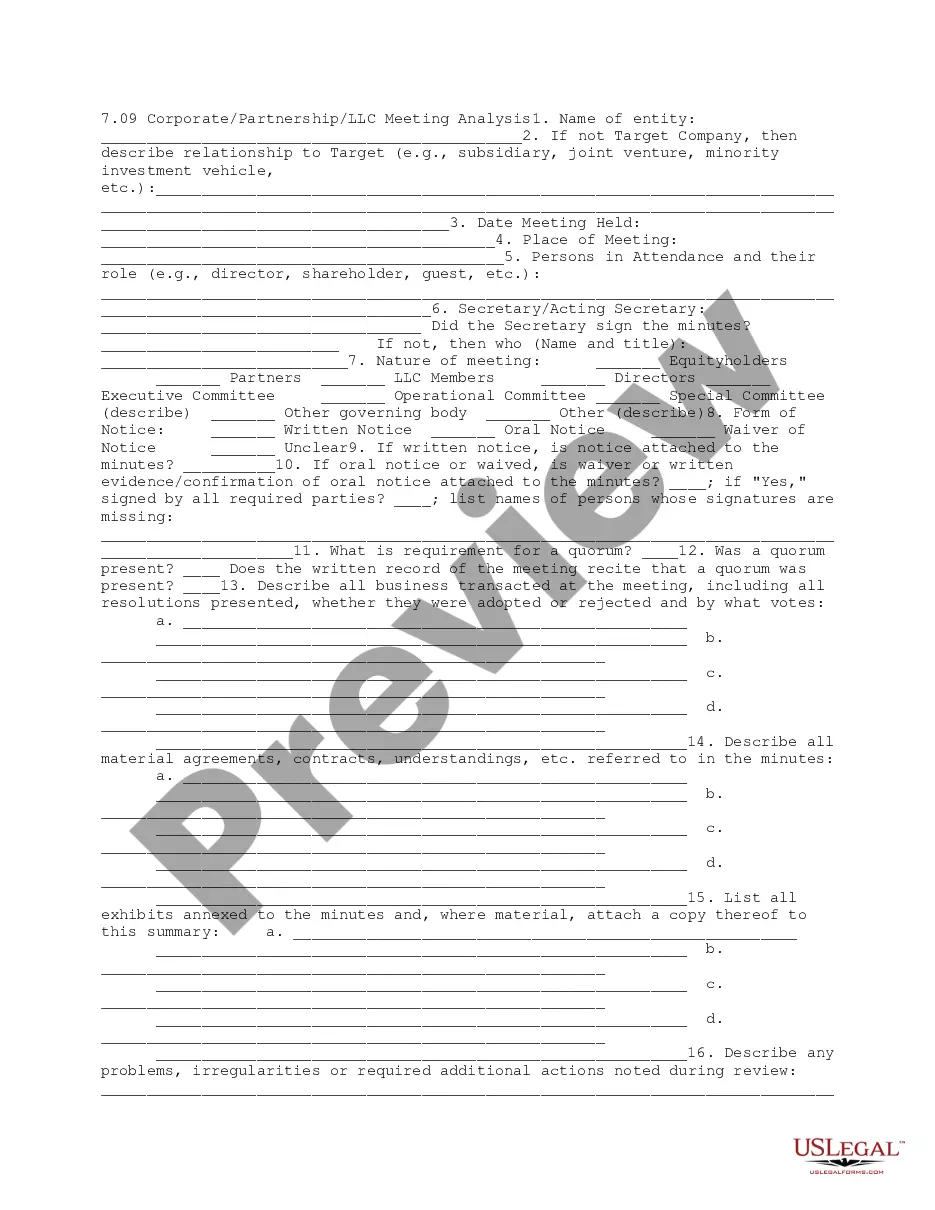

This due diligence form is used to summarize data for each partnership entity associated with the company in business transactions.

New Jersey Partnership Data Summary

Category:

State:

Multi-State

Control #:

US-DD0706

Format:

Word;

PDF;

Rich Text

Instant download

Description

Free preview

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Built-in online Word editor

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Export easily

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

E-sign your document

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

Notarize online 24/7

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

Store your document securely

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Partnership Data Summary?

Are you in a scenario where you require documentation for various business or personal reasons nearly every single day.

There are numerous legal document templates accessible online, but locating ones you can trust is not easy.

US Legal Forms offers a wide array of form templates, such as the New Jersey Partnership Data Summary, crafted to meet state and federal requirements.

Once you identify the correct form, simply click Buy now.

Choose the payment plan you prefer, complete the necessary details to create your account, and pay for the order using your PayPal or credit card. Select a convenient document format and download your copy. Access all the document templates you have purchased in the My documents section. You can retrieve another copy of the New Jersey Partnership Data Summary anytime if needed. Click the required form to download or print the document template. Use US Legal Forms, the most extensive collection of legal forms, to save time and avoid mistakes. The service offers properly constructed legal document templates that can be utilized for a variety of purposes. Create an account on US Legal Forms and start making your life a bit easier.

- If you are already familiar with the US Legal Forms website and have an account, simply Log In.

- Then, you can download the New Jersey Partnership Data Summary template.

- If you do not have an account and want to start using US Legal Forms, follow these steps.

- Find the form you need and ensure it is for the correct city/region.

- Utilize the Review button to inspect the form.

- Read the description to confirm that you have selected the appropriate form.

- If the form is not what you're looking for, use the Lookup field to find the form that meets your requirements.

Form popularity

FAQ

Any individual or entity earning income in New Jersey is required to file a state tax return. This includes residents and non-residents who earn income from New Jersey sources. Understanding filing requirements is crucial when creating your New Jersey Partnership Data Summary, as it ensures compliance for all partners. Utilizing our platform can make navigating these requirements straightforward and efficient.

A partnership return must be filed by any business partnership operating within New Jersey, including both general and limited partnerships. This requirement ensures transparency in financial activities and compliance with state tax regulations. By compiling a comprehensive New Jersey Partnership Data Summary, you can ensure all necessary filings are complete. Let our platform guide you through the partnership return process effortlessly.

In New Jersey, a significant number of individuals earn more than $100,000 annually. This statistic is vital for understanding the state's economic landscape and can impact partnership income levels. When compiling your New Jersey Partnership Data Summary, this data point helps in planning and strategizing for partnerships. Our tools can assist you in analyzing income trends within your partnership structure.

The New Jersey Partnership Act governs the formation, operation, and dissolution of partnerships in the state. This legislation outlines the rights and responsibilities of partners and provides a framework for resolving disputes. Knowing the key principles of the New Jersey Partnership Act can enhance your New Jersey Partnership Data Summary. Our platform offers resources to support your understanding and compliance with these legal standards.

In New Jersey, any partnership doing business within the state must file a partnership tax return. This includes partnerships with income, even if it is under New Jersey's threshold for taxation. By creating a New Jersey Partnership Data Summary, partnerships can ensure compliance with state regulations. Our platform simplifies this process, helping you meet your filing requirements efficiently.

Partnerships generally need to fill out Form 1065 to report their financial activities. This form is critical for providing a clear New Jersey Partnership Data Summary, which breaks down each partner's share of income and helps in their tax filings. Additionally, if applicable, partnerships may need to issue K-1 forms to their partners, making it a key part of the tax process.

The $500 check in New Jersey is part of a broader program aimed at financial relief for residents. However, eligibility can vary based on certain criteria such as income and household size. To stay informed about initiatives like this, consider tracking updates from local government sources alongside your financial reporting through New Jersey Partnership Data Summary.

No, Form 1065 is not the same as a K-1. Form 1065 is for the partnership to report income and expenses, while the K-1 is a schedule sent to each partner detailing their share of the income, deductions, and credits from the partnership. The information from both forms contributes to a comprehensive New Jersey Partnership Data Summary.

An LLC classified as a partnership typically files Form 1065. This allows the LLC to provide a clear New Jersey Partnership Data Summary for each member's share of income. If the LLC elects to be treated as an S corporation, it would then file Form 1120S instead.

Not all partnerships are required to file a K-2. A K-2 is necessary when a partnership has foreign income or deductions that need to be reported. If your partnership’s financial activities are straightforward, you may focus primarily on the New Jersey Partnership Data Summary via Form 1065.