This form is a business type form that is formatted to allow you to complete the form using Adobe Acrobat or Word. The word files have been formatted to allow completion by entry into fields. Some of the forms under this category are rather simple while others are more complex. The formatting is worth the small cost.

Nevada Balance Sheet Deposits

Category:

State:

Multi-State

Control #:

US-122-AZ

Format:

Word;

PDF;

Rich Text

Instant download

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Built-in online Word editor

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Export easily

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

E-sign your document

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

Notarize online 24/7

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

Store your document securely

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Balance Sheet Deposits?

You can dedicate time online looking for the legal documents template that meets the state and federal requirements you desire.

US Legal Forms offers a vast array of legal forms that are reviewed by experts.

You can actually download or print the Nevada Balance Sheet Deposits from our services.

If available, use the Review button to navigate through the document template as well. If you want to find another version of the form, use the Search area to locate the template that suits you and your needs.

- If you already possess a US Legal Forms account, you can sign in and click on the Obtain button.

- After that, you can complete, edit, print, or sign the Nevada Balance Sheet Deposits.

- Each legal document template you receive is yours permanently.

- To obtain another copy of any acquired form, go to the My documents tab and click on the corresponding button.

- If you are using the US Legal Forms site for the first time, follow the simple instructions listed below.

- First, ensure that you have selected the correct document template for the area/town of your choice.

- Read the form description to make sure you have chosen the appropriate form.

Form popularity

FAQ

When documenting a security deposit on a balance sheet, classify it as an asset. You can include it under current assets if you expect to receive it back within a year, or under non-current assets for longer-term deposits. This classification aligns with the representation of Nevada Balance Sheet Deposits, aiding clear financial disclosure. Accurate recording ensures stakeholders understand the financial position concerning liabilities.

To account for deposits on the balance sheet, classify them as current or non-current assets based on their expected use within the upcoming year. Record the deposit amounts under the appropriate category, ensuring they accurately reflect the company's liquidity. Tools like USLegalForms assist in documenting Nevada Balance Sheet Deposits clearly.

To prepare a balance sheet from a bank statement, start by reviewing all transactions for the reporting period. Categorize deposits as assets and withdrawals as liabilities. Once categorized, summarize the totals to reflect your financial position on the balance sheet. This method can enhance your understanding of Nevada Balance Sheet Deposits.

Maintaining a business balance sheet involves tracking your company's assets and liabilities closely. Regular updates and reconciliations are essential to reflect the current financial state accurately. Consider using uslegalforms for efficient management of your Nevada Balance Sheet Deposits, which can streamline this process and promote clarity.

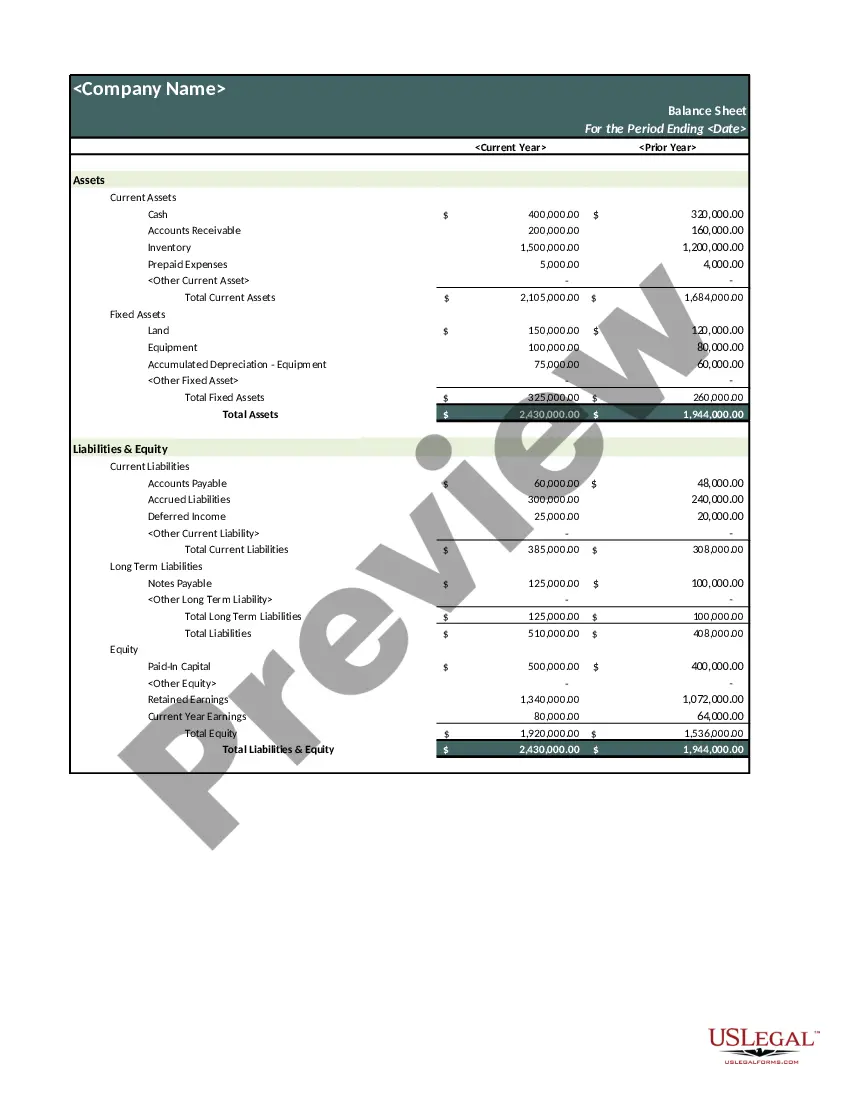

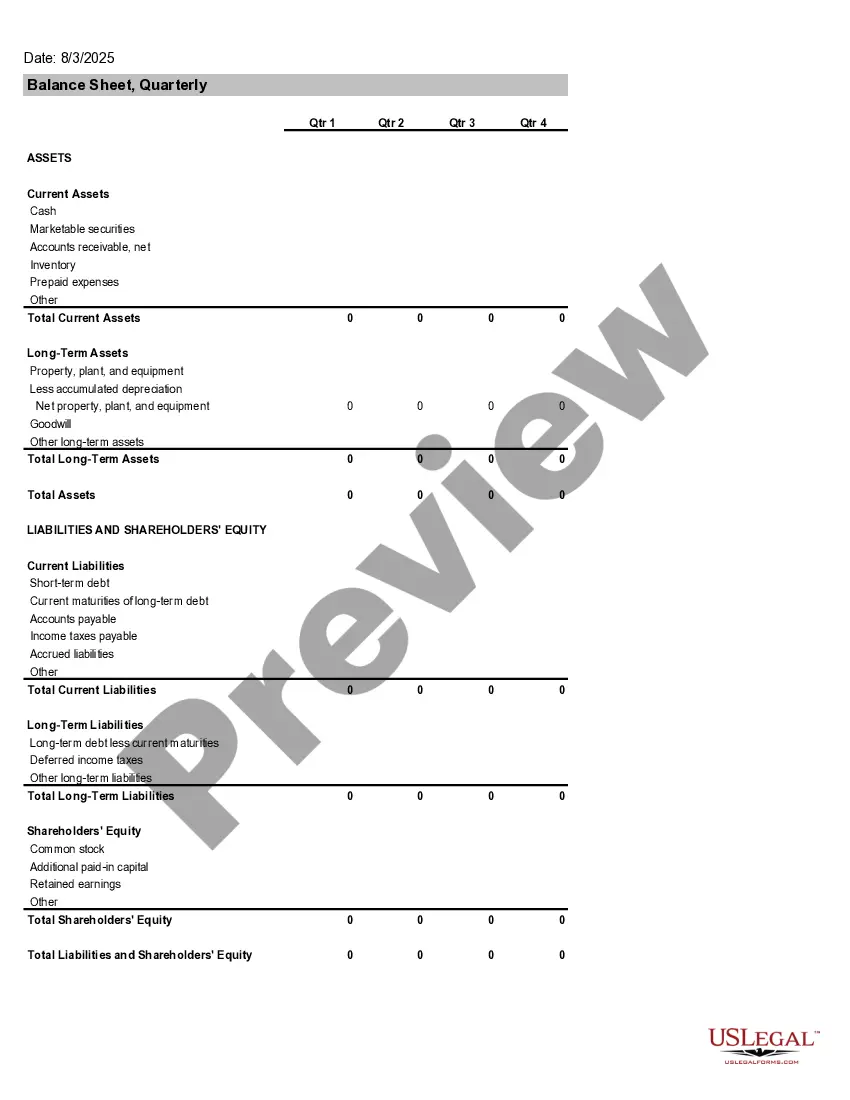

The balance sheet includes information about a company's assets and liabilities. Depending on the company, this might include short-term assets, such as cash and accounts receivable, or long-term assets such as property, plant, and equipment (PP&E).

Finally, the Division of Financial Institutions (commonly referred to as the Financial Institutions Division FID) of Nevada's Department of Business and Industry charters and regulates State banks under the provisions of Title 55 (Banks and Related Organizations) of Nevada Revised Statutes (NRS).

Balance sheets are typically prepared monthly, quarterly and annually, but you can prepare one at any time to show your firm's position.

National banks must be members of the Federal Reserve System; however, they are regulated by the Office of the Comptroller of the Currency (OCC). The Federal Reserve supervises and regulates many large banking institutions because it is the federal regulator for bank holding companies (BHCs).

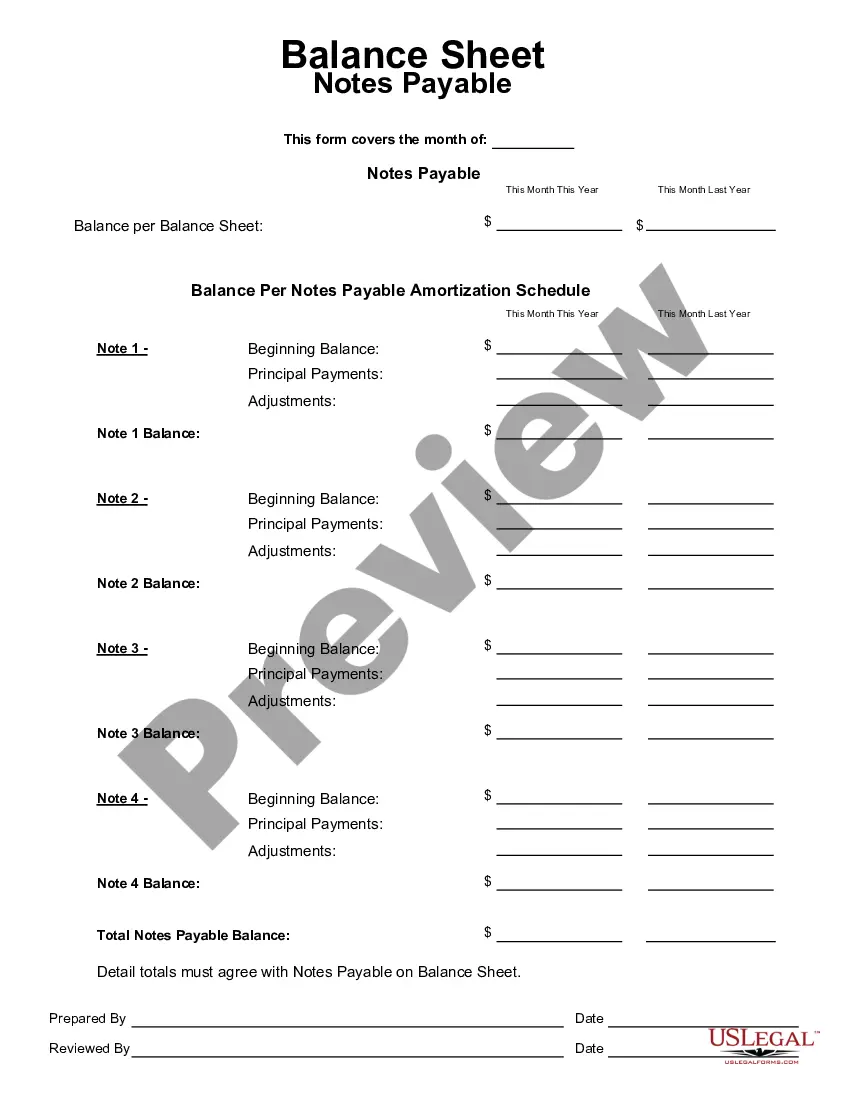

Deposits is a current liability account in the general ledger, in which is stored the amount of funds paid by customers in advance of a product or service delivery. These funds are essentially down payments.

A customer deposit is usually classified as a current liability, since the company typically provides services or goods within one year of the deposit being made. If the deposit is for a longer-term project that will not be resolved within one year, it could instead be classified as a long-term liability.