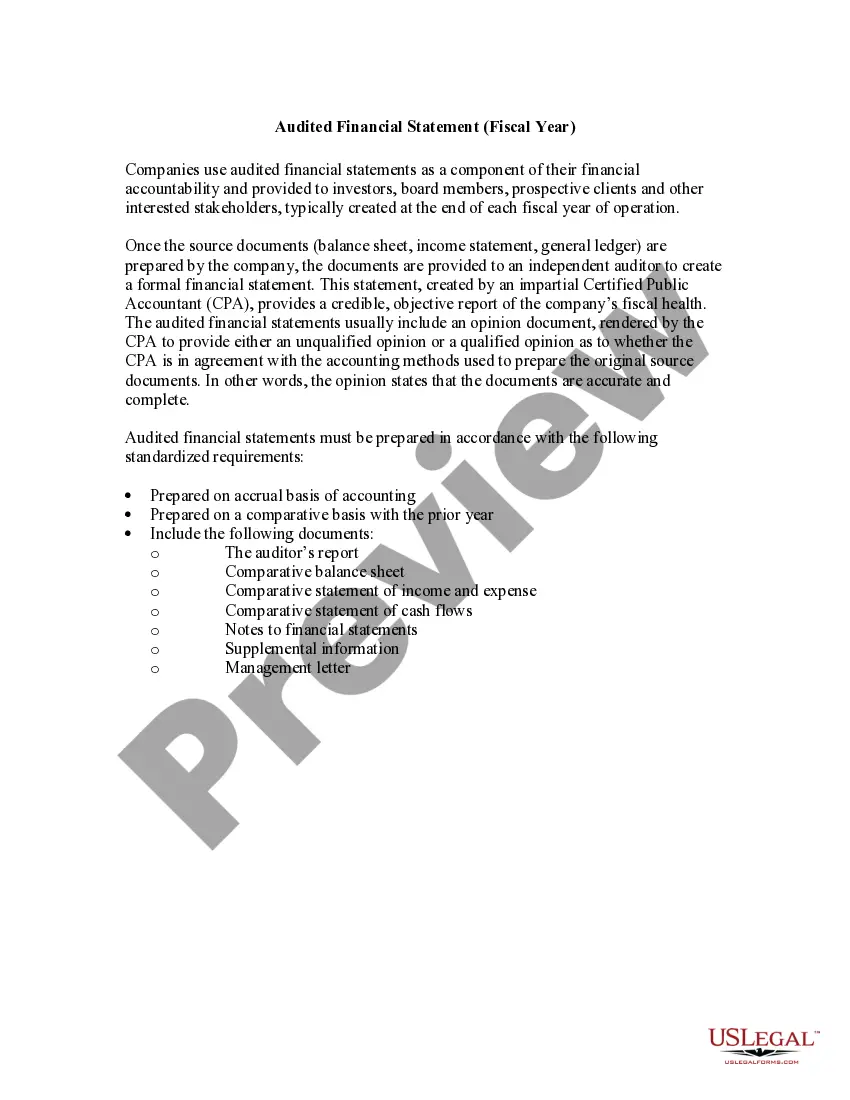

As most commonly used in legal settings, an audit is an examination of financial records and documents and other evidence by a trained accountant. Audits are conducted of records of a business or governmental entity, with the aim of ensuring proper accounting practices, recommendations for improvements, and a balancing of the books. An audit performed by employees is called "internal audit," and one done by an independent (outside) accountant is an "independent audit." Auditors may refuse to sign the audit to guarantee its accuracy if only limited records are produced.

New York Report of Independent Accountants after Audit of Financial Statements

Category:

State:

Multi-State

Control #:

US-01939BG

Format:

Word

Instant download

Description

How to fill out Report Of Independent Accountants After Audit Of Financial Statements?

Locating the appropriate legal document template can be challenging. Of course, there are numerous templates accessible online, but how can you acquire the specific legal type you require.

Utilize the US Legal Forms website. The platform offers a vast array of templates, including the New York Report of Independent Accountants after Audit of Financial Statements, suitable for both business and personal needs. All forms are reviewed by professionals and comply with both federal and state regulations.

If you are already registered, Log In to your account and click the Download button to obtain the New York Report of Independent Accountants after Audit of Financial Statements. Use your account to browse the legal forms you have previously acquired. Navigate to the My documents section of your account to get another copy of the document you need.

Complete, modify, and print the downloaded New York Report of Independent Accountants after Audit of Financial Statements. US Legal Forms is the largest collection of legal forms, where you can find various document templates. Take advantage of the service to download professionally crafted papers that meet state requirements.

- If you are a new user of US Legal Forms, here are some simple steps to follow.

- First, ensure you have selected the correct form for your locality/region. You may review the document using the Review button and read the form description to confirm it is the right fit for you.

- If the form does not meet your needs, utilize the Search box to find the appropriate form.

- Once you are certain the form is suitable, click the Buy now button to proceed with the purchase.

- Choose the pricing plan you prefer and fill in the required information. Create your account and complete the order using your PayPal account or credit card.

- Select the format and download the legal document template to your device.

Form popularity

FAQ

Indeed, financial accounting reports are commonly audited by certified public accountants (CPAs). These auditors follow rigorous standards to assess the validity of the financial data included in the reports. Upon completion of their analysis, they issue a Report of Independent Accountants after Audit of Financial Statements, which signifies that the reports have been independently reviewed and are trustworthy. Engaging a CPA for this process is vital for achieving accurate and credible financial disclosures.

Yes, financial accounting is often subjected to an audit, especially for companies that are publicly traded or have significant stakeholders. Through this audit process, independent auditors evaluate the accuracy and completeness of the financial records. They provide a Report of Independent Accountants after Audit of Financial Statements, which enhances the reliability of the accounting information presented. This ensures compliance with applicable laws and standards, promoting overall financial transparency.

An independent CPA becomes associated with financial statements when they are engaged to perform an audit. During this process, the CPA examines the financial documents, transactions, and internal controls of the company. After completing the audit, they issue a Report of Independent Accountants after Audit of Financial Statements, which formally presents their findings. This association signifies a third-party validation of the financial data, adding value to the company's reporting.

A company often opts for an independent audit to demonstrate transparency to shareholders, investors, and regulatory bodies. An independent auditor provides an objective assessment of the financial statements, resulting in a Report of Independent Accountants after Audit of Financial Statements. This report can enhance investor confidence and reduce risks associated with financial misstatements. Ultimately, it supports better decision-making and fosters trust in the organization's financial integrity.

The management of a company holds the primary responsibility for preparing its financial statements. Once the statements are prepared, it is the role of the independent auditor to evaluate their accuracy and provide a Report of Independent Accountants after Audit of Financial Statements. This independent evaluation helps ensure that the financial reports convey an honest picture of the company's financial health. Stakeholders can trust the reports knowing they have undergone thorough scrutiny.

Financial reports are typically audited by independent certified public accountants (CPAs). These professionals review and analyze the financial statements to ensure accuracy and compliance with accounting standards. In New York, a Report of Independent Accountants after Audit of Financial Statements is often required to provide assurance to stakeholders. Relying on experienced CPAs enhances the credibility of your financial reporting.

Auditing generally refers to the examination of financial records, which can be conducted internally or externally. Independent auditing strictly involves a third-party auditor assessing a company's financial statements without any conflicts of interest. This level of impartiality is key for stakeholders seeking a reliable New York Report of Independent Accountants after Audit of Financial Statements, promoting greater confidence in financial disclosures.

An independent audit report focuses on providing an unbiased assessment of financial statements, while a statutory audit report is conducted to comply with legal requirements. Both aim to ensure accuracy and transparency in financial reporting, but the statutory audit report is mandatory for certain entities. Many companies refer to the New York Report of Independent Accountants after Audit of Financial Statements to highlight compliance and thoroughness.

An independent audit report serves as a formal opinion on the fairness of a company's financial statements. After thorough examination, auditors provide their insights based on the applicable accounting standards and regulations. This report is crucial for stakeholders and often serves as the New York Report of Independent Accountants after Audit of Financial Statements, reinforcing financial transparency.

The function of an independent audit is to provide an objective assessment of a company's financial statements. Auditors evaluate the accuracy and completeness of these documents, building trust among stakeholders such as investors and creditors. By obtaining an independent audit, businesses can enhance their credibility, often reflected in the New York Report of Independent Accountants after Audit of Financial Statements.