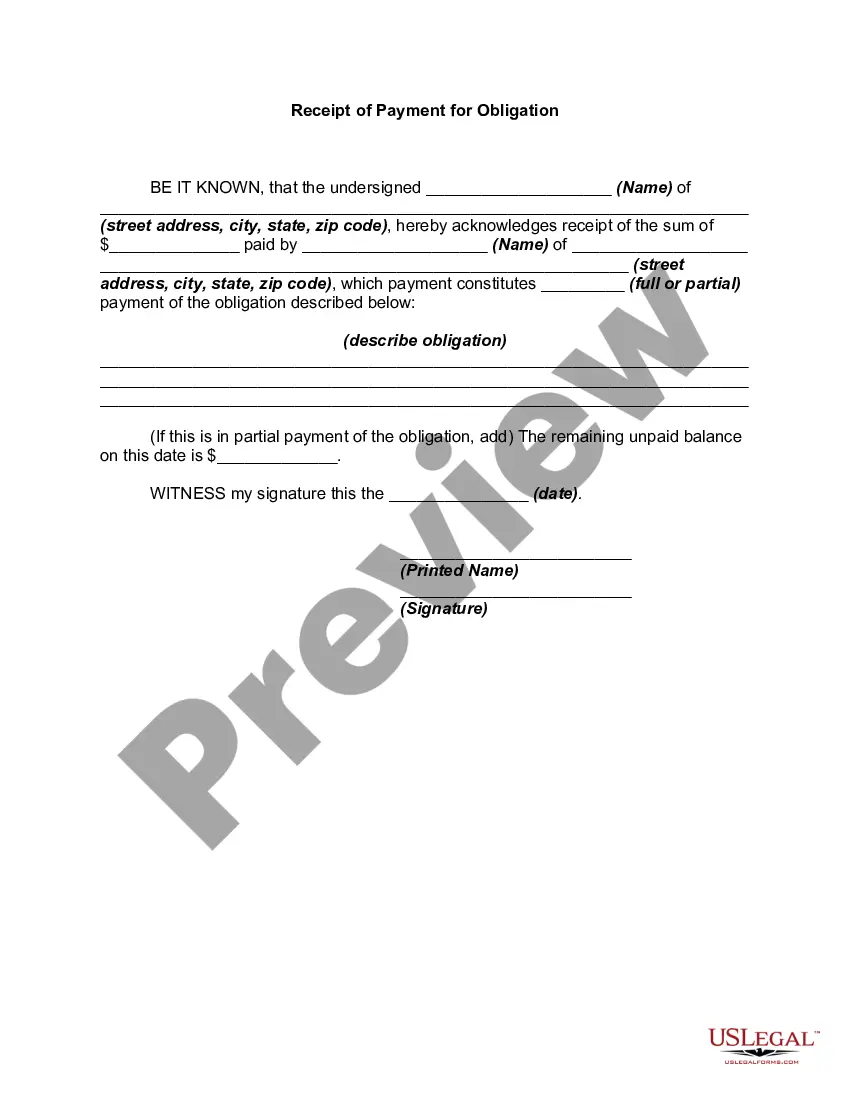

Ohio Receipt for loan Funds

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Receipt For Loan Funds?

You can invest hrs on the web attempting to find the lawful document web template which fits the federal and state demands you require. US Legal Forms provides 1000s of lawful forms which can be examined by professionals. You can actually download or print out the Ohio Receipt for loan Funds from our support.

If you currently have a US Legal Forms profile, you may log in and then click the Obtain button. Following that, you may comprehensive, change, print out, or indicator the Ohio Receipt for loan Funds. Every single lawful document web template you get is the one you have permanently. To obtain an additional backup of any obtained type, visit the My Forms tab and then click the corresponding button.

If you are using the US Legal Forms site the first time, stick to the basic guidelines beneath:

- First, be sure that you have chosen the proper document web template for your county/metropolis of your liking. See the type description to make sure you have picked the correct type. If readily available, utilize the Review button to search from the document web template as well.

- In order to get an additional model of your type, utilize the Search discipline to discover the web template that fits your needs and demands.

- After you have discovered the web template you would like, click on Buy now to move forward.

- Pick the rates prepare you would like, type your qualifications, and register for a free account on US Legal Forms.

- Complete the deal. You can utilize your Visa or Mastercard or PayPal profile to purchase the lawful type.

- Pick the format of your document and download it for your device.

- Make changes for your document if possible. You can comprehensive, change and indicator and print out Ohio Receipt for loan Funds.

Obtain and print out 1000s of document themes making use of the US Legal Forms web site, that offers the biggest collection of lawful forms. Use expert and status-distinct themes to tackle your company or personal demands.

Form popularity

FAQ

As used in sections 1322.01 to 1322.12 of the Revised Code: (A) "Buyer" means an individual who is solicited to purchase or who purchases the services of a mortgage broker for purposes of obtaining a residential mortgage loan.

The Residential Mortgage Lending Act states that the bond needs to be 0.5% of the aggregate loan amount of residential mortgage loans originated in the preceding calendar year. The bond needs to be at least $50,000 and cannot exceed $150,000.

Rule 13-3-03 | Definitions. (B) "Net worth," as used in division (B)(1) of section 1321.53 of the Revised Code shall mean the amount by which the business assets exceed the business liabilities.

(A) No supplier shall commit an unfair or deceptive act or practice in connection with a consumer transaction. Such an unfair or deceptive act or practice by a supplier violates this section whether it occurs before, during, or after the transaction.

Homebuyer's Protection Act (Predatory Lending Law) (2007) Protects consumers from abusive lending practices committed on or after January 1, 2007 by non-bank lenders, loan officers and mortgage brokers.

The Act prohibits these businesses from committing unfair, deceptive or unconscionable acts in connection with a residential mortgage loan, including: Entering into a mortgage knowing you had no reasonable probability of payment of the mortgage.

The cornerstone of Ohio consumer law is the Consumer Sales Practices Act (CSPA), which protects individual consumers from unfair, deceptive, and unconscionable sales practices in connection with consumer transactions.

The Truth in Lending Act (TILA) protects you against inaccurate and unfair credit billing and credit card practices. It requires lenders to provide you with loan cost information so that you can comparison shop for certain types of loans.