New Jersey Sample Letter transmitting Cancellation and Satisfaction of Promissory Notes

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Sample Letter Transmitting Cancellation And Satisfaction Of Promissory Notes?

US Legal Forms - one of the largest collections of legal documents in the USA - provides a range of legal document formats that you can download or print.

By utilizing the site, you will access numerous forms for business and personal needs, categorized by type, state, or keywords. You can find the latest versions of forms such as the New Jersey Sample Letter sending Cancellation and Satisfaction of Promissory Notes within minutes.

If you have a subscription, Log In and download the New Jersey Sample Letter sending Cancellation and Satisfaction of Promissory Notes from your US Legal Forms library. The Download button will appear on every form you view. You have access to all previously downloaded forms in the My documents tab of your account.

Complete the transaction. Use your credit card or PayPal account to finalize the purchase.

Select the format and download the form to your device. Edit, complete, and print the downloaded New Jersey Sample Letter sending Cancellation and Satisfaction of Promissory Notes.

Every template you add to your account has no expiration date and is yours indefinitely. Therefore, if you wish to download or print another copy, simply go to the My documents section and click on the form you need. Access the New Jersey Sample Letter sending Cancellation and Satisfaction of Promissory Notes with US Legal Forms, one of the most comprehensive libraries of legal document formats. Utilize thousands of professional and state-specific templates that cater to your business or personal requirements.

- Ensure you have selected the correct form for your state/region.

- Click the Review button to examine the details of the form.

- Check the form overview to confirm you have the correct one.

- If the form does not fit your needs, use the Search field at the top of the screen to find one that does.

- When satisfied with the form, confirm your choice by clicking the Buy now button.

- Then, choose the payment plan you prefer and provide your information to sign up for an account.

Form popularity

FAQ

In order for a promissory note to be valid and legally binding, it needs to include specific information. "A promissory note should include details including the amount loaned, the repayment schedule and whether it is secured or unsecured," says Wheeler.

Even if you have the original note, it may be void if it was not written correctly. If the person you're trying to collect from didn't sign it and yes, this happens the note is void. It may also become void if it failed some other law, for example, if it was charging an illegally high rate of interest.

To write a promissory note for a personal loan, you will need to include the names of both parties, the principal balance, the APR, and any fees that are part of the agreement. The promissory note should also clearly explain what will happen if the borrower pays late or does not pay the loan back at all.

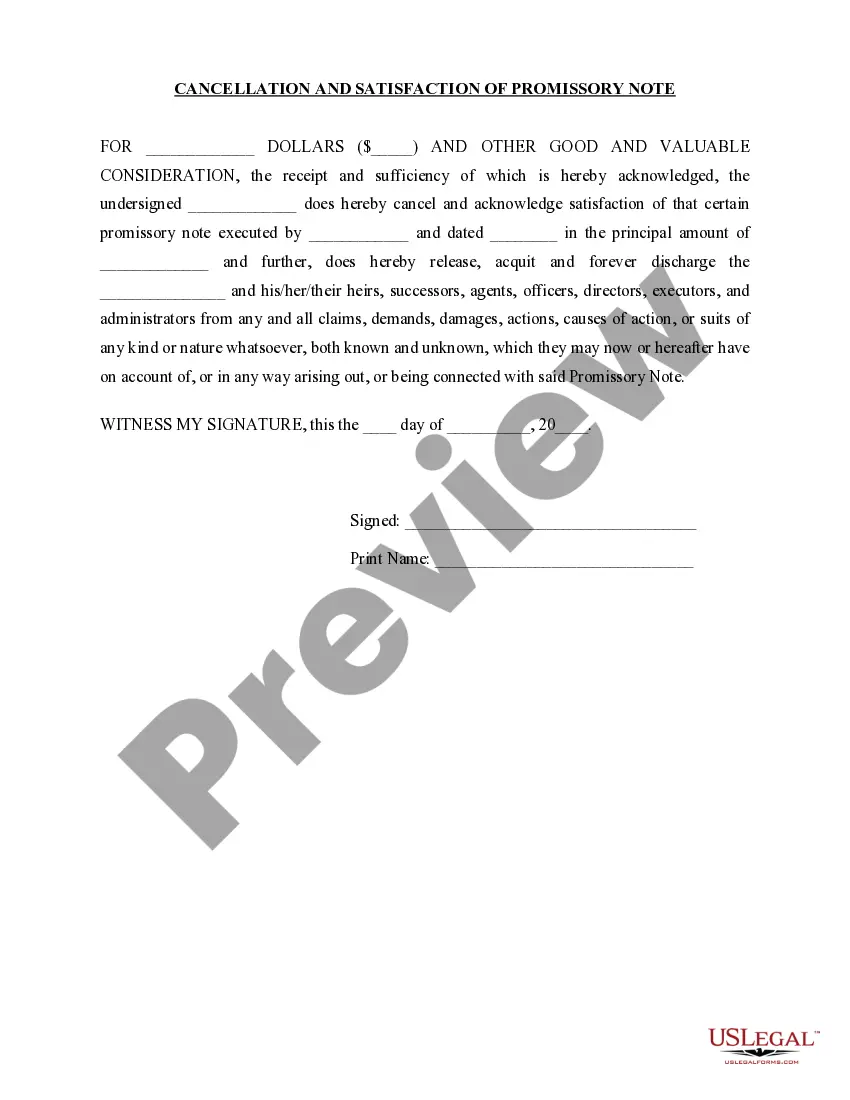

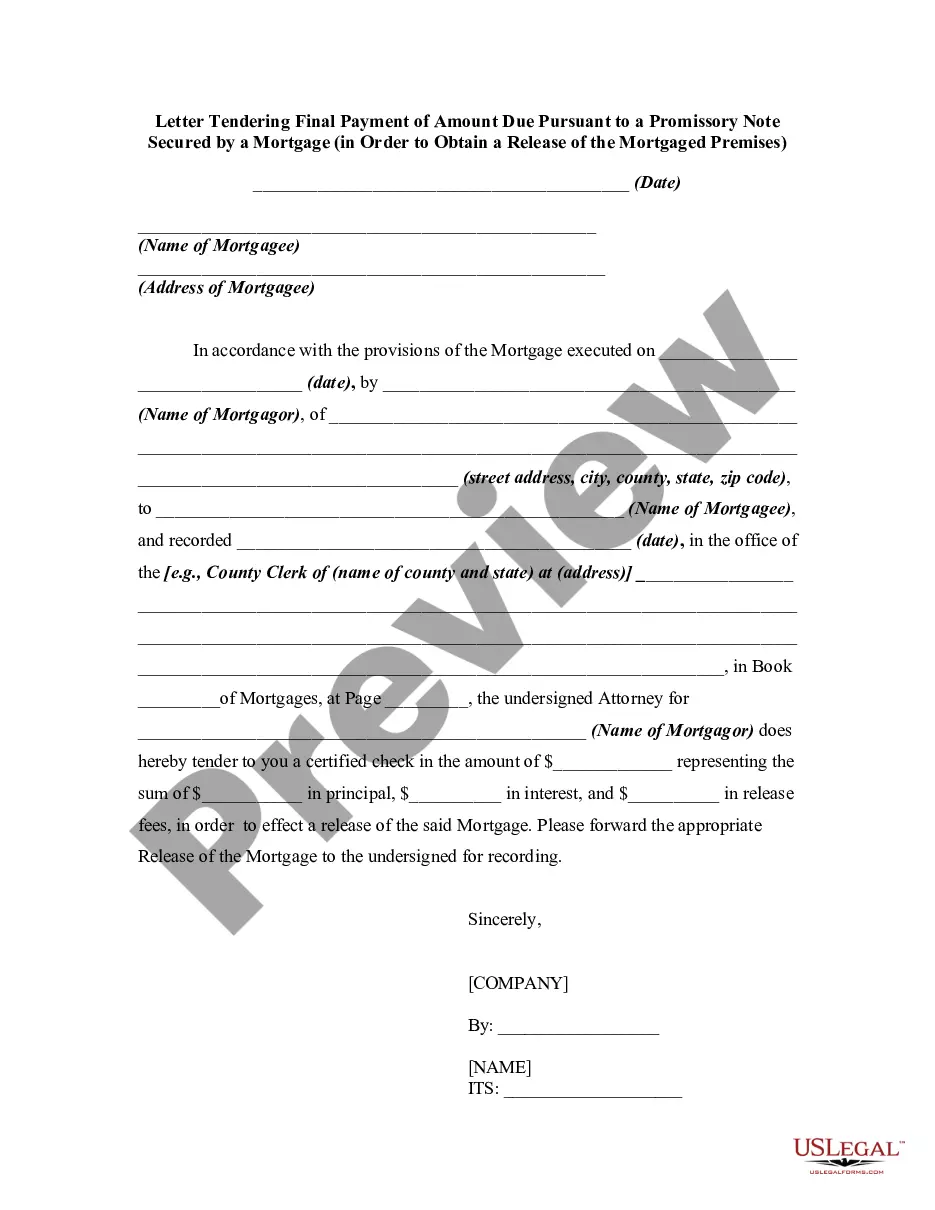

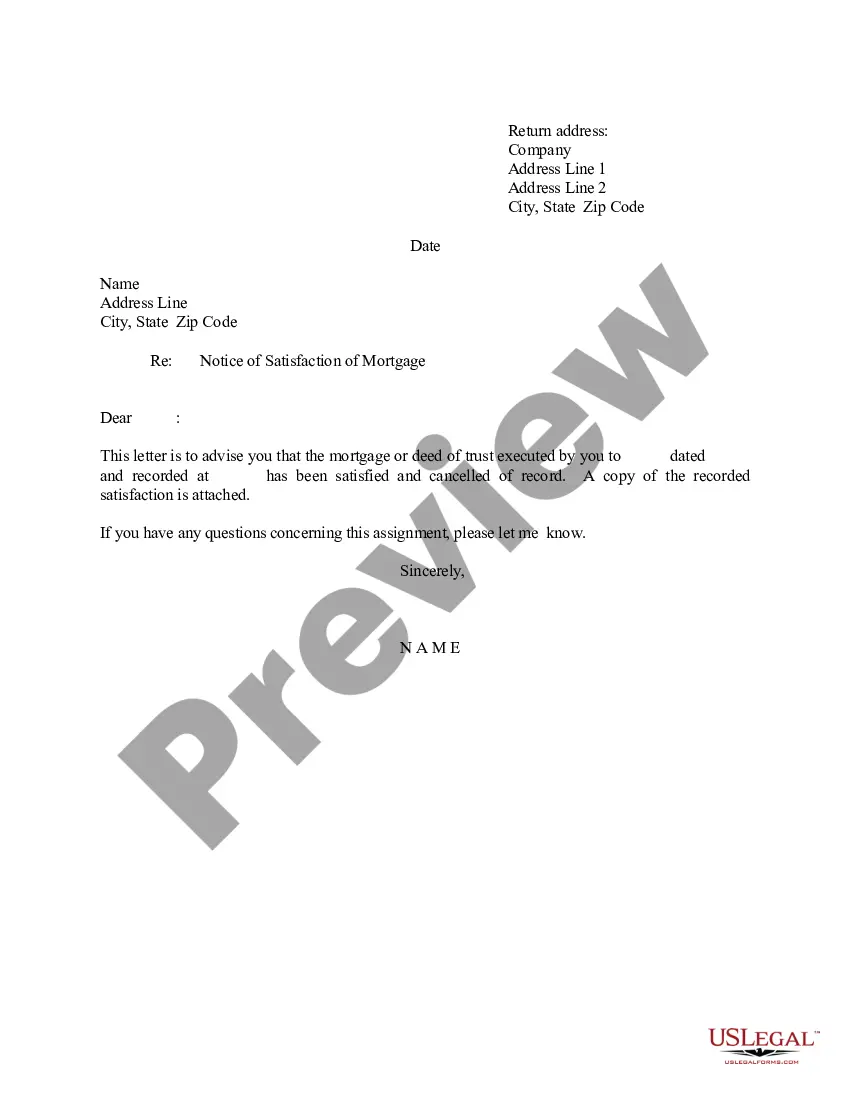

The debt owed on a promissory note either can be paid off, or the noteholder can forgive the debt even if it has not been fully paid. In either case, a release of promissory note needs to be signed by the noteholder.

Give the borrower the original promissory note, with a notation on it that says CANCELLED or PAID IN FULL. Keep a copy of this note for your records.

Write a "Cancellation of Promissory Note" letter or have the attorney write one for you. The note should include details of the original promissory note and also indicate that the original promissory note is canceled at the request of both parties. Have the promisee sign the document in the presence of a notary.

Detailed Information The note has all the required information including the name of the drawer and payee, date of maturity, terms of repayment, issue date, name of the drawee, name, and signature of the drawer, principal amount, and the rate of interest, etc.

How to Write a Promissory NoteDate.Name of the lender and borrower.Loan amount.Whether the loan is secured or unsecured. If it's secured with collateral: What is the collateral?Payment amount and frequency.Payment due date.Whether the loan has a cosigner, and if so, who.

Even if you have the original note, it may be void if it was not written correctly. If the person you're trying to collect from didn't sign it and yes, this happens the note is void. It may also become void if it failed some other law, for example, if it was charging an illegally high rate of interest.

You can use a template or create a promissory note online. But before you begin, you'll need to gather some information and make decisions about the way the loan will be structured. First, you'll need the names and addresses of both the lender (or "payee") and the borrower.