New York Notice of Adverse Action - Non-Employment - Due to Credit Report

Description

How to fill out Notice Of Adverse Action - Non-Employment - Due To Credit Report?

US Legal Forms - one of the most extensive collections of legal documents in the United States - offers a range of legal document templates you can download or print.

By using the website, you can access thousands of forms for business and personal purposes, categorized by type, state, or keywords. You can find the latest versions of forms such as the New York Notice of Adverse Action - Non-Employment - Due to Credit Report in moments.

If you already have a membership, Log In and download the New York Notice of Adverse Action - Non-Employment - Due to Credit Report from the US Legal Forms library. The Download button will be visible on every document you view. You can access all previously downloaded forms in the My documents section of your account.

Process the transaction. Use your credit card or PayPal account to complete the purchase.

Select the format and download the document onto your device. Make edits. Fill out, modify, print, and sign the downloaded New York Notice of Adverse Action - Non-Employment - Due to Credit Report. Every template you added to your account does not have an expiry date and is yours forever. So, if you wish to download or print another copy, simply visit the My documents section and click on the document you desire. Access the New York Notice of Adverse Action - Non-Employment - Due to Credit Report through US Legal Forms, the most comprehensive collection of legal document templates. Utilize thousands of professional and state-specific templates that fulfill your business or personal needs and requirements.

- Ensure you have selected the correct document for your region/area.

- Click on the Review button to examine the document's content.

- Read the document description to confirm that you have selected the right document.

- If the document does not meet your requirements, use the Search box at the top of the screen to find one that does.

- If you are satisfied with the document, confirm your choice by clicking the Get now button.

- Then, select your preferred pricing option and provide your details to register for an account.

Form popularity

FAQ

Most job seekers don't' even know this, and it raises a really important question is: can you be denied a job because of bad credit? The short answer is yes, you can. Also, keep in mind that bad credit is different than no credit but in this case, bad credit can be the culprit.

Continue with the hire or take adverse action Taking adverse action is regrettable for both the organization and the candidate, but eventually you'll need to decide to rescind your job offer or proceed with hiring.

In particular: if you deny a consumer credit based on information in a consumer report, you must provide an adverse action notice to the consumer. if you grant credit, but on less favorable terms based on information in a consumer report, you must provide a risk-based pricing notice.

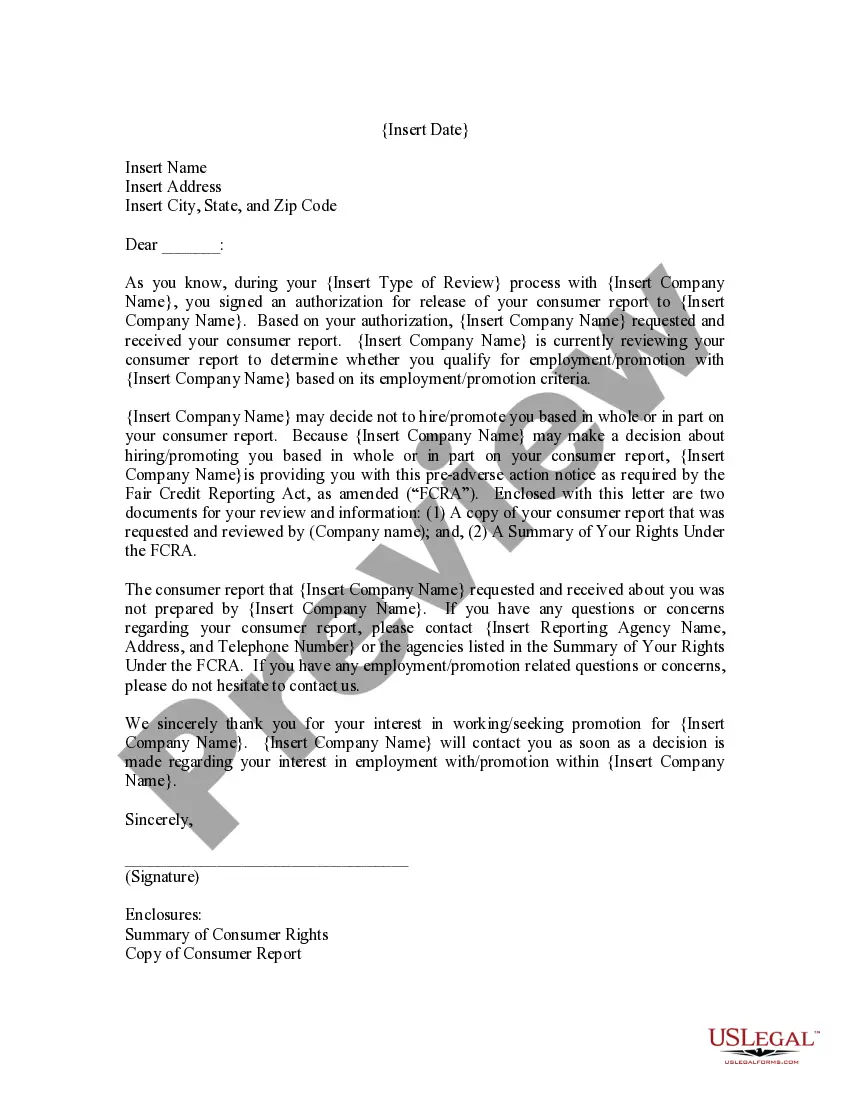

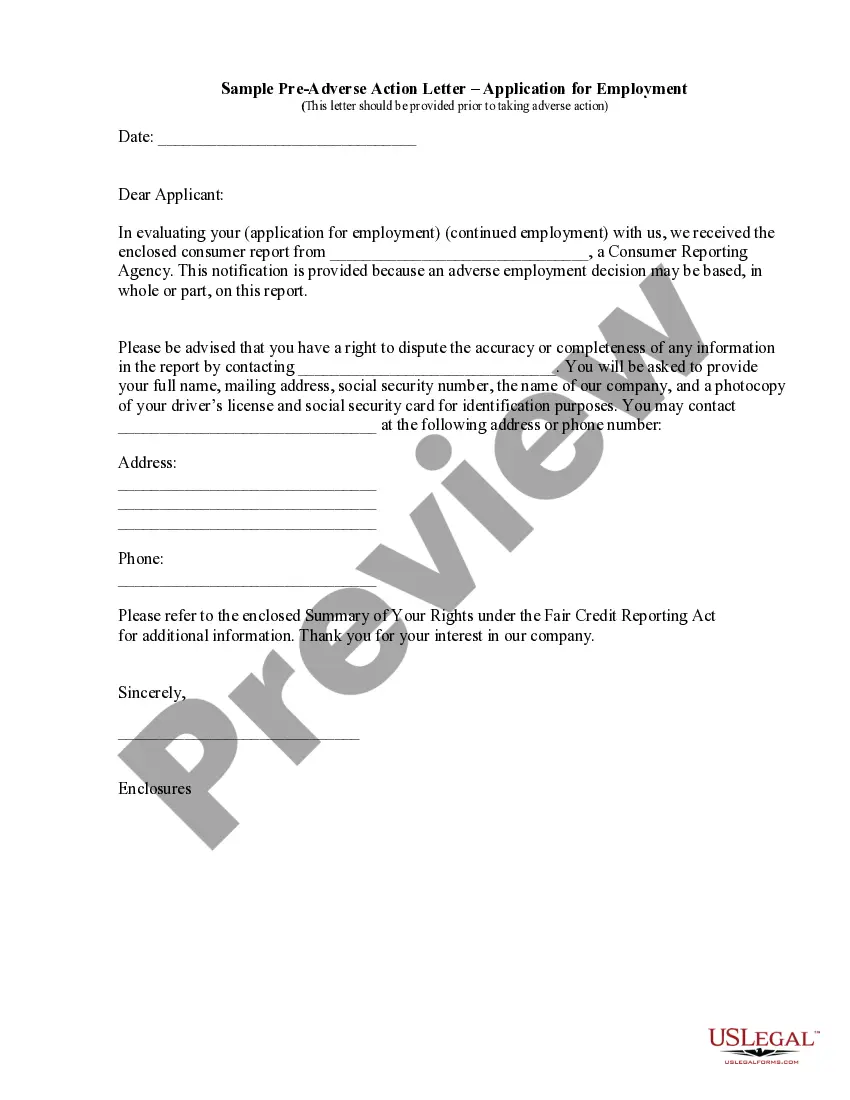

If you plan to take adverse action based on consumer report finding, you must send the tenant or employee a Pre-Adverse Action notice within 3 days of receiving the consumer report. Though this notice is typically mailed, it may also be communicated verbally or by e-mail.

Some states and major cities have enacted legislation that protects applicants from having their credit histories used against them in hiring and other employment practices. However, the majority of states still allow private employers to use poor credit history as a lawful reason to reject a job seeker's application.

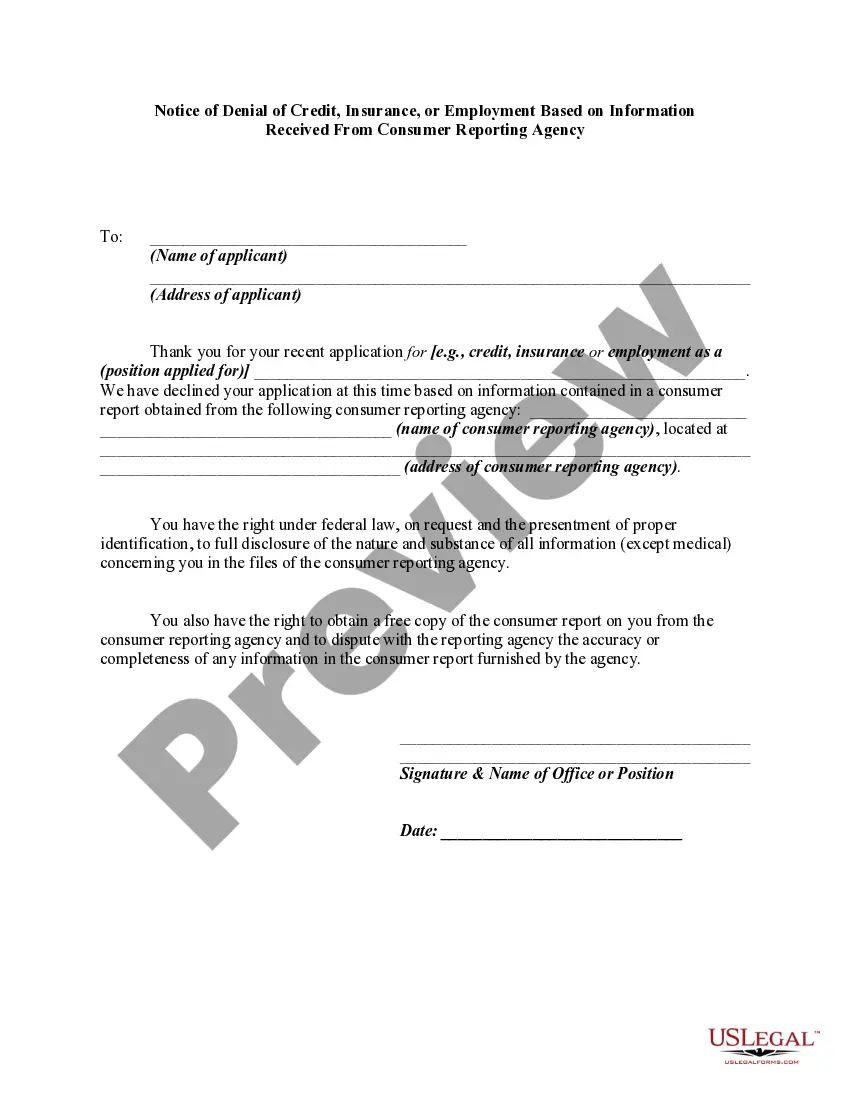

An adverse action notice is to inform you that you have been denied credit, employment, insurance, or other benefits based on information in a credit report. The notice should indicate which credit reporting agency was used, and how to contact them.

The pre-adverse action letter minimizes the possibility of an applicant being denied employment without ever knowing he or she was the victim of inaccurate or incomplete data. In Step 2, here's how long you should give the applicant to dispute the information found in their background check.

Your credit cannot be the reason you are fired, not hired, or not promoted. Under the NYC Human Rights Law, employers are prohibited from considering credit when making employment decisions about current or potential employees.

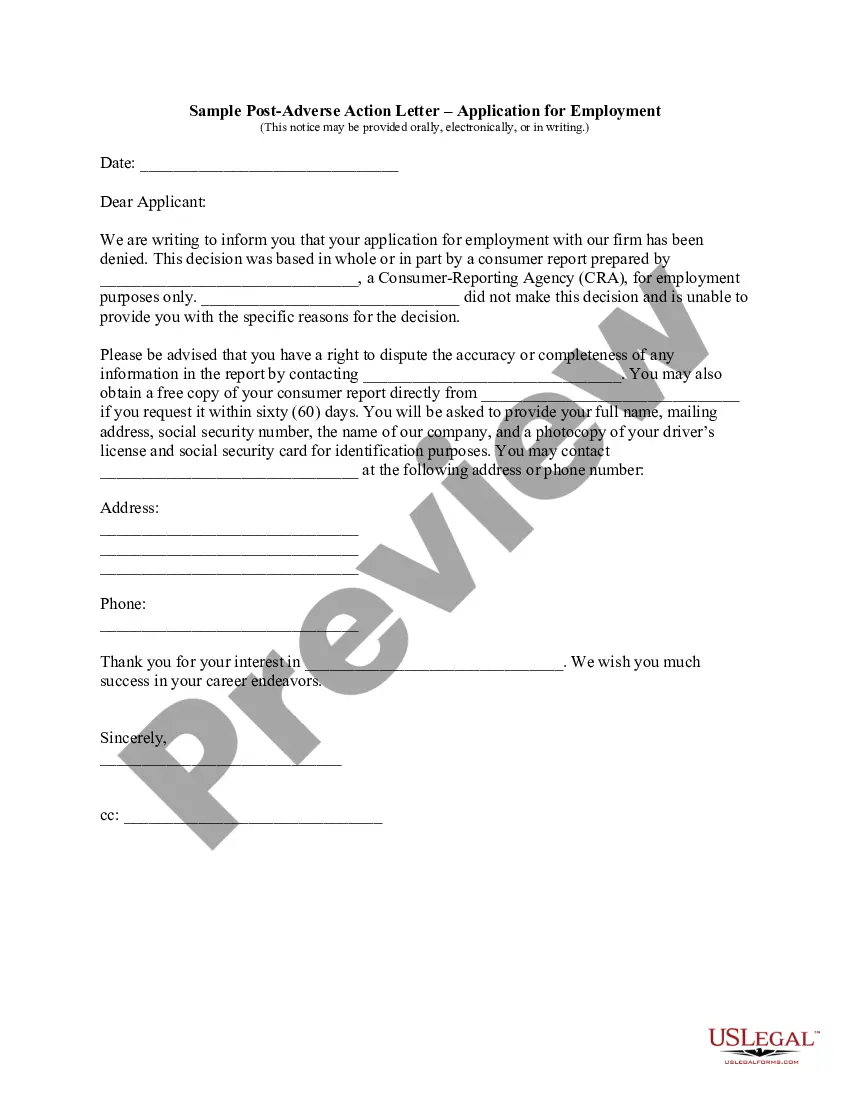

While there is no time period specifically referenced in the Fair Credit Reporting Act (FCRA), the Fair Trade Commission (FTC) has provided guidance that suggests five (5) business days is the minimum time period that should elapse after sending a Pre-Adverse Action Notice before sending the Final Adverse Action

A creditor must notify the applicant of adverse action within: 30 days after receiving a complete credit application. 30 days after receiving an incomplete credit application. 30 days after taking action on an existing credit account.