New Hampshire Construction Loan Financing Term Sheet

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Construction Loan Financing Term Sheet?

Discovering the right legal record template can be a have a problem. Obviously, there are tons of layouts available online, but how would you find the legal type you will need? Utilize the US Legal Forms website. The service gives 1000s of layouts, for example the New Hampshire Construction Loan Financing Term Sheet, which you can use for business and private demands. All the kinds are examined by professionals and satisfy state and federal specifications.

Should you be already registered, log in to the profile and click on the Down load button to find the New Hampshire Construction Loan Financing Term Sheet. Make use of profile to check from the legal kinds you possess bought earlier. Check out the My Forms tab of your own profile and get yet another version of the record you will need.

Should you be a new user of US Legal Forms, here are straightforward guidelines that you can comply with:

- Initial, ensure you have selected the correct type to your town/county. You may look over the shape utilizing the Review button and read the shape explanation to guarantee this is basically the right one for you.

- In the event the type fails to satisfy your expectations, utilize the Seach field to find the correct type.

- Once you are certain the shape is proper, click on the Acquire now button to find the type.

- Select the prices program you would like and enter the essential information and facts. Create your profile and pay money for an order using your PayPal profile or credit card.

- Select the submit structure and download the legal record template to the device.

- Comprehensive, edit and produce and signal the acquired New Hampshire Construction Loan Financing Term Sheet.

US Legal Forms is definitely the greatest catalogue of legal kinds for which you can find numerous record layouts. Utilize the company to download appropriately-created documents that comply with state specifications.

Form popularity

FAQ

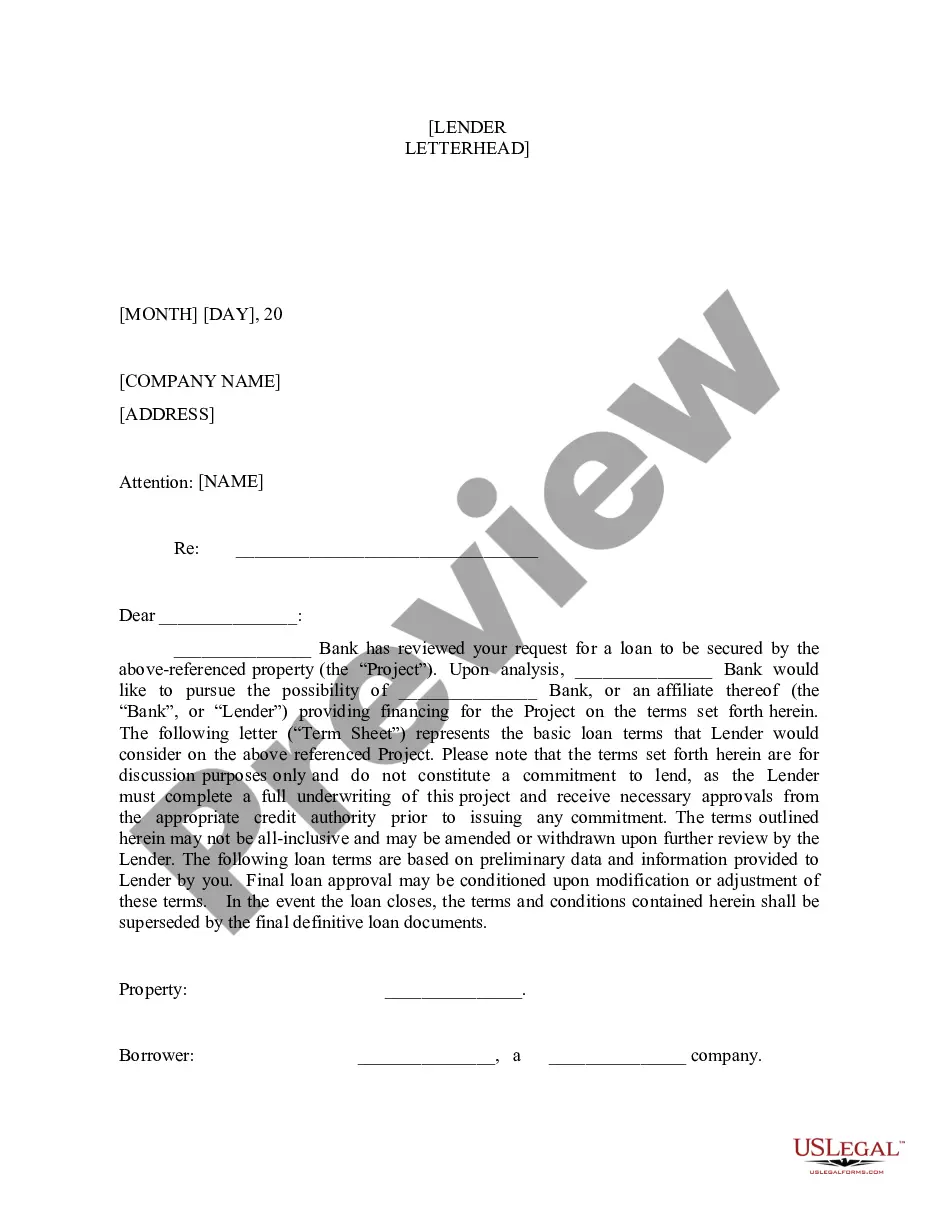

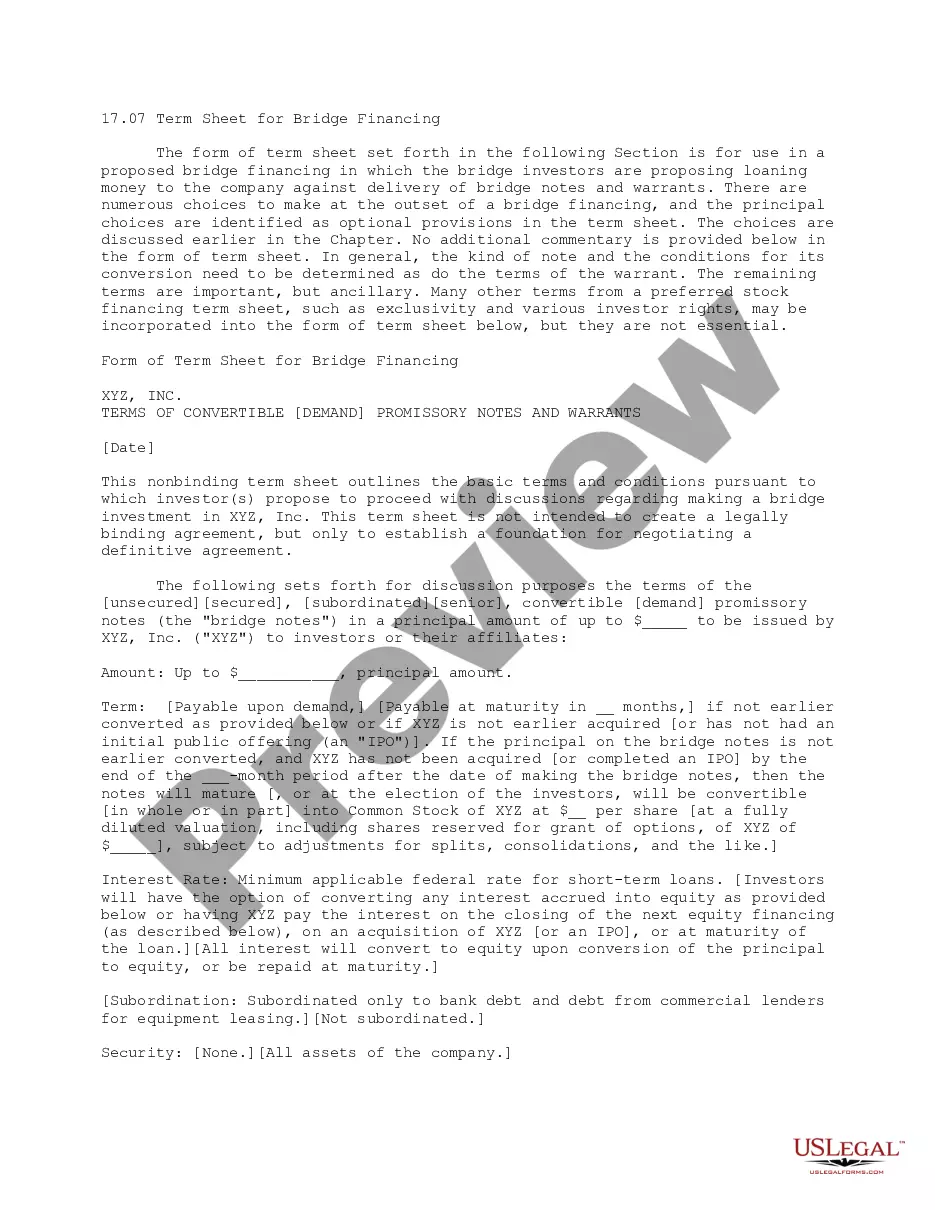

A term sheet is a nonbinding agreement that shows the basic terms and conditions of an investment. The term sheet serves as a template and basis for more detailed, legally binding documents.

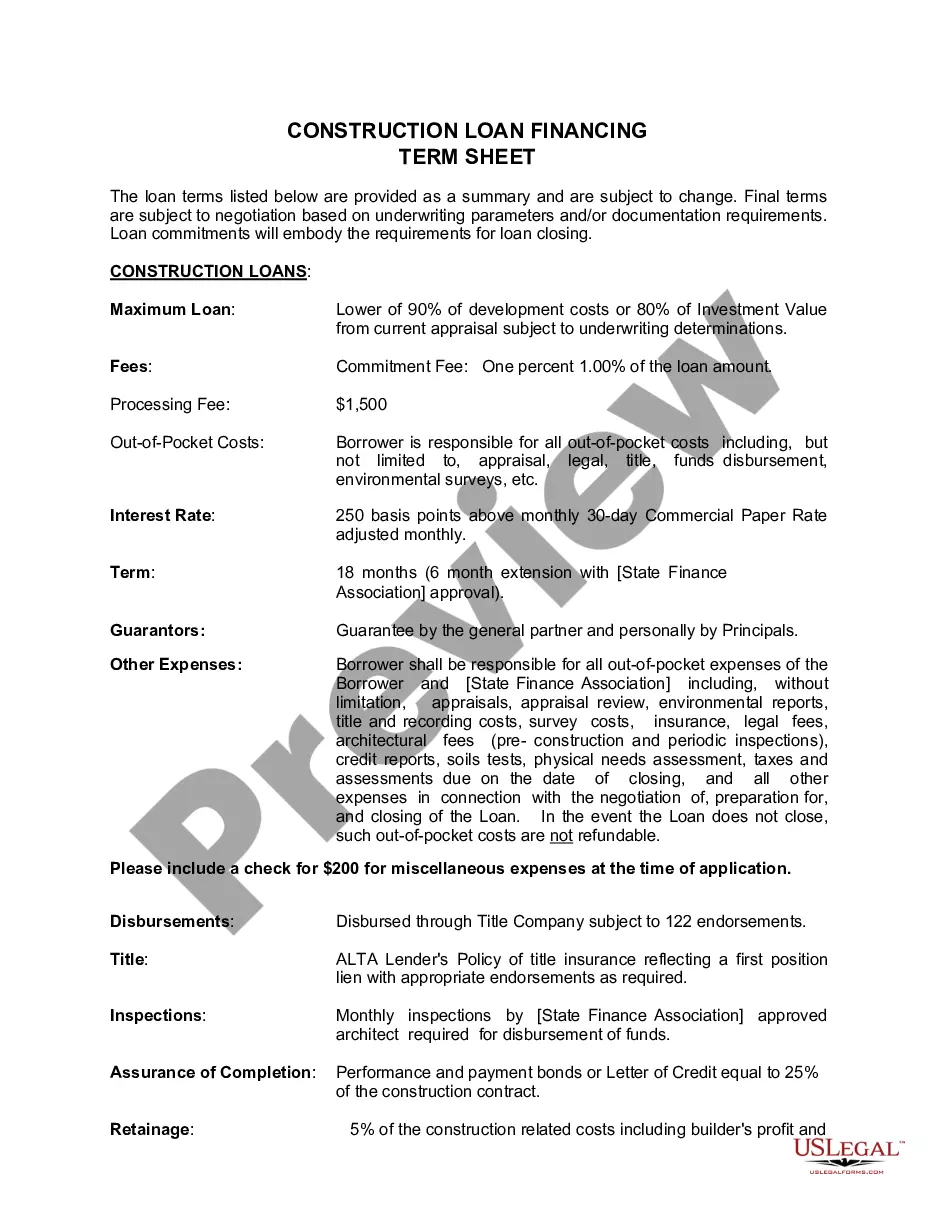

A construction loan is usually a short-term loan that provides funds to cover the cost of building or rehabilitating a home.

The period from borrowing money until the construction of the house is called pre-construction period. Pre-construction interest deduction is allowed for interest payments made from the date of borrowing till March 31st before the financial year in which the construction is completed.

After a construction loan is approved, your loan amount would be disbursed in stages as per the demand of each construction stage. The lender would inspect the site during the construction work or might ask a third-party technical team to visit and check the same.

Each release of money is called a draw. These smaller disbursements help to keep the project moving along ing to schedule. Most construction loans have a five- to seven-draw schedule, although some projects require more. For instance, the first draw may cover getting the necessary permits and preparing the land.

A mortgage is the homeowner's permanent financing plan once the home is completed. Most of us know this as the normal 15 year or 30 year-note mortgage while a construction loan is a temporary loan from the lender to fund the construction of a home.

In general, construction loans have higher interest rates than longer-term mortgage loans used to purchase homes. The money borrowed through a construction loan is typically provided in a series of advances as the construction progresses.

Cons The loan amount is set in advance, giving the borrower little flexibility in the event of unexpected costs. The entire balance of the loan is due at the end of the construction process. ... You'll pay higher interest rates on a construction loan compared to other loan options.

Construction loans are usually taken out by builders or a homebuyer custom-building their own home. They are short-term loans, usually for a period of only one year.

TERM LENGTH A 30-year loan may be the most common, but homebuyers have the option of selecting shorter terms depending on their bank, such as 20 or 15 years. A construction loan has a term of one year or less. The rates tend to be much higher, too.