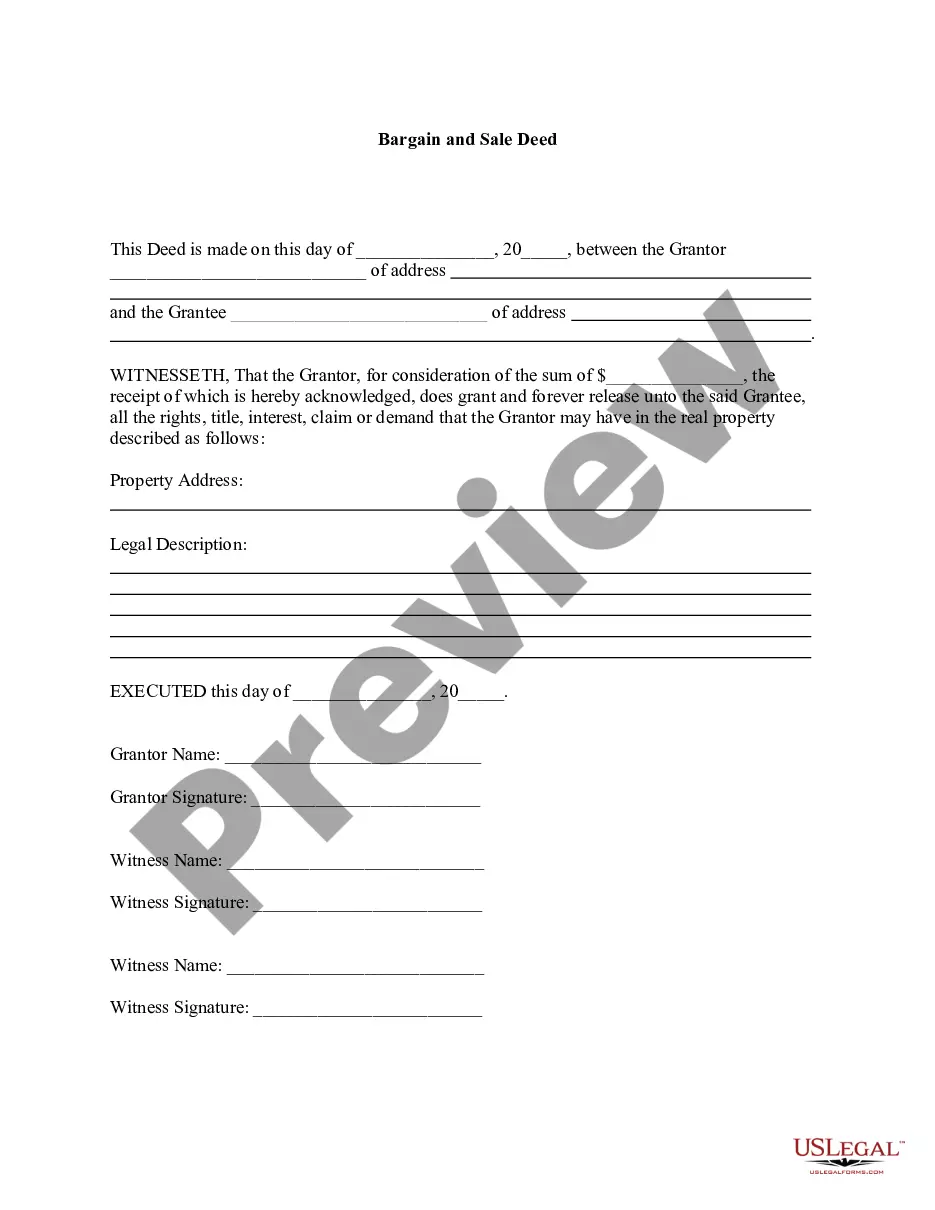

New Jersey Bargain and Sale Deed - With Covenants as to Grantor's Acts

Description

How to fill out New Jersey Bargain And Sale Deed - With Covenants As To Grantor's Acts?

Among hundreds of free and paid templates which you get online, you can't be certain about their reliability. For example, who created them or if they are competent enough to deal with what you require them to. Always keep calm and utilize US Legal Forms! Find New Jersey Bargain and Sale Deed - With Covenants as to Grantor's Acts samples created by professional legal representatives and get away from the high-priced and time-consuming process of looking for an lawyer and then paying them to write a papers for you that you can easily find on your own.

If you have a subscription, log in to your account and find the Download button near the form you’re searching for. You'll also be able to access all of your earlier saved templates in the My Forms menu.

If you are utilizing our service the first time, follow the instructions listed below to get your New Jersey Bargain and Sale Deed - With Covenants as to Grantor's Acts quickly:

- Make sure that the document you discover applies where you live.

- Review the template by reading the description for using the Preview function.

- Click Buy Now to start the purchasing process or look for another template using the Search field in the header.

- Select a pricing plan and create an account.

- Pay for the subscription with your credit/debit/debit/credit card or Paypal.

- Download the form in the preferred format.

When you have signed up and purchased your subscription, you can utilize your New Jersey Bargain and Sale Deed - With Covenants as to Grantor's Acts as many times as you need or for as long as it continues to be valid in your state. Change it with your favorite online or offline editor, fill it out, sign it, and print it. Do a lot more for less with US Legal Forms!

Form popularity

FAQ

When done properly, a deed is recorded anywhere from two weeks to three months after closing.

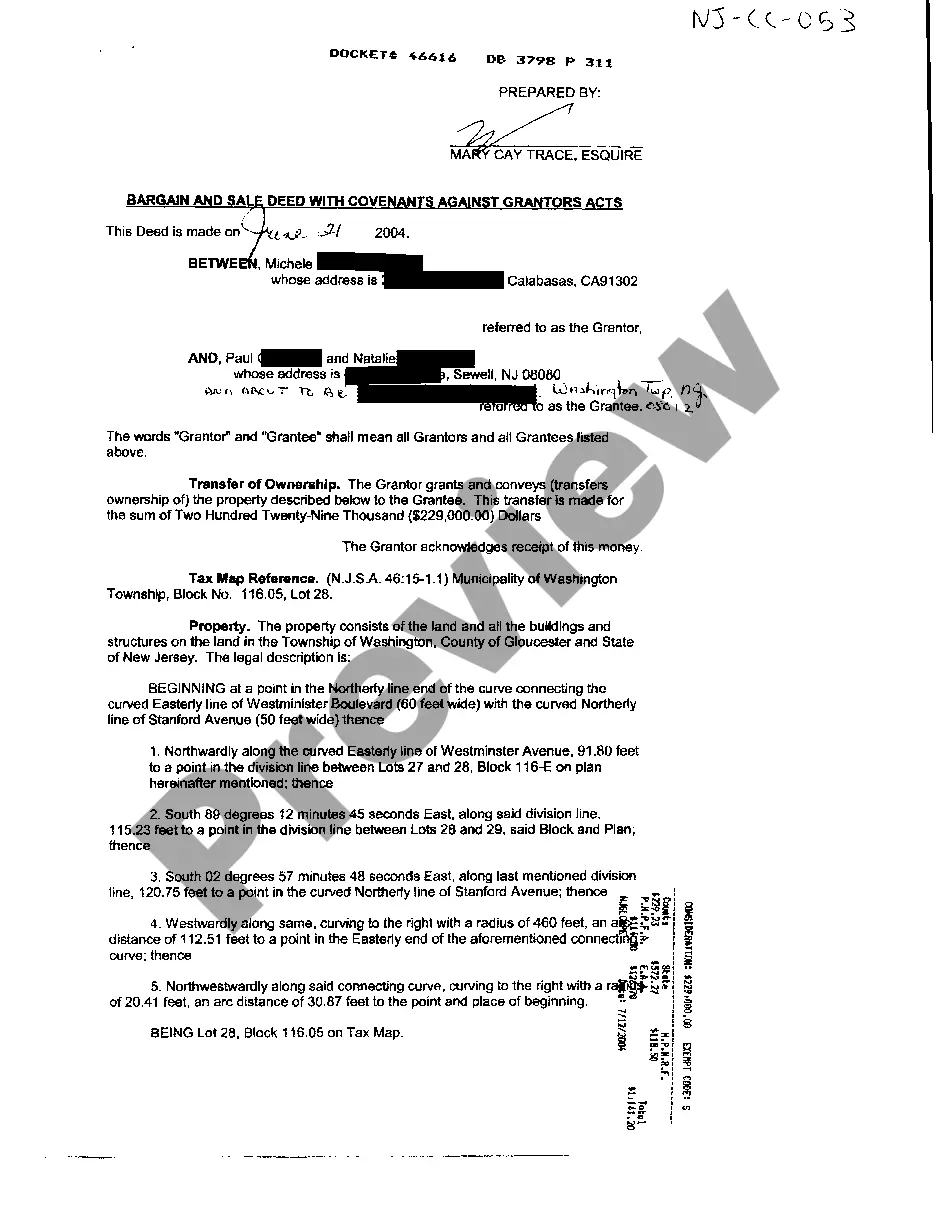

Bargain and Sale With Covenants If a bargain and sale deed comes with expressly stated guarantees beyond simple ownership rights, it is known as a bargain and sale deed with covenants. The grantor of such a deed is guaranteeing the property against any possible claims expressly covered by the covenant.

In its most basic form, a bargain and sale deed includes a warranty that the grantor has title to the property but does not guarantee that the property is free of claims. This is known as a bargain and sale deed without covenants.

In New Jersey, the deed must be in English, identify the seller/buyer (grantor/grantee), name the person that prepared the deed, state the consideration (amount paid) for the transfer, contain a legal description of the property (a survey), include the signature of the grantor and be signed before a notary.

A bargain and sale with covenants against grantor's acts contains only one covenant or promise; that is, that the grantor has done nothing to encumber title with easements, liens, judgements and the like while owing the property.It does not run with the land. This type of deed is typically used in New Jersey.

Be in English or include an English translation (N.J.S.A. Identify the grantor / grantee (N.J.S.A. Be signed by the grantor with the name printed underneath (N.J.S.A. Include the name and mailing address of the grantee (N.J.S.A. Be notarized (N.J.S.A.

Bargain and sale deeds are generally used to transfer the grantor's entire interest in the property at the time of conveyance without any warranties of title.Unlike quitclaim deeds, bargain and sale deeds imply that the grantor holds an actual interest in the property being conveyed.

In New Jersey, the preparation of legal documents such as a deed is considered the practice of law which may only be undertaken by an Attorney at Law of the State of New Jersey. The only exception to that rule is that an individual representing him/herself may prepare his/her own documents.

Retrieve your original deed. Get the appropriate deed form. Draft the deed. Sign the deed before a notary. Record the deed with the county recorder. Obtain the new original deed.