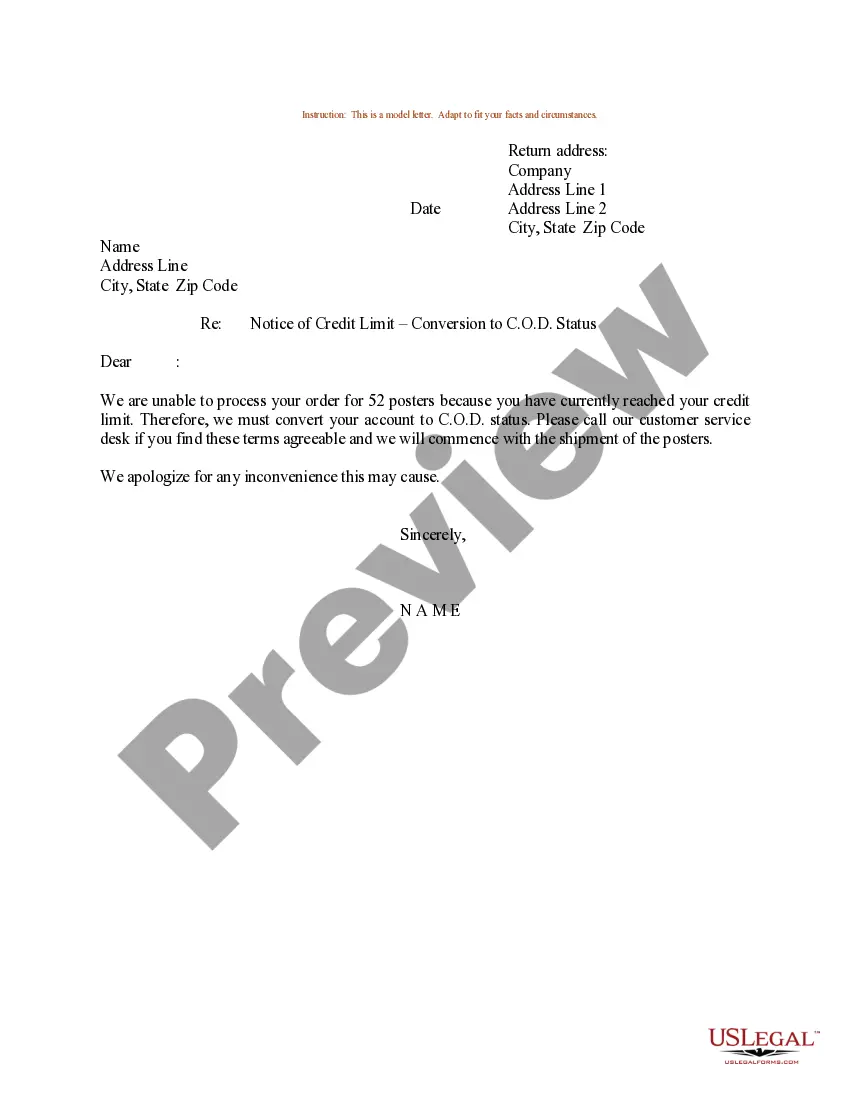

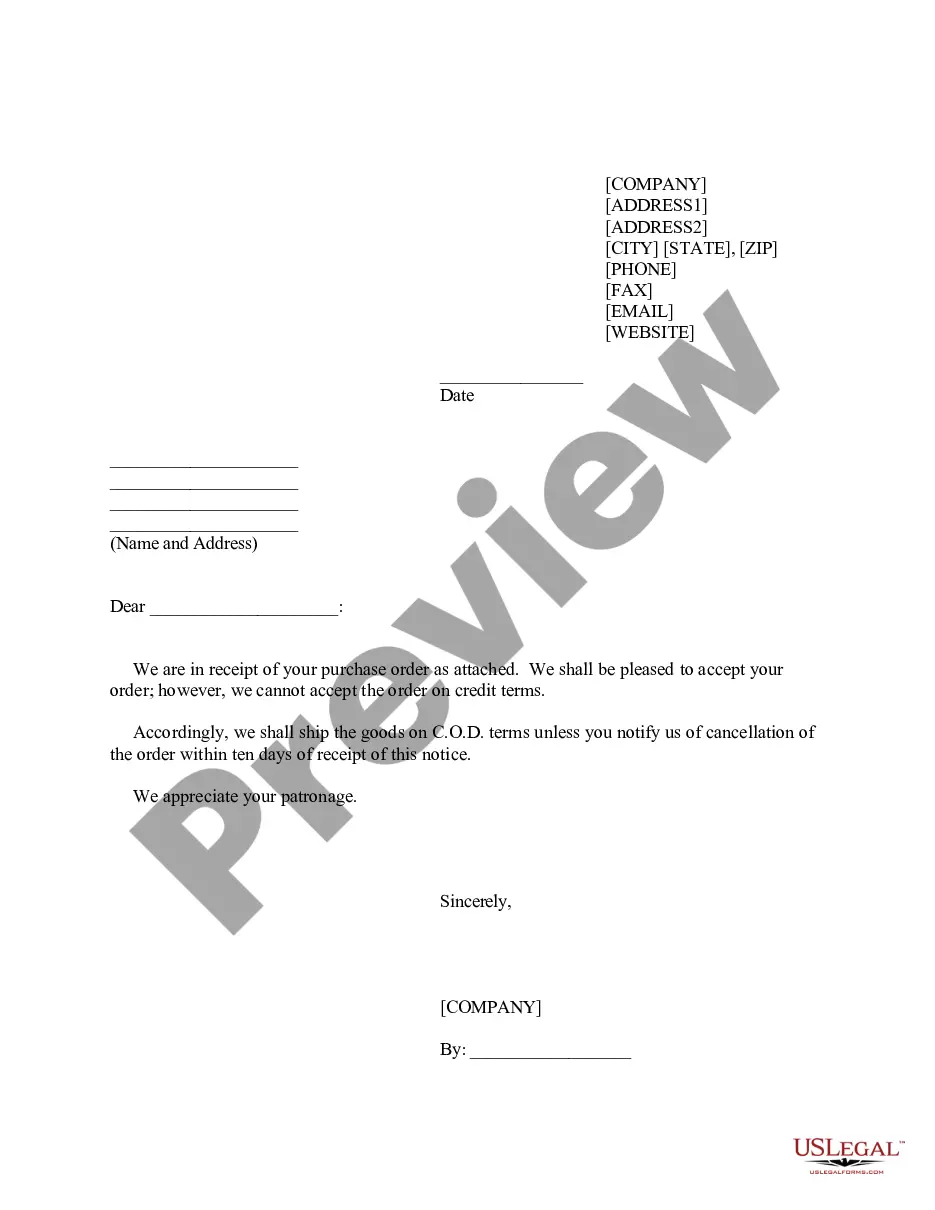

New Mexico Notice of C.O.D. Terms

Description

How to fill out Notice Of C.O.D. Terms?

Finding the right authorized file template can be quite a struggle. Obviously, there are a variety of layouts available on the Internet, but how will you find the authorized form you want? Take advantage of the US Legal Forms internet site. The support offers a huge number of layouts, like the New Mexico Notice of C.O.D. Terms, which you can use for enterprise and private requirements. All of the varieties are checked by pros and meet up with state and federal demands.

In case you are currently registered, log in for your account and click the Down load option to have the New Mexico Notice of C.O.D. Terms. Utilize your account to appear throughout the authorized varieties you might have purchased formerly. Check out the My Forms tab of your own account and obtain yet another backup from the file you want.

In case you are a new consumer of US Legal Forms, listed below are straightforward instructions that you should stick to:

- Initial, ensure you have selected the proper form for your personal town/state. You can look over the form making use of the Preview option and look at the form description to guarantee this is the best for you.

- In the event the form is not going to meet up with your requirements, use the Seach industry to find the right form.

- Once you are certain the form is proper, go through the Purchase now option to have the form.

- Pick the costs plan you desire and type in the required information and facts. Make your account and pay money for the transaction using your PayPal account or bank card.

- Opt for the data file structure and obtain the authorized file template for your product.

- Complete, edit and print out and signal the received New Mexico Notice of C.O.D. Terms.

US Legal Forms may be the largest collection of authorized varieties in which you can find numerous file layouts. Take advantage of the service to obtain skillfully-created paperwork that stick to condition demands.

Form popularity

FAQ

Generally, if you borrow money from a commercial lender and the lender later cancels or forgives the debt, you may have to include the cancelled amount in income for tax purposes. The lender is usually required to report the amount of the canceled debt to you and the IRS on a Form 1099-C, Cancellation of Debt.

Unless debt cancellation comes in the form of bankruptcy or debt settlement, cancellation of debt doesn't always impact your credit score. However, debt cancellation may not be all good news for you. In some cases, you may have to pay taxes on canceled debt, as the government may consider it taxable income.

If you can demonstrate to the IRS that you were insolvent at the time the debt was cancelled, you can similarly avoid taxes on that debt. Certain other types of debt, including qualified farm indebtedness and qualified real property business indebtedness, can also avoid taxation in the event of cancellation.

The creditor that sent you the 1099-C also sent a copy to the IRS. If you don't acknowledge the form and income on your own tax filing, it could raise a red flag. Red flags could result in an audit or having to prove to the IRS later that you didn't owe taxes on that money.

The gain or loss on such a ?sale? is separate from any cancellation of debt income that you need to include on your return. If you don't report the taxable amount of the canceled debt, the IRS may send you a notice proposing to assess additional tax and may audit your tax return.

If your debt is forgiven or discharged for less than the full amount owed, the debt is considered canceled for the forgiven or discharged amount that you no longer need to pay. Cancellation of a debt may occur if the creditor can't collect, or gives up on collecting, the amount you're obligated to pay.

IRC section 6050P states: Certain lenders that cancel a debt of $600 or more required to file Form 1099-C with the IRS and issue a copy to the borrower. Taxpayers must report all Form 1099-C income on their returns.

The amount of income reported from debt cancellation is generally the difference between outstanding debt owed and any amount paid to settle the obligation. The amount paid to settle a debt includes any money paid and/or the fair market value of property transferred to the lender.