New Hampshire Assignment of Life Insurance as Collateral

Description

How to fill out Assignment Of Life Insurance As Collateral?

US Legal Forms - one of many most significant libraries of legitimate kinds in the USA - offers a variety of legitimate papers web templates it is possible to download or printing. While using internet site, you may get a huge number of kinds for business and individual purposes, sorted by groups, suggests, or keywords.You can get the most up-to-date variations of kinds just like the New Hampshire Assignment of Life Insurance as Collateral in seconds.

If you already possess a monthly subscription, log in and download New Hampshire Assignment of Life Insurance as Collateral from the US Legal Forms library. The Download key can look on every kind you view. You have accessibility to all in the past delivered electronically kinds from the My Forms tab of your account.

In order to use US Legal Forms the first time, allow me to share basic instructions to obtain started off:

- Ensure you have picked the correct kind for your personal metropolis/area. Go through the Preview key to review the form`s content material. Read the kind description to ensure that you have selected the right kind.

- In the event the kind doesn`t fit your specifications, make use of the Look for area on top of the display screen to obtain the one which does.

- When you are happy with the form, verify your selection by visiting the Get now key. Then, select the costs prepare you like and give your references to register for an account.

- Process the transaction. Make use of bank card or PayPal account to accomplish the transaction.

- Choose the file format and download the form on your own system.

- Make modifications. Fill out, change and printing and indicator the delivered electronically New Hampshire Assignment of Life Insurance as Collateral.

Every format you put into your account lacks an expiry date and is also the one you have eternally. So, if you would like download or printing yet another duplicate, just proceed to the My Forms area and then click in the kind you require.

Obtain access to the New Hampshire Assignment of Life Insurance as Collateral with US Legal Forms, by far the most comprehensive library of legitimate papers web templates. Use a huge number of skilled and condition-certain web templates that satisfy your small business or individual requirements and specifications.

Form popularity

FAQ

Unless instructed differently, your life insurance company creates a revocable beneficiary designation when you purchase the policy. If you want to assign an irrevocable beneficiary, let your insurance company know. You may be able to update an existing life insurance policy to include an irrevocable beneficiary.

A collateral assignment supersedes your beneficiaries' rights to the death benefit. If you die, the life insurance company pays the lender, or assignee, the loan balance. As noted earlier, any remaining benefit goes to your beneficiaries.

If you have a life insurance policy, you're in luck, because most businesses typically accept life insurance as collateral as they can guarantee funds if the borrower dies or defaults.

The collateral assignment is irrevocable as established by a written agreement preventing the holder of the life insurance policy from affecting or using the cash surrender value after the irrevocable assignment.

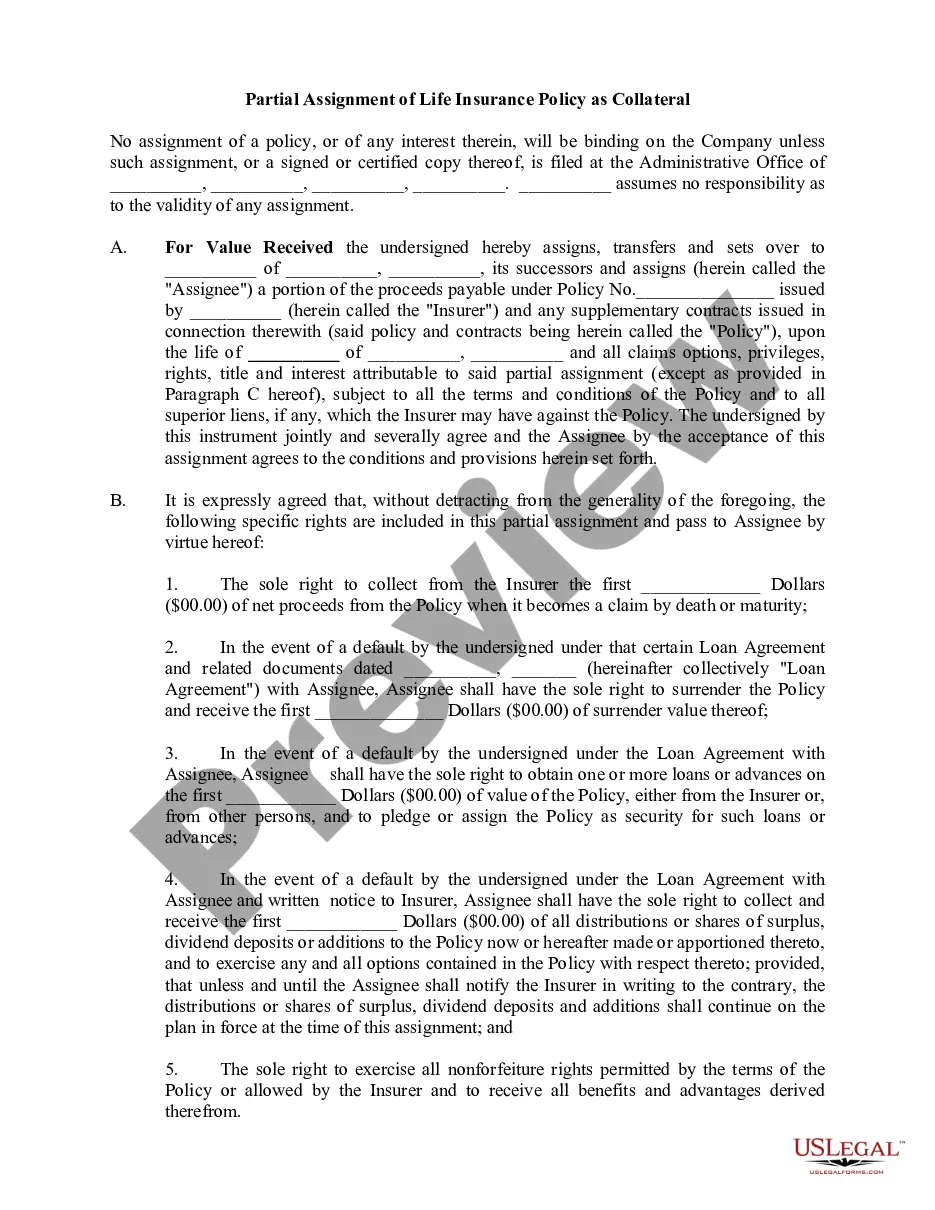

Collateral assignment of life insurance is a method of providing a lender with collateral when you apply for a loan. In this case, the collateral is your life insurance policy's face value, which could be used to pay back the amount you owe in case you die while in debt.

You can use either term or whole life insurance policy as collateral, but the death benefit must meet the lender's terms. Alternately, the policy owner's access to the cash value is restricted to protect the collateral.

The irrevocable assignment includes: Irrevocably assigns and transfers all the benefits and proceeds of the life insurance policy to the funeral home/funeral director. The cash value is not counted as an available asset. The life insurance cannot be canceled.

Any type of life insurance policy is acceptable for collateral assignment, provided the insurance company allows assignment for the policy. Some banks may require an escrow account for the life insurance premiums, others may require proof of premiums paid or prepaid.