New York Breakdown of Savings for Budget and Emergency Fund

Description

How to fill out Breakdown Of Savings For Budget And Emergency Fund?

It is feasible to invest hours online trying to locate the legal document template that meets the state and federal requirements you require.

US Legal Forms offers an extensive collection of legal forms that have been reviewed by experts.

You can easily obtain or print the New York Breakdown of Savings for Budget and Emergency Fund from our services.

If available, use the Review button to look through the document template as well.

- If you already possess a US Legal Forms account, you may Log In and then click the Download button.

- After that, you can complete, modify, print, or sign the New York Breakdown of Savings for Budget and Emergency Fund.

- Each legal document template you acquire is yours indefinitely.

- To obtain another copy of any purchased form, go to the My documents tab and click the corresponding button.

- If you are visiting the US Legal Forms website for the first time, follow the simple instructions below.

- First, verify that you have selected the correct document template for the region/area you choose.

- Review the form details to ensure that you have selected the appropriate form.

Form popularity

FAQ

The 3-6-9 rule suggests saving three months' worth of expenses for minor emergencies, six months for major ones, and nine months as a maximum cushion. This strategy fits neatly into the New York Breakdown of Savings for Budget and Emergency Fund approach, providing flexibility according to your financial situation. Adopting this rule can enhance your financial security and peace of mind. You may find helpful templates on USLegalForms to track your savings according to this guideline.

It's all about your personal expenses Those include things like rent or mortgage payments, utilities, healthcare expenses, and food. If your monthly essentials come to $2,500 a month, and you're comfortable with a four-month emergency fund, then you should be set with a $10,000 savings account balance.

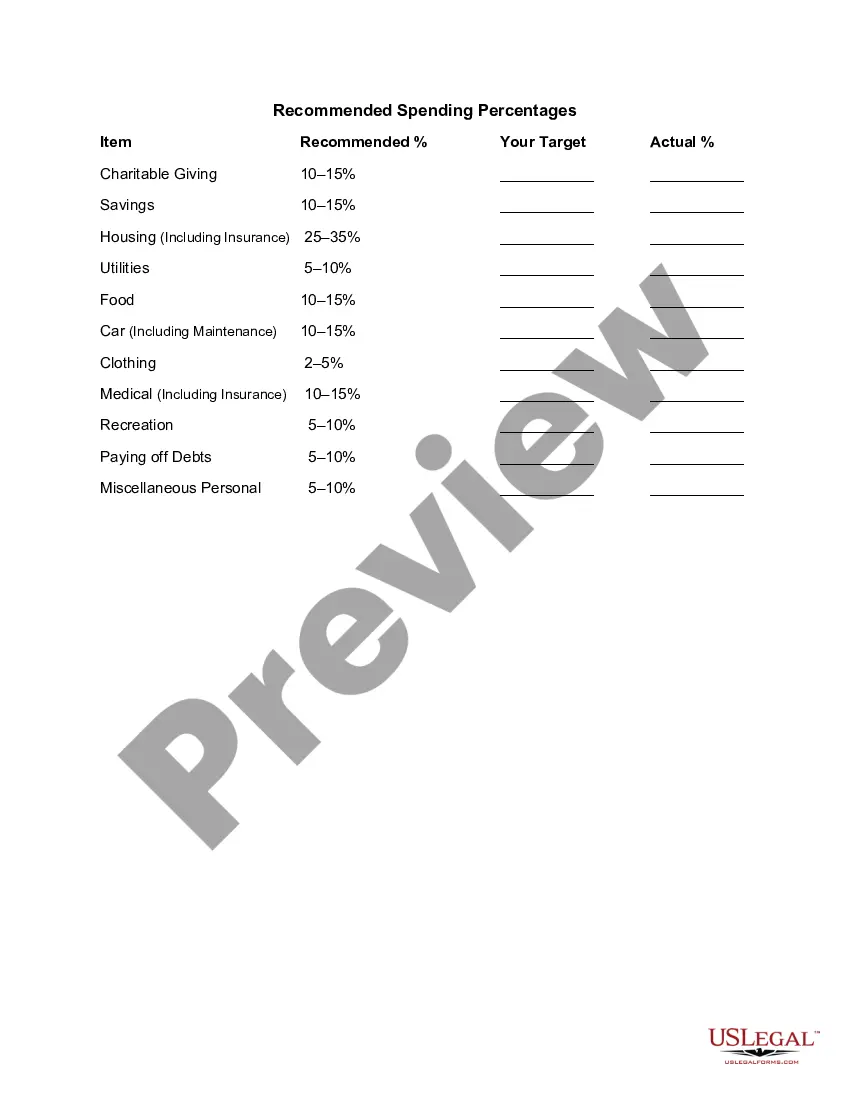

The rule states that you should spend up to 50% of your after-tax income on needs and obligations that you must-have or must-do. The remaining half should be split up between 20% savings and debt repayment and 30% to everything else that you might want.

Budget 101: debunking the 50-20-30 ruleWhat is the 50-20-30 rule? The 50-20-30 rule is a money management technique that divides your paycheck into three categories: 50% for the essentials, 20% for savings and 30% for everything else.The envelope system.The 80-20 plan.Create your own.

If you have consumer debt, I recommend saving a starter emergency fund of $1,000 first. Then, once you're out of debt, it's time to beef up that amount and save three to six months of expenses in a fully funded emergency fund.

While the size of your emergency fund will vary depending on your lifestyle, monthly costs, income, and dependents, the rule of thumb is to put away at least three to six months' worth of expenses.

It does work. That $1,000 emergency fund will be enough to have your back while you hustle to pay off your debt as quick as you can. The Baby Steps work, so stick with themno matter how uncomfortable it might make you feel. Lean into that awkward feeling and let that spur you on to pay off your debt even faster.

Dave Ramsey: $1,000; then three to six months of expenses If you follow Ramsey's Seven Baby Steps, which are designed to help people take control of their money through debt payoff and building wealth, the first step is to establish a starter emergency fund of $1,000.

Senator Elizabeth Warren popularized the so-called "50/20/30 budget rule" (sometimes labeled "50-30-20") in her book, All Your Worth: The Ultimate Lifetime Money Plan. The basic rule is to divide up after-tax income and allocate it to spend: 50% on needs, 30% on wants, and socking away 20% to savings.

The basic rule of thumb is to divide your monthly after-tax income into three spending categories: 50% for needs, 30% for wants and 20% for savings or paying off debt. By regularly keeping your expenses balanced across these main spending areas, you can put your money to work more efficiently.