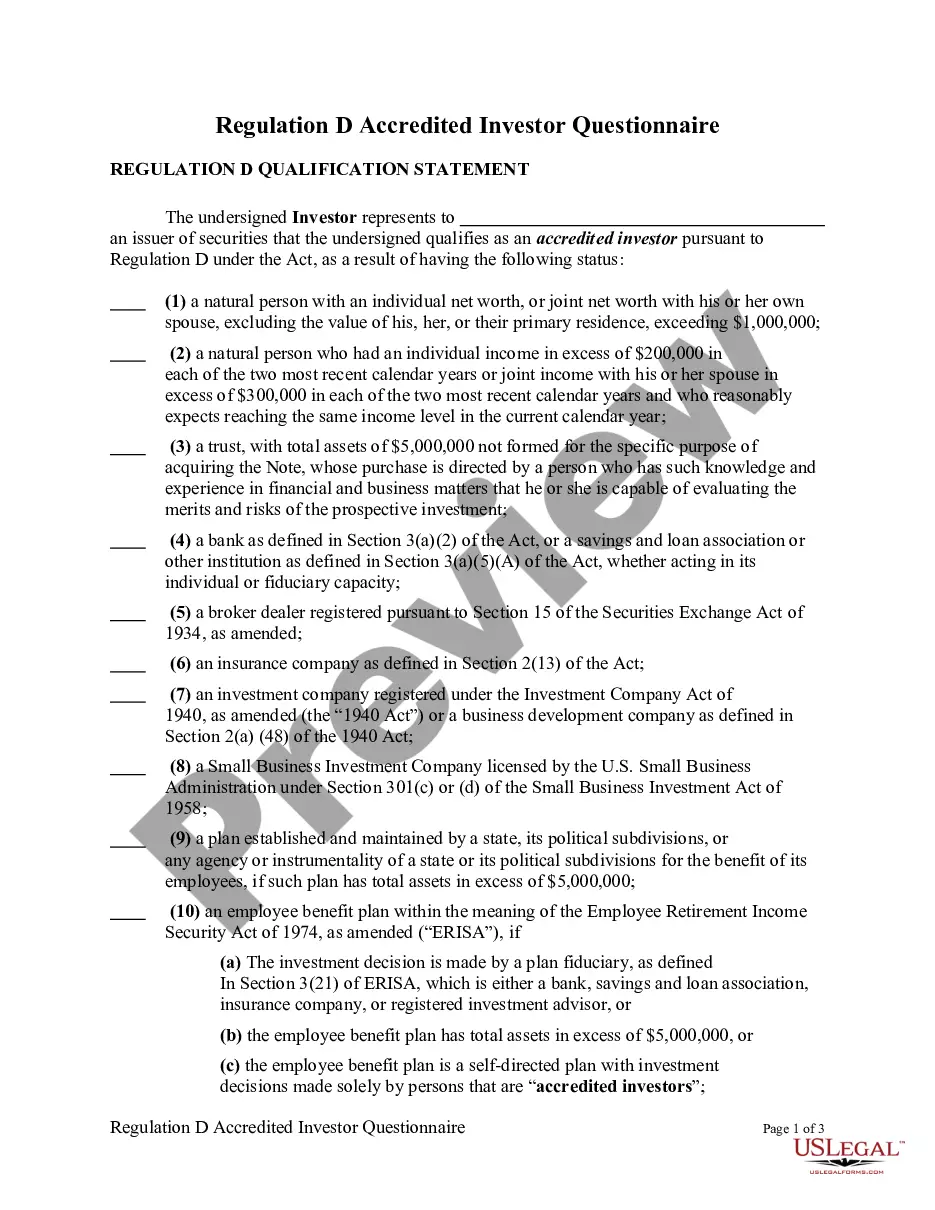

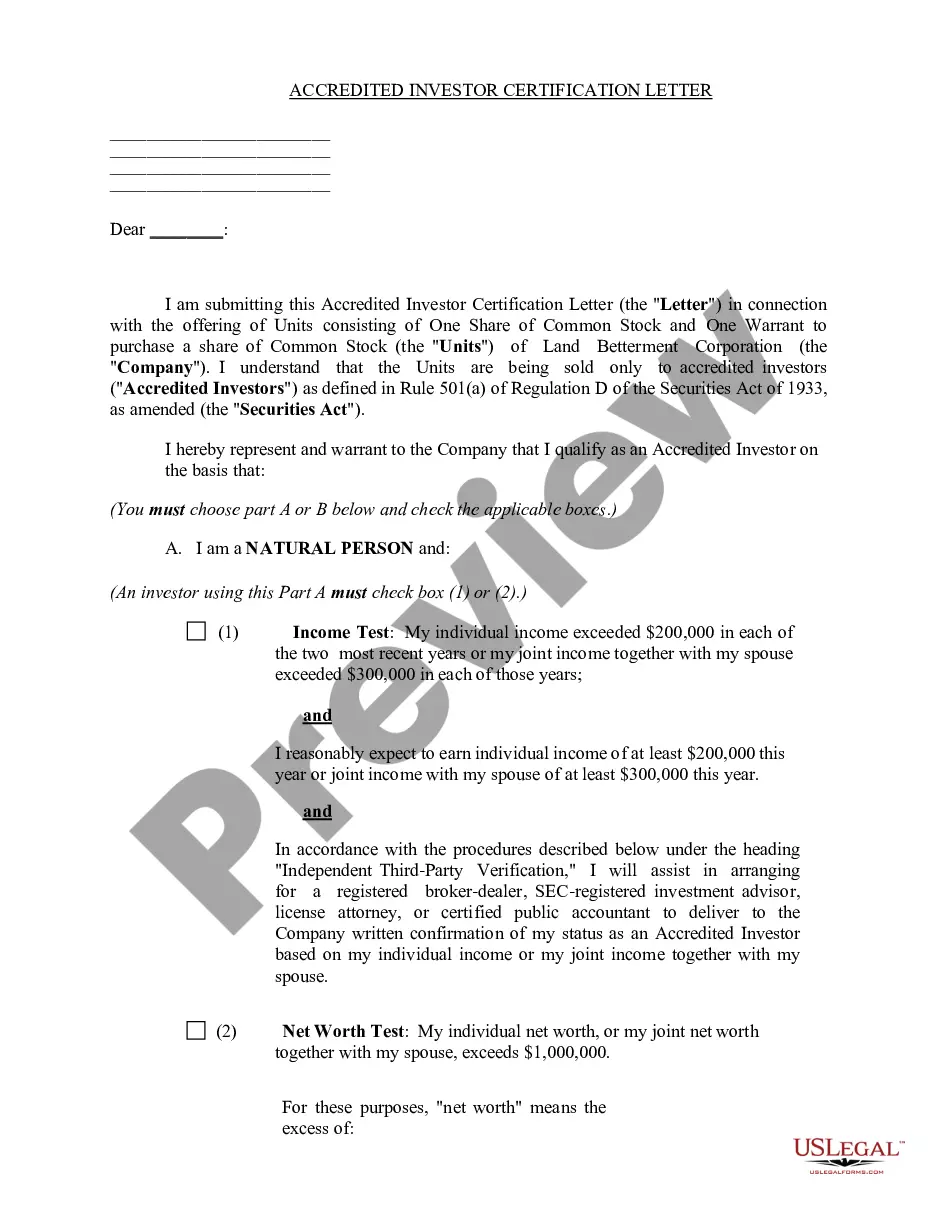

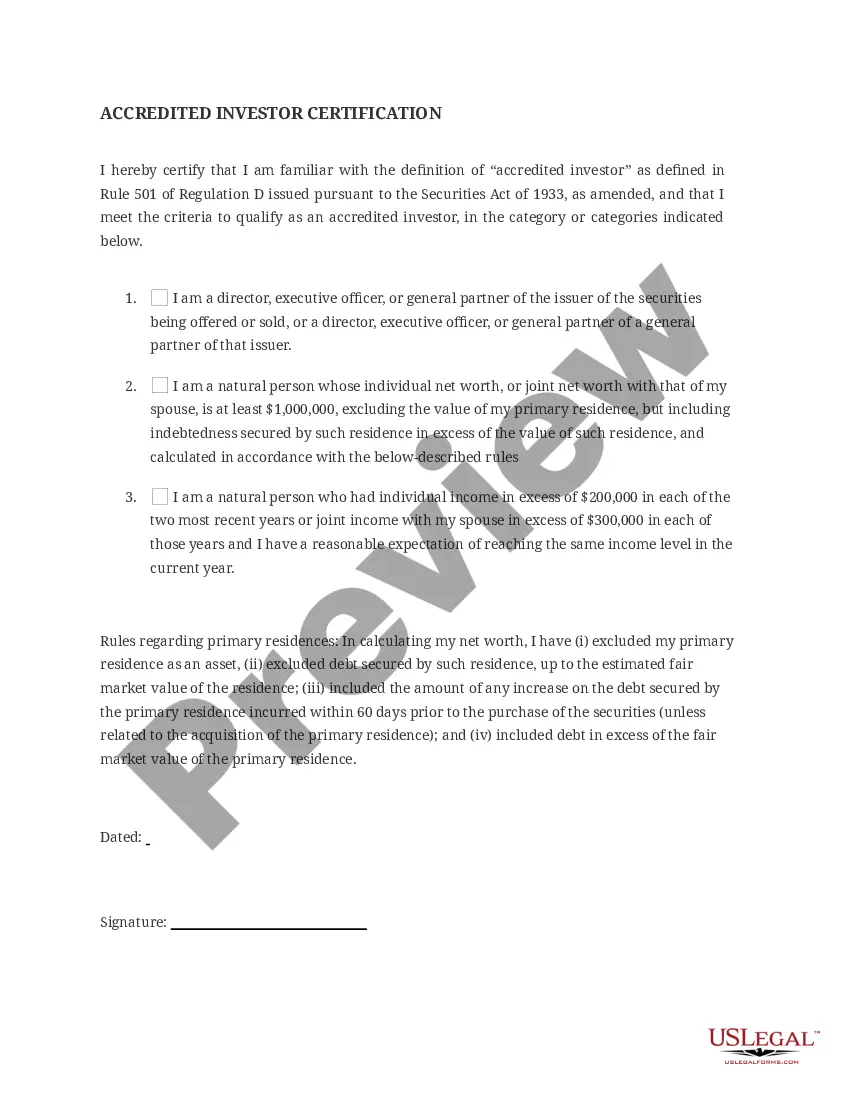

Under SEC law, a company that offers its own securities must register these investments with the SEC before it can sell them unless it meets an exception. One of those exceptions is selling unregistered investments to accredited investors.

To become an accredited investor the (SEC) requires certain wealth, income or knowledge requirements. The investor must fall into one of three categories. Firms selling unregistered securities must put investors through their own screening process to determine if investors can be considered an accredited investor.

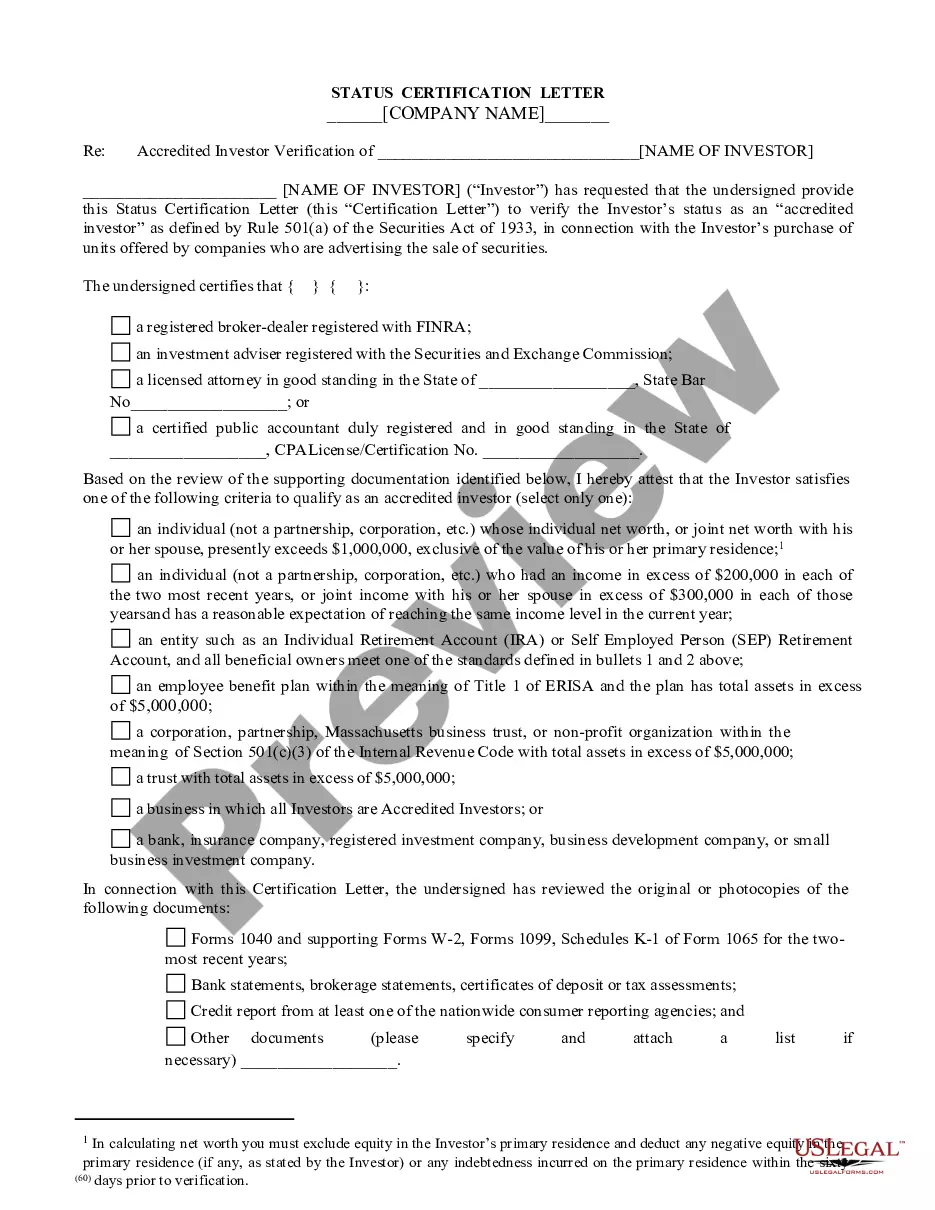

The Verifying Individual or Entity should take reasonable steps to verify and determined that an Investor is an "accredited investor" as such term is defined in Rule 501 of the Securities Act, and hereby provides written confirmation. This letter serves to help the Entity determine status.

Ohio Accredited Investor Self-Certification Attachment D

State:

Multi-State

Control #:

US-ENTREP-0015-1

Format:

Word;

Rich Text

Instant download

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Built-in online Word editor

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Export easily

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

E-sign your document

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

Notarize online 24/7

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

Store your document securely

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Accredited Investor Self-Certification Attachment D?

Discovering the right lawful document template could be a battle. Naturally, there are a variety of layouts available on the net, but how would you discover the lawful kind you need? Take advantage of the US Legal Forms internet site. The service gives thousands of layouts, for example the Ohio Accredited Investor Self-Certification Attachment D, that can be used for enterprise and personal demands. All of the types are checked by specialists and meet federal and state requirements.

In case you are presently authorized, log in for your profile and then click the Down load option to get the Ohio Accredited Investor Self-Certification Attachment D. Use your profile to check through the lawful types you may have bought earlier. Check out the My Forms tab of the profile and have another version from the document you need.

In case you are a whole new end user of US Legal Forms, listed below are easy instructions so that you can adhere to:

- First, make sure you have chosen the appropriate kind for your metropolis/state. You are able to examine the form utilizing the Preview option and study the form outline to make sure it will be the right one for you.

- If the kind will not meet your expectations, make use of the Seach industry to discover the correct kind.

- When you are certain that the form is acceptable, select the Get now option to get the kind.

- Choose the costs program you want and type in the essential details. Create your profile and pay money for your order using your PayPal profile or credit card.

- Opt for the submit structure and down load the lawful document template for your product.

- Comprehensive, modify and print out and indication the attained Ohio Accredited Investor Self-Certification Attachment D.

US Legal Forms will be the largest local library of lawful types for which you can discover numerous document layouts. Take advantage of the service to down load appropriately-manufactured files that adhere to condition requirements.

Form popularity

FAQ

PTE tax is a deduction on the entities' actual income, which then gets passed through to the partners/shareholders. Because the deduction is at the entity level instead of an itemized deduction, the shareholders' AGI is lowered, and then the itemized/standard deductions are considered.

Alternatively, a PTE may elect to file a composite return (OH DOT Form 4708) covering any or all of its owners (i.e., including both Ohio resident and nonresident owners) and paying tax for them at the highest marginal rate for nonbusiness income, which is currently 3.99%.

Ohio Income Tax Tables. For tax year 2022, Ohio's individual income tax brackets have been modified so that individuals with Ohio taxable nonbusiness income of $26,050 or less are not subject to income tax. Additionally, Ohio taxable nonbusiness income in excess of $115,300 is taxed at 3.99%.

Who Should file the IT 1140? A qualifying PTE is required to file an IT 1140 when it is subject to withholding or entity tax on distributive shares of income issued to qualifying investors.

You received an identity verification letter because an Ohio income tax return was filed OR an OH|TAX eServices account was created using your SSN. You should check with your spouse or tax preparer to ensure an Ohio return was not legitimately filed or an OH|TAX eServices account was not created on your behalf.

Only business income earned by a sole proprietorship or a pass-through entity generally qualifies for the deduction. A pass-through entity includes partnerships, S corporations and LLCs (limited liability companies).

Who Should File Form IT 4708? The IT 4708 is a composite income tax return a PTE elects to file on behalf of its qualifying investors. It is filed in lieu of the IT 1140 (the PTE withholding return). Unlike the IT 1140, a PTE can use the IT 4708 to claim credits or payments made on its behalf by other PTEs.

Every full-year resident, part year resident and full year nonresident must file an Ohio tax return if they have income from Ohio sources. An exception is for full year nonresidents living in a border state will not have to file an Ohio tax return if wages received are from an unrelated employer.