New Hampshire MHA Request for Short Sale

Description

How to fill out MHA Request For Short Sale?

US Legal Forms - one of the foremost collections of legal documents in the United States - provides a variety of legal form templates that you can download or create.

By using the website, you can access thousands of forms for business and personal purposes, organized by categories, states, or keywords. You can obtain the latest versions of forms such as the New Hampshire MHA Request for Short Sale in moments.

If you already have an account, Log In to access the New Hampshire MHA Request for Short Sale in the US Legal Forms library. The Download button will appear on every form you view. You can access all previously downloaded forms from the My documents section of your account.

Make changes. Complete, modify, and print and sign the downloaded New Hampshire MHA Request for Short Sale.

Every template you add to your account has no expiration date and is yours indefinitely. So, if you want to download or create another copy, just navigate to the My documents section and click on the form you need.

- If you are using US Legal Forms for the first time, here are simple instructions to get started.

- Make sure you have selected the correct form for your city/county. Click the Review button to view the form's details. Read the form description to ensure you have chosen the right one.

- If the form does not meet your requirements, use the Search field at the top of the screen to find one that does.

- If you are satisfied with the form, confirm your choice by clicking the Buy now button. Then, select your preferred payment plan and provide your credentials to sign up for an account.

- Process the payment. Use your credit card or PayPal account to complete the transaction.

- Select the format and download the form to your device.

Form popularity

FAQ

The amount a bank accepts on a short sale typically depends on various factors, including the property's market value and the seller's situation. Banks may consider offers significantly lower than the mortgage balance, often accepting 80% or less of the market value. When initiating your New Hampshire MHA Request for Short Sale, it’s essential to provide a well-supported offer to help the bank make a favorable decision.

Yes, New Hampshire is a judicial foreclosure state, meaning that all foreclosures must go through the court system. This process can extend the timeline for homeowners and adds layers of complexity to property sales. Knowing this can be crucial when considering options like a New Hampshire MHA Request for Short Sale, as it could offer alternate pathways to resolving your mortgage issues.

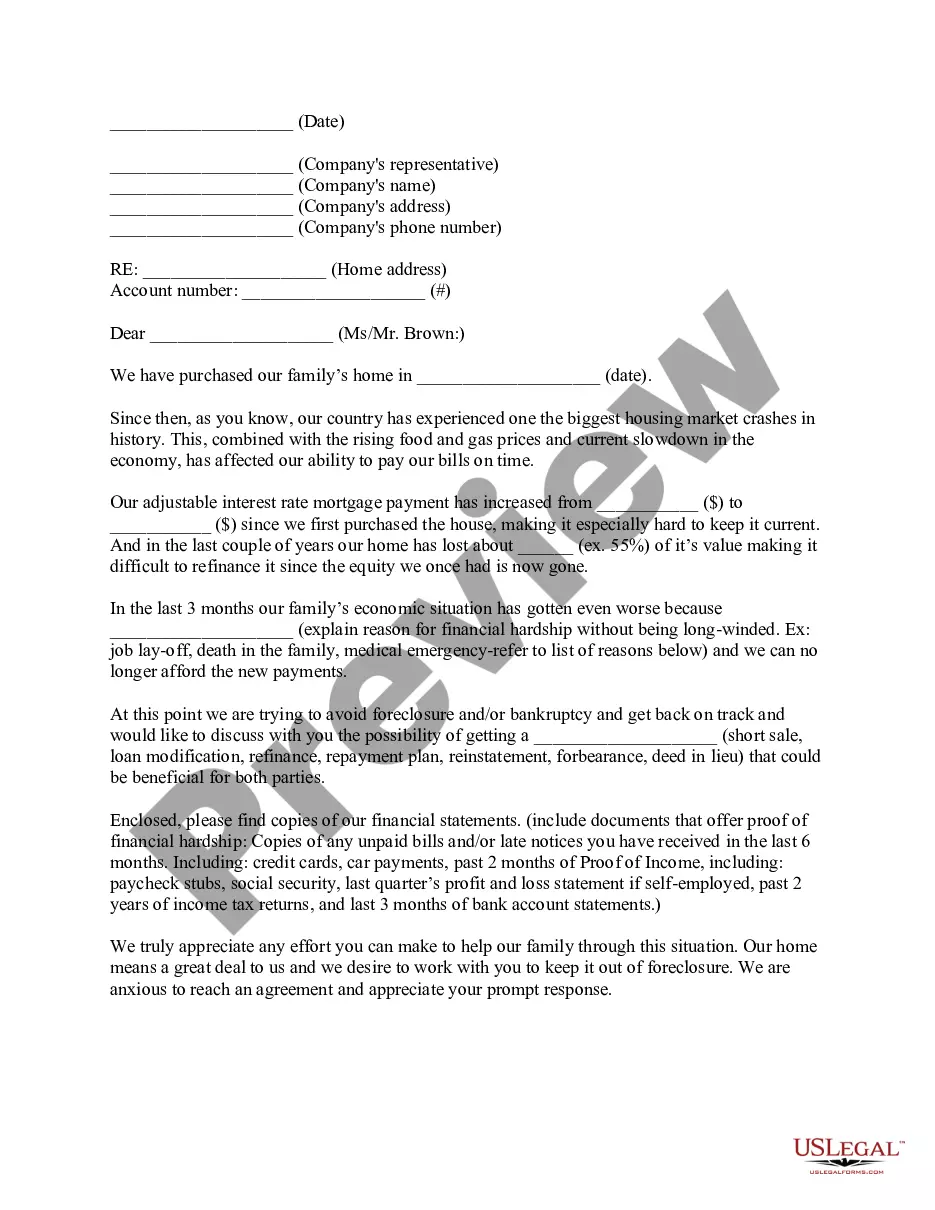

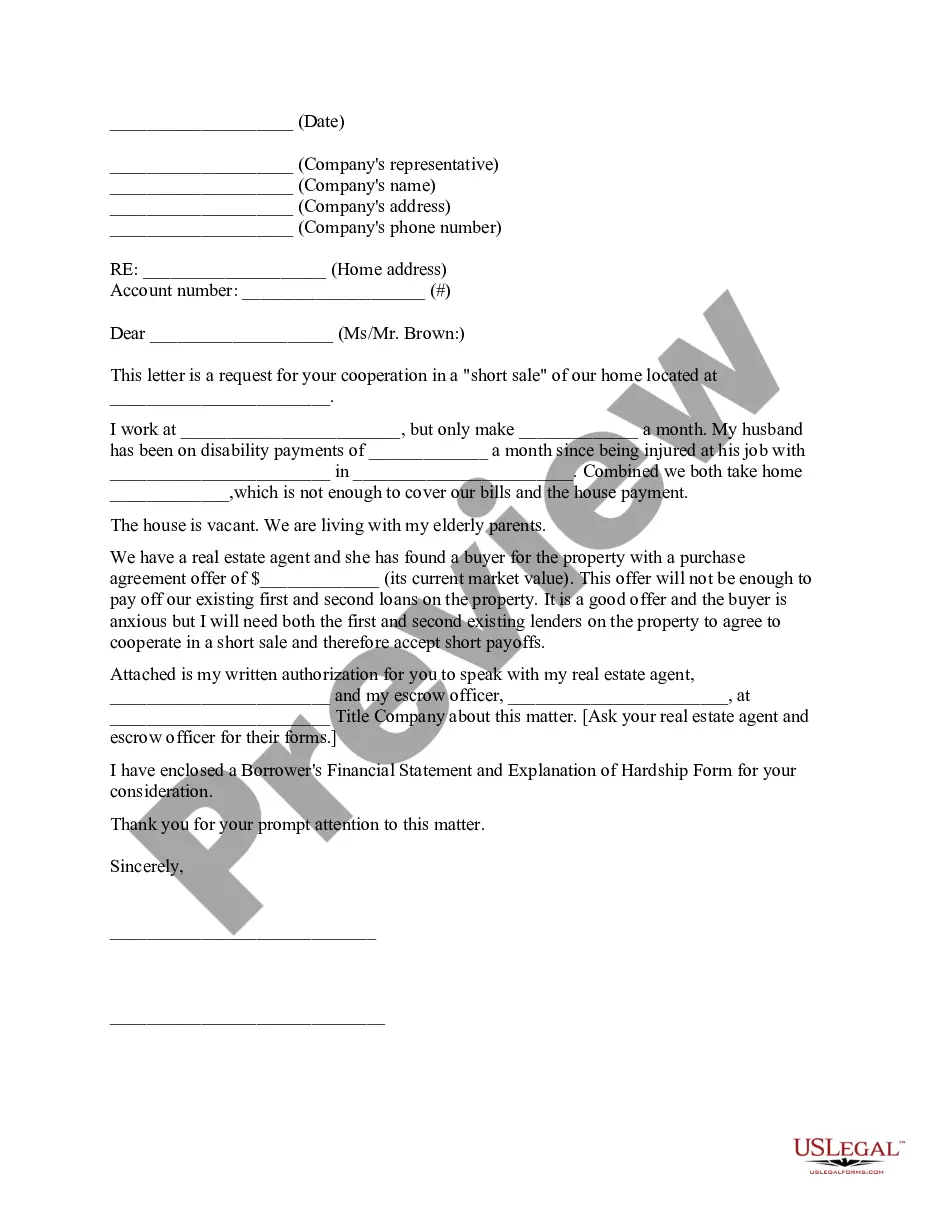

To request a short sale, first contact your lender to express your interest and discuss your situation. Provide them with necessary documentation to support your New Hampshire MHA Request for Short Sale, such as financial statements and hardship letters. Your lender will then assess your request as part of the approval process.

Qualifying for a short sale generally involves proving financial hardship, which can include job loss, medical expenses, or a decrease in property value. Your lender will review your situation based on your financial circumstances and the specifics of your New Hampshire MHA Request for Short Sale. Meeting these qualifications may increase your chances of approval.

To ask for a short sale, start by discussing your financial situation with your lender. You will need to provide documentation that shows your financial hardship, which is key in supporting your New Hampshire MHA Request for Short Sale. Once you gather the necessary paperwork, submit a formal request to your lender to evaluate your case for a short sale.

Short sales can have an impact on your credit score, but they may be less damaging than a foreclosure. When you complete a New Hampshire MHA Request for Short Sale, the process typically results in a 'settled' status on your credit report, which still reflects negatively but not as severely. Typically, credit scores can recover faster after a short sale compared to a foreclosure.

The New Hampshire Land Sales Full Disclosure Act is a law that requires sellers of land to provide detailed information about the properties they plan to sell. This act ensures that buyers receive vital information, helping them make informed decisions when considering purchasing land. If you're exploring options like the New Hampshire MHA Request for Short Sale, understanding this Act is essential in navigating property sales.

The hardship relief program in New Hampshire offers assistance to homeowners facing financial difficulties, helping them manage their mortgage payments. Eligible participants can apply for programs that may include the New Hampshire MHA Request for Short Sale, which facilitates selling their home to escape foreclosure. This program aims to reduce the adverse impact of financial hardships by providing options for those in need. Exploring these resources can provide the necessary support during tough times.

Foreclosure in New Hampshire typically takes between 90 to 150 days, depending on various factors such as the lender’s actions and court schedules. During this time, homeowners may explore options like the New Hampshire MHA Request for Short Sale as an alternative to losing their property. This process allows homeowners to sell their property at market value, potentially avoiding foreclosure altogether. Staying informed and proactive can help you navigate this challenging situation effectively.