Ohio Annuity as Consideration for Transfer of Securities

Description

How to fill out Annuity As Consideration For Transfer Of Securities?

US Legal Forms - one of the most prominent collections of legal documents in the United States - provides a vast selection of legal templates you can obtain or print.

By utilizing the website, you can find thousands of documents for professional and personal use, organized by categories, states, or keywords. You can access the latest versions of forms like the Ohio Annuity as Consideration for Transfer of Securities within moments.

If you already have an account, Log In to obtain the Ohio Annuity as Consideration for Transfer of Securities from your US Legal Forms library. The Download button will appear on every form you view. You can access all previously acquired documents in the My documents section of your account.

Complete the purchase process. Use your credit card or PayPal account to finalize the transaction.

Choose the format and download the form onto your device. Edit it. Fill out, modify, and print and sign the downloaded Ohio Annuity as Consideration for Transfer of Securities. Each document you added to your account has no expiration date and is yours permanently. Therefore, if you wish to obtain or print another copy, simply go to the My documents section and click on the form you need. Access the Ohio Annuity as Consideration for Transfer of Securities with US Legal Forms, the most extensive collection of legal document templates. Utilize thousands of professional and state-specific templates that cater to your business or personal requirements.

- Make sure you select the correct form for your city/region.

- Click on the Preview button to review the content of the form.

- Read the form description to confirm that you have chosen the right document.

- If the form does not meet your needs, use the Search bar at the top of the screen to locate the one that does.

- Once you are satisfied with the form, confirm your selection by clicking the Purchase now button.

- Then, select the payment plan you prefer and provide your information to create an account.

Form popularity

FAQ

The new owner of the annuity can start receiving payments, change beneficiaries, and cash out the policy whenever they want. To give the annuity away, you simply contact the insurance company and state that you want to gift the ownership of the annuity policy to someone else or a trust.

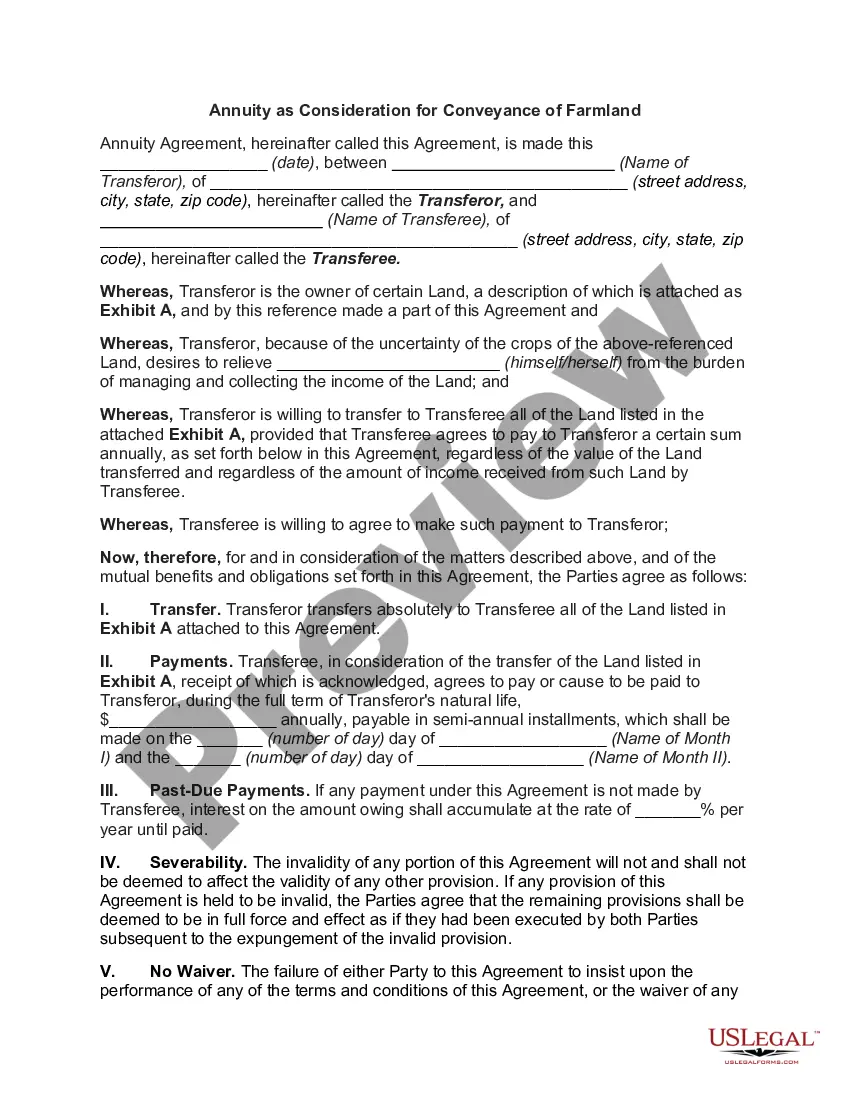

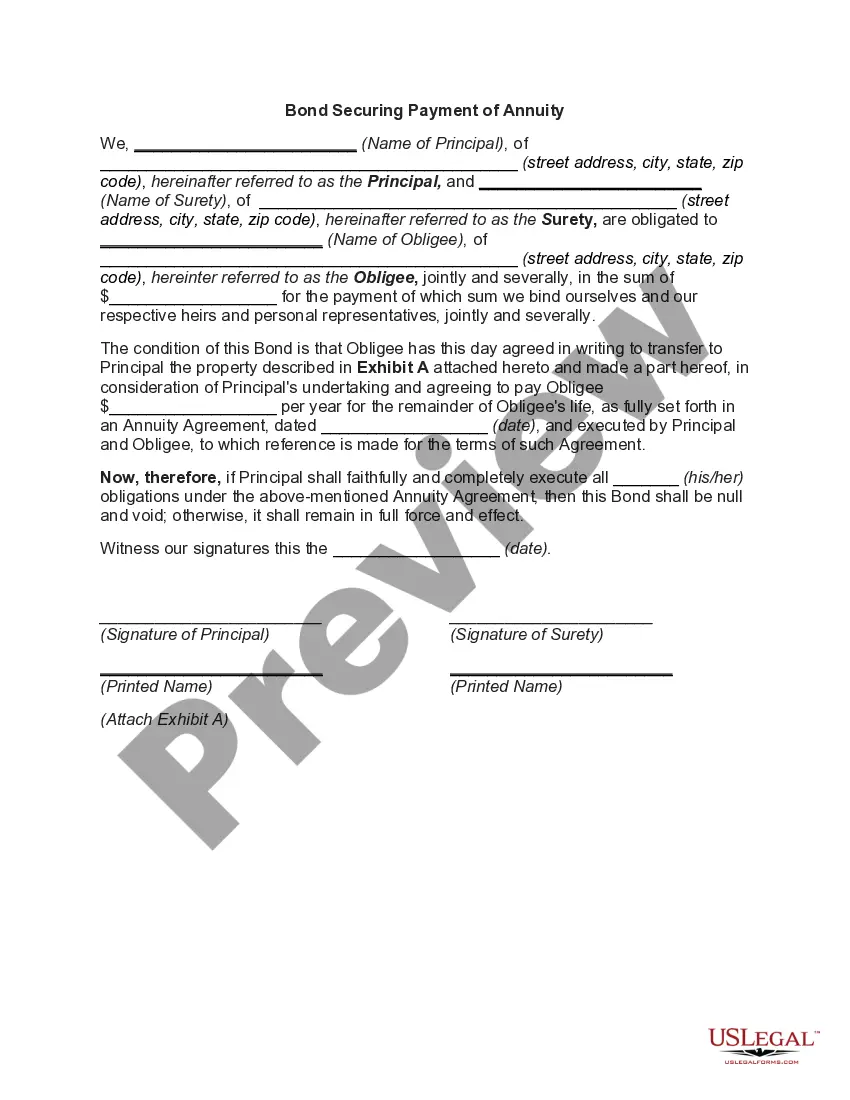

Annuity is a contract in between the insurance company (i.e., the party granting the annuity) and the annuitant (receiver of annuity) whereby in consideration of the payment of a purchase price by the annuitant, the other party (i.e., the insurance company) undertakes to make a yearly or annual payment to the annuitant

The most clear-cut way to withdraw money from an annuity without penalty is to wait until the surrender period expires. If your contract includes a free withdrawal provision, take only what's allowed each year, usually 10 percent.

Suitability Information Gathered by an InsurerAge.Annual income.Financial situation and needs, including the financial resources you're using to fund the annuity.Financial experience.Financial goals and objectives.Intended use of the annuity.Financial time horizon.More items...

From one retirement account IRA to another retirement account IRA. It's a non-taxable event. Even though any money coming out of an IRA will be taxed at ordinary income levels, transferring an annuity from one IRA to another will NOT trigger any taxes at all because no money is being taken out of the policy.

An annuity consideration or premium is the money an individual pays to an insurance company to fund an annuity or receive a stream of annuity payments. An annuity consideration may be made as a lump sum or as a series of payments, often referred to as contributions.

The new owner of the annuity can start receiving payments, change beneficiaries, and cash out the policy whenever they want. To give the annuity away, you simply contact the insurance company and state that you want to gift the ownership of the annuity policy to someone else or a trust.

As long as you do not withdraw your investment gains and keep them in the annuity, they are not taxed. A variable annuity is linked to market performance. If you do not withdraw your earnings from the investments in the annuity, they are tax-deferred until you withdraw them.

Variable annuities are securities regulated by the SEC. An indexed annuity may or may not be a security; however, most indexed annuities are not registered with the SEC. Fixed annuities are not securities and are not regulated by the SEC.

If you own an annuity inside of a Traditional IRA, the transfer is from one retirement account IRA to another retirement account IRA. It is a non-taxable event.