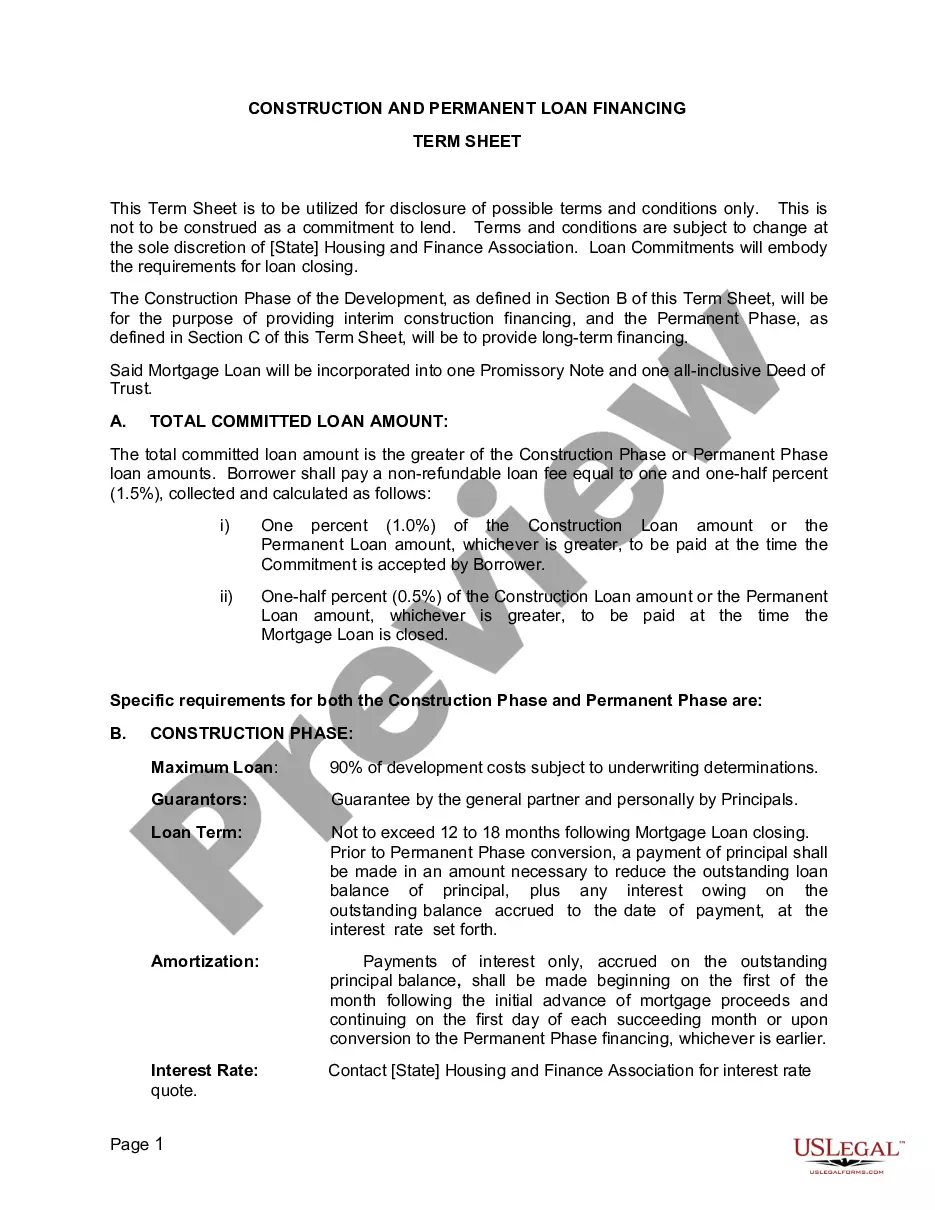

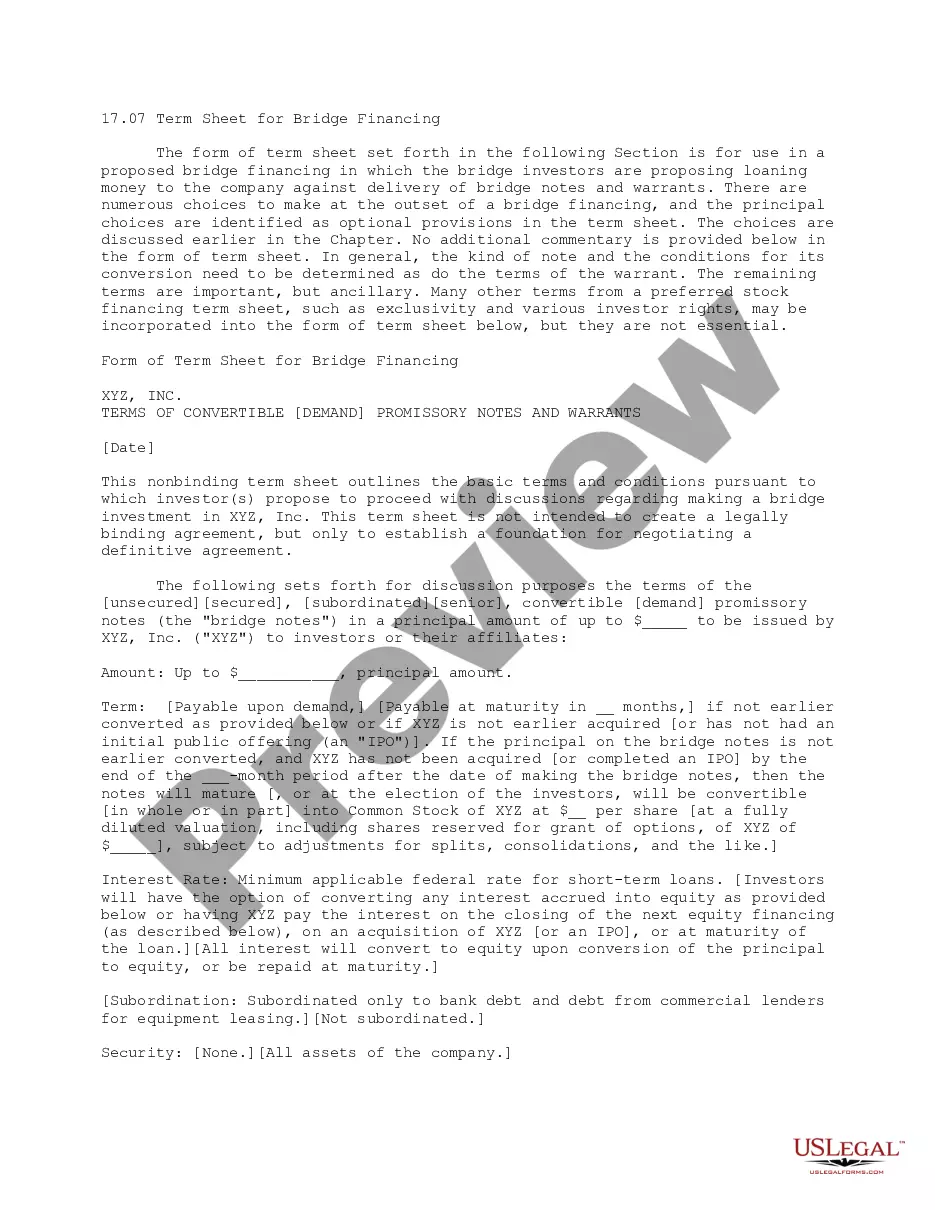

Nevada Construction Loan Financing Term Sheet

Description

How to fill out Construction Loan Financing Term Sheet?

US Legal Forms - one of the biggest libraries of lawful varieties in the States - gives an array of lawful document web templates it is possible to acquire or produce. Using the web site, you can find a huge number of varieties for organization and specific reasons, categorized by types, suggests, or keywords.You can find the newest variations of varieties just like the Nevada Construction Loan Financing Term Sheet in seconds.

If you already have a registration, log in and acquire Nevada Construction Loan Financing Term Sheet from your US Legal Forms local library. The Obtain option will show up on every kind you view. You have access to all formerly downloaded varieties from the My Forms tab of your bank account.

If you want to use US Legal Forms the very first time, listed here are easy instructions to help you get started out:

- Make sure you have chosen the correct kind for your metropolis/state. Click on the Review option to review the form`s articles. Look at the kind description to ensure that you have selected the correct kind.

- If the kind does not fit your requirements, utilize the Research industry towards the top of the display to find the one which does.

- If you are content with the form, affirm your choice by simply clicking the Get now option. Then, opt for the rates program you like and provide your credentials to sign up for an bank account.

- Procedure the financial transaction. Make use of bank card or PayPal bank account to perform the financial transaction.

- Select the format and acquire the form on your own system.

- Make changes. Load, modify and produce and signal the downloaded Nevada Construction Loan Financing Term Sheet.

Each and every web template you put into your bank account lacks an expiration date and is also yours forever. So, in order to acquire or produce one more backup, just proceed to the My Forms portion and then click around the kind you require.

Obtain access to the Nevada Construction Loan Financing Term Sheet with US Legal Forms, one of the most comprehensive local library of lawful document web templates. Use a huge number of specialist and express-particular web templates that satisfy your company or specific demands and requirements.

Form popularity

FAQ

Construction factoring is an increasingly popular financing option among subcontractors. It improves cash flow and provides a financial platform that can be used to grow the business. Most factoring companies finance your invoices by purchasing them rather than offering a loan.

Cons to doing a construction loan would be that payments on the construction loan begin once funds start being disbursed to the builder. With a traditional mortgage, payments don't begin until settlement. Another con is that the interest rates on construction loans are typically higher than on traditional mortgages.

As mentioned, construction loans are short-term loans, usually no longer than a year in length. On the other hand, traditional mortgages are long-term loans, with terms typically ranging from 15 ? 30 years. With a mortgage, the borrower receives the money in one lump sum.

The conversion of construction-to-permanent financing involves the granting of a long-term mortgage to a borrower for the purpose of replacing interim construction financing that the borrower has obtained to fund the construction of a new residence.

If you're looking to build a new home from scratch, you might want to use a construction-to-permanent loan. These loans will cover everything needed to build your dream house but then convert into a conventional mortgage once construction is complete.

Construction-to-permanent financing is a type of loan which allows you to build or renovate your home. When the construction process concludes, this loan rolls over into a traditional mortgage without you having to go through another closing. You'll only have to pay for one set of closing costs.

A construction loan is a short-term loan that covers only the costs of custom home building. This is different from a mortgage, and it's considered specialty financing. Once the home is built, the prospective occupant must apply for a mortgage to pay for the completed home.

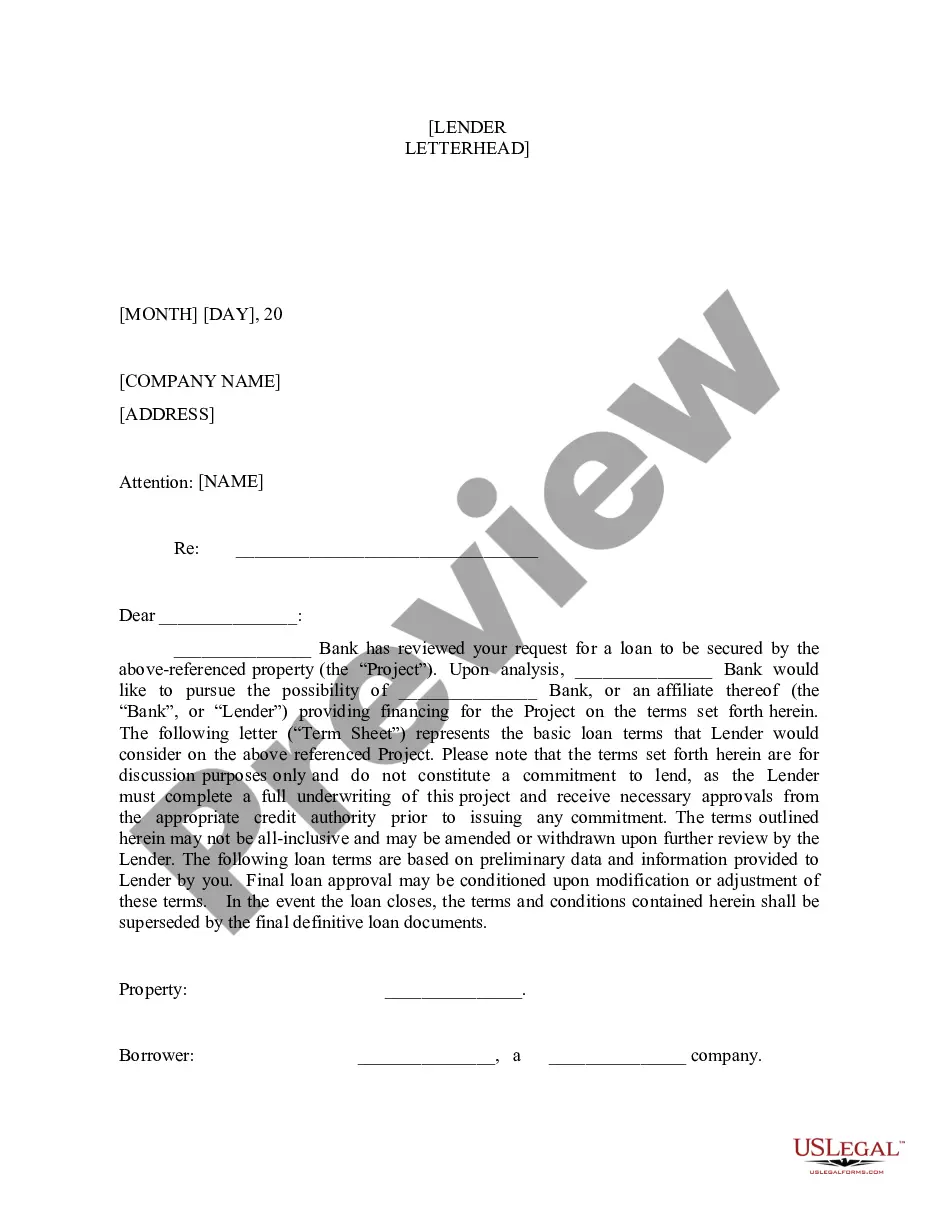

This includes the term, loan size, interest rate, and other financial matters common to debt. Risk mitigation preferences. The lender will often require specific conditions be met or specific information be provided on a recurring, timely manner.