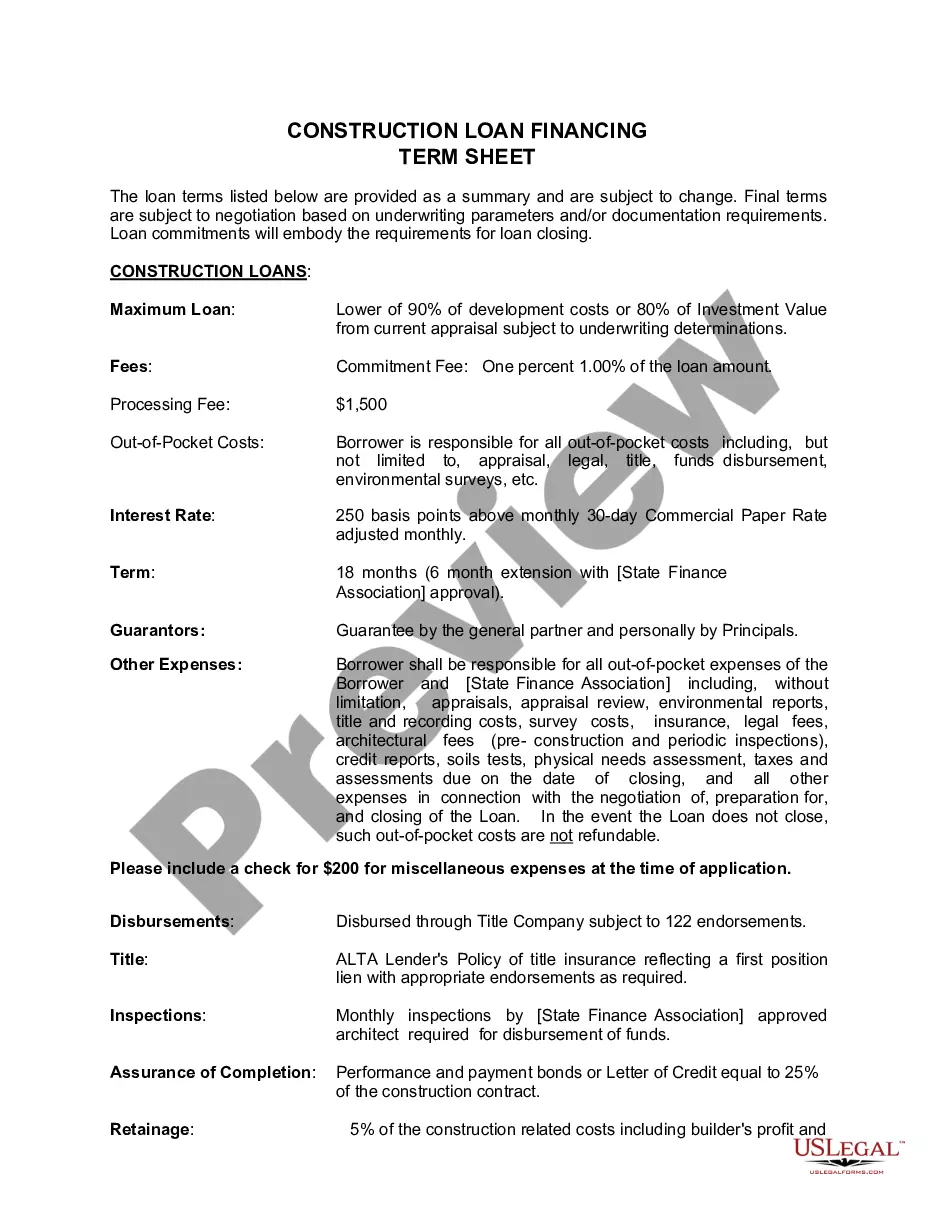

Nevada Construction Loan Financing Term Sheet

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Construction Loan Financing Term Sheet?

You may invest hrs on the web looking for the legal record design that meets the state and federal requirements you will need. US Legal Forms offers a huge number of legal kinds which are examined by pros. It is possible to down load or produce the Nevada Construction Loan Financing Term Sheet from the service.

If you already possess a US Legal Forms accounts, you can log in and click on the Download button. Afterward, you can complete, modify, produce, or indicator the Nevada Construction Loan Financing Term Sheet. Every legal record design you buy is your own permanently. To get one more copy of the acquired develop, proceed to the My Forms tab and click on the corresponding button.

If you use the US Legal Forms site the very first time, follow the basic guidelines under:

- Very first, ensure that you have selected the correct record design for the county/town of your liking. Browse the develop information to make sure you have selected the right develop. If accessible, take advantage of the Preview button to check with the record design at the same time.

- If you would like discover one more version of your develop, take advantage of the Search industry to discover the design that meets your requirements and requirements.

- Upon having identified the design you want, click on Purchase now to continue.

- Find the pricing prepare you want, enter your qualifications, and register for a free account on US Legal Forms.

- Complete the deal. You can utilize your charge card or PayPal accounts to cover the legal develop.

- Find the formatting of your record and down load it for your system.

- Make changes for your record if needed. You may complete, modify and indicator and produce Nevada Construction Loan Financing Term Sheet.

Download and produce a huge number of record layouts utilizing the US Legal Forms site, which offers the most important variety of legal kinds. Use skilled and state-specific layouts to handle your business or specific requires.

Form popularity

FAQ

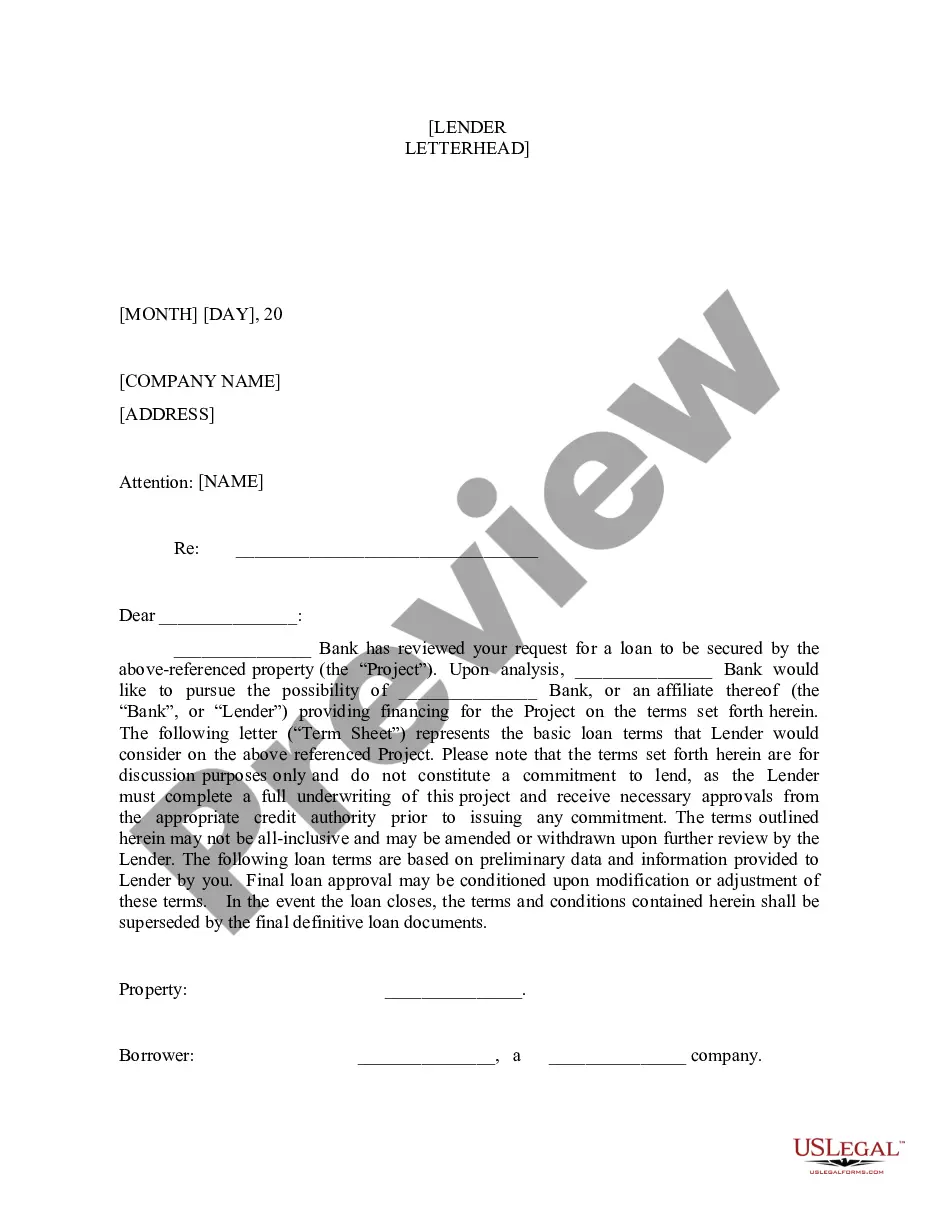

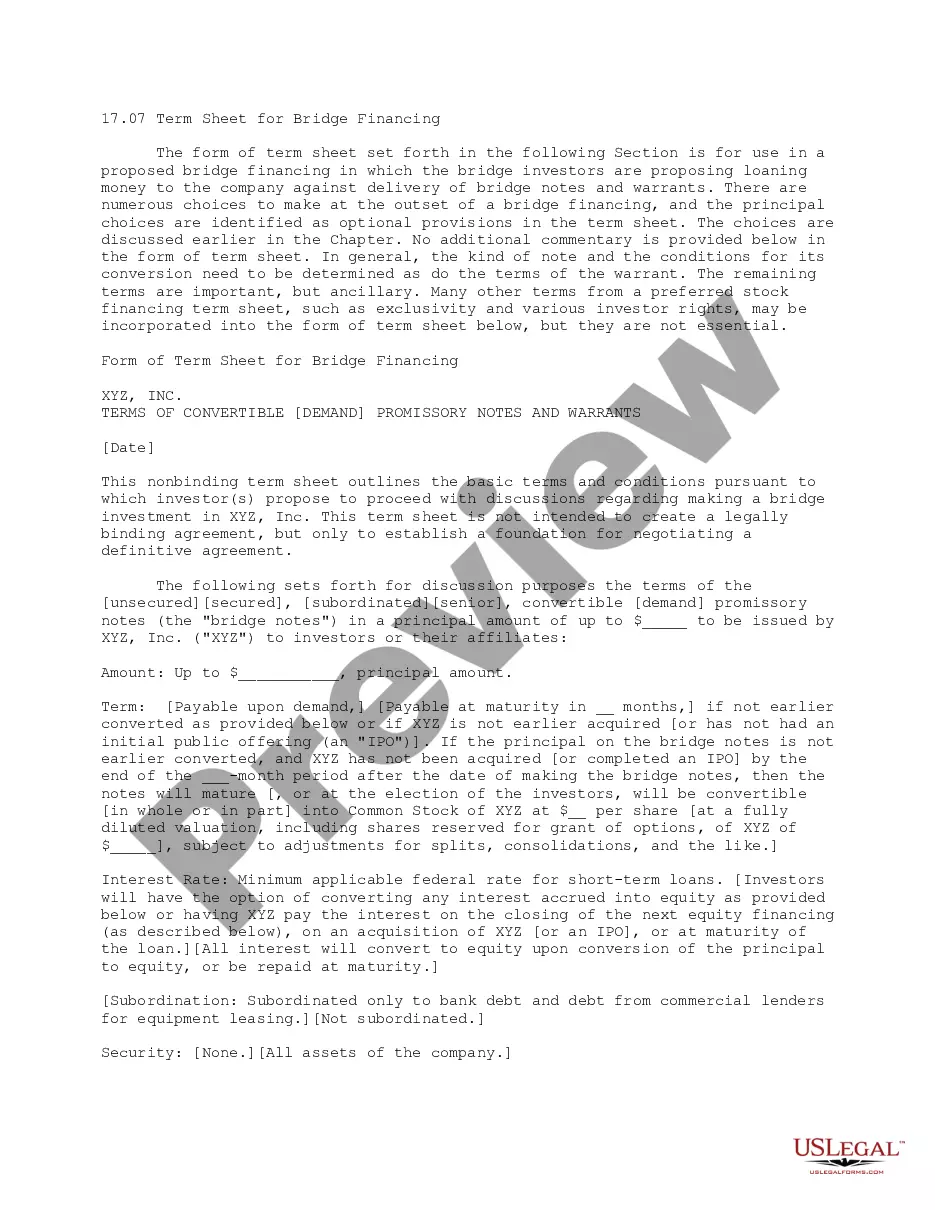

This includes the term, loan size, interest rate, and other financial matters common to debt. Risk mitigation preferences. The lender will often require specific conditions be met or specific information be provided on a recurring, timely manner.

Construction loans are short-term loans funded in increments over the project's construction. The borrower pays interest only on the outstanding balance, so interest charges grow as the project progresses.

A major feature of a construction loan is that the total approved loan amount is not usually given to the borrower right away, in one lump sum. Instead, the construction loan operates more like a line of credit from which the borrower can access funds as needed at various stages of the construction project.

Construction factoring is an increasingly popular financing option among subcontractors. It improves cash flow and provides a financial platform that can be used to grow the business. Most factoring companies finance your invoices by purchasing them rather than offering a loan.

In a project finance transaction, a set of conditions a project company must satisfy once the project has achieved substantial completion or final completion to convert a construction loan to a term loan. Failure to satisfy these conditions may result in the immediate repayment of the construction loan.

Here are a few potential outcomes: Personal Financial Responsibility: If you are responsible for covering the additional costs, you may need to contribute additional funds from your own pocket to cover the overage. This can strain your personal finances and potentially disrupt your financial plans.

As mentioned, construction loans are short-term loans, usually no longer than a year in length. On the other hand, traditional mortgages are long-term loans, with terms typically ranging from 15 ? 30 years. With a mortgage, the borrower receives the money in one lump sum.

Construction-to-permanent financing is a type of loan which allows you to build or renovate your home. When the construction process concludes, this loan rolls over into a traditional mortgage without you having to go through another closing. You'll only have to pay for one set of closing costs.