New Hampshire Notice of Adverse Action - Non-Employment - Due to Consumer Investigative Report

Description

How to fill out Notice Of Adverse Action - Non-Employment - Due To Consumer Investigative Report?

Are you in a location where you need documents for both business or personal purposes almost every day.

There are many legal document templates accessible online, but locating reliable ones can be challenging.

US Legal Forms offers a vast array of form templates, such as the New Hampshire Notice of Adverse Action - Non-Employment - Due to Consumer Investigative Report, designed to comply with federal and state regulations.

Once you find the appropriate form, simply click Download now.

Choose the pricing plan you prefer, fill in the required details to create your account, and complete the purchase using your PayPal or credit card. Select a convenient file format and download your copy. Access all the document templates you have purchased in the My documents section. You can obtain another copy of the New Hampshire Notice of Adverse Action - Non-Employment - Due to Consumer Investigative Report anytime, if necessary. Just select the needed form to download or print the document template.

- If you are already familiar with the US Legal Forms website and have an account, simply Log In.

- Then, you can download the New Hampshire Notice of Adverse Action - Non-Employment - Due to Consumer Investigative Report template.

- If you do not have an account and wish to start using US Legal Forms, follow these steps.

- Locate the form you need and ensure it is for your correct city/state.

- Use the Preview button to review the document.

- Check the outline to confirm you have selected the right form.

- If the document is not what you were looking for, use the Search field to find the form that meets your needs.

Form popularity

FAQ

These credit reporting agencies give employers detailed information about your personal credit activity, including consumer debt and payment activity as well as adverse information, such as bankruptcies and late payments.

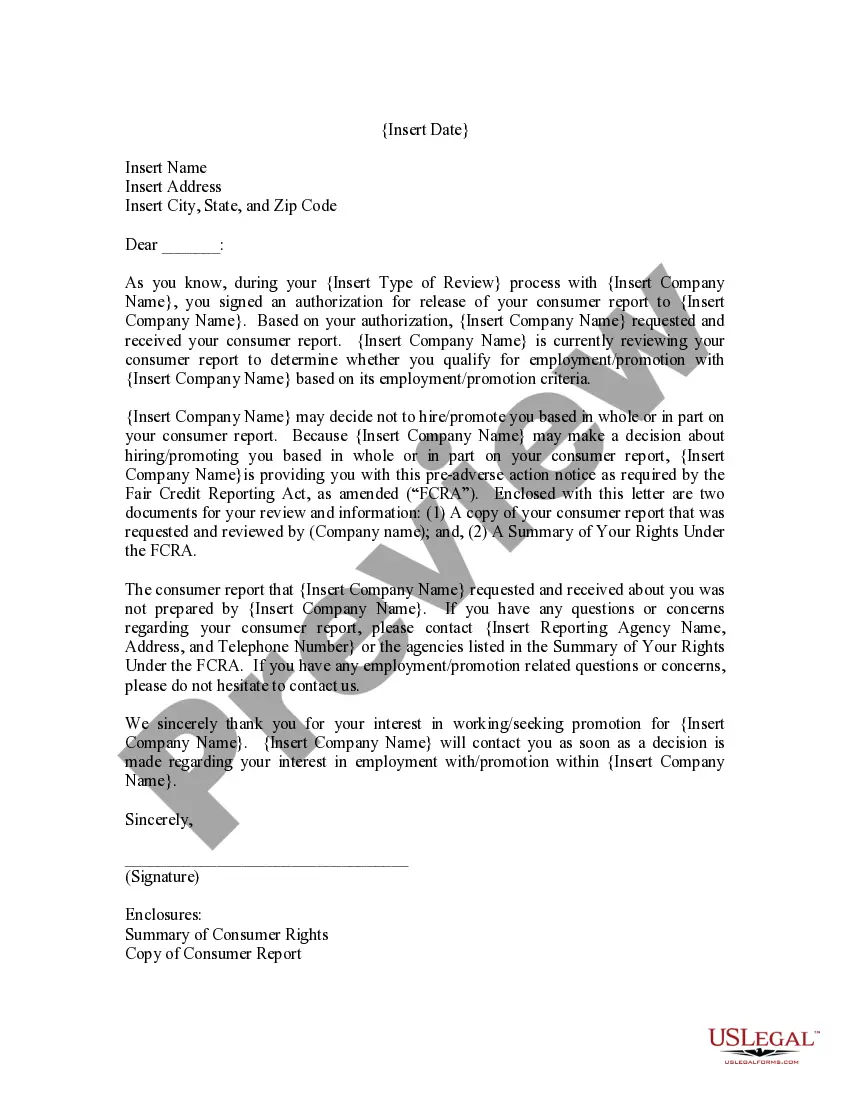

Anytime an employer requests a consumer report on an applicant or employee, obligations under the FCRA are triggered. Consumer reports can include a broad range of categories, including driving records, criminal records, credit reports, and other reports from third parties, such as drug tests.

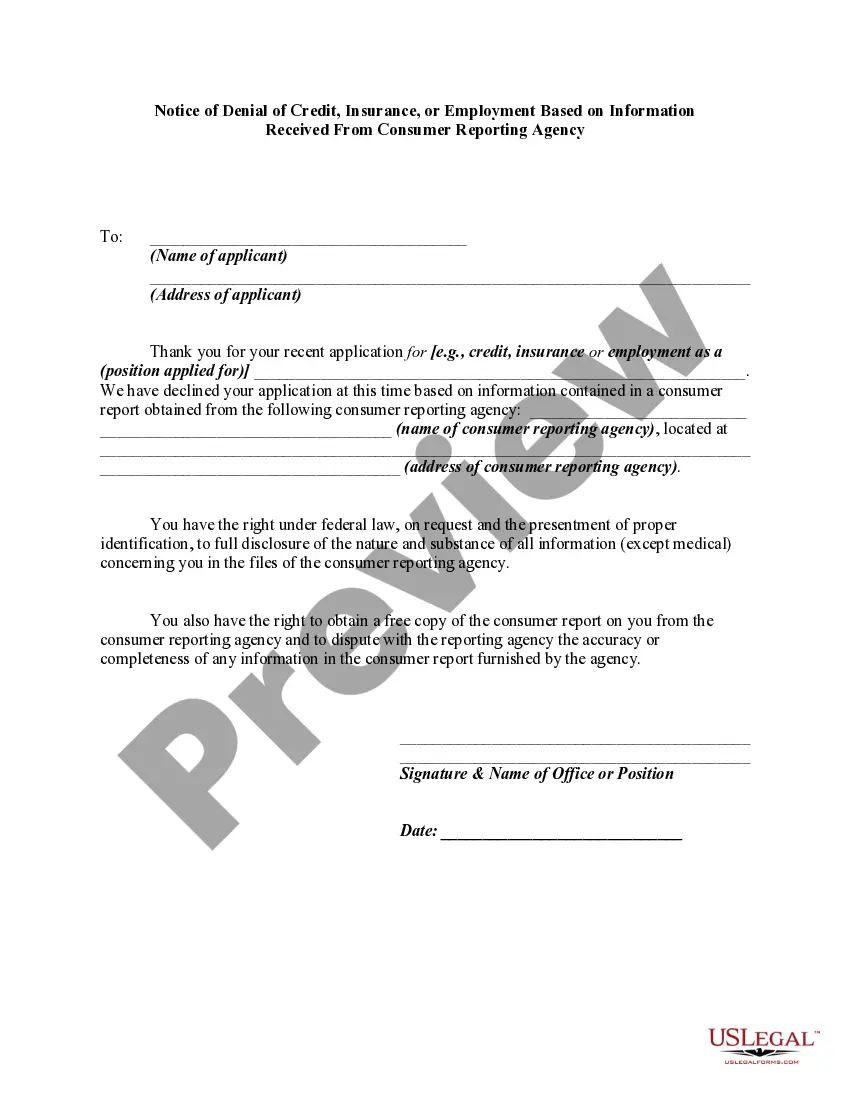

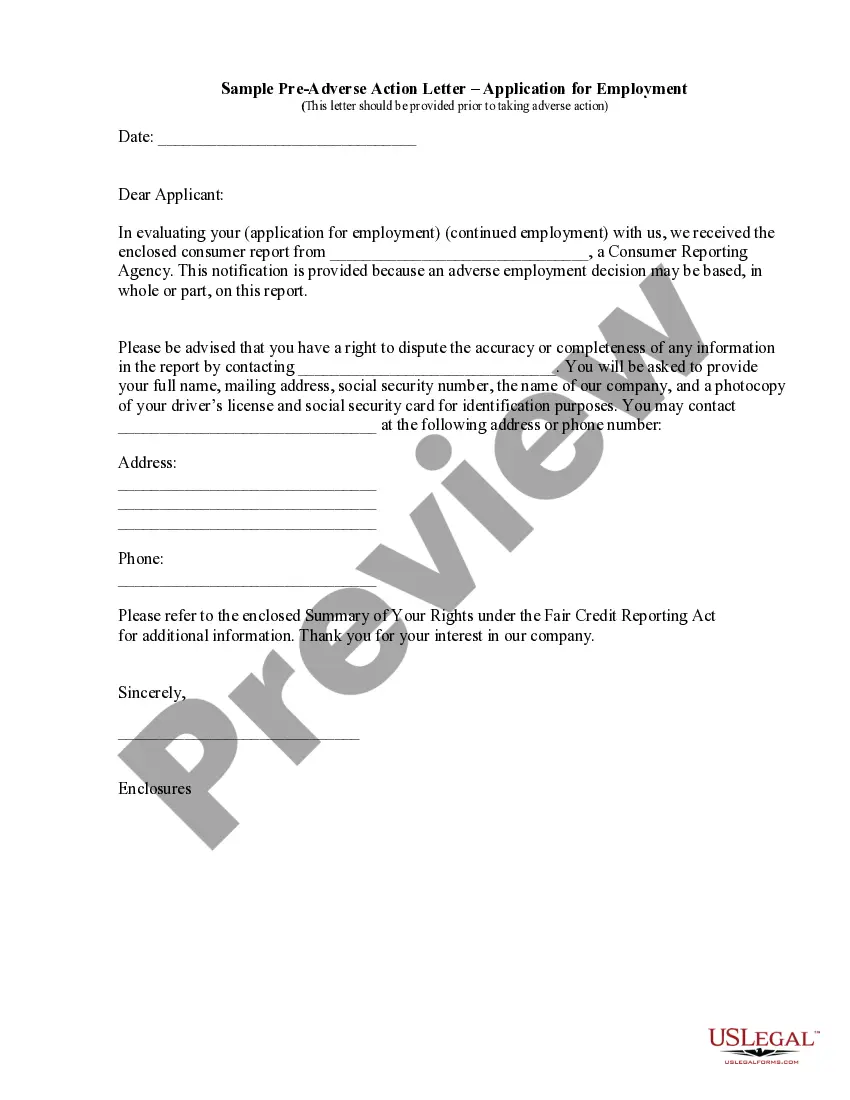

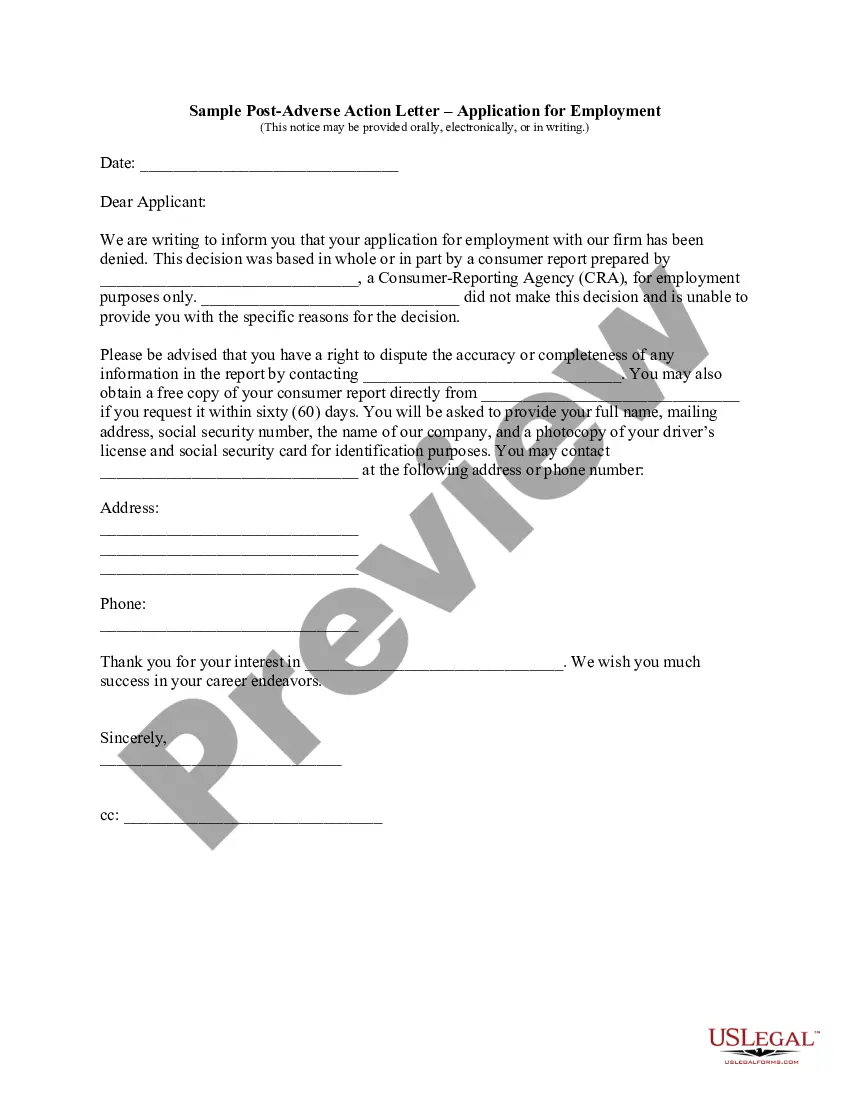

It must include information about the credit bureau used, an explanation of the specific reasons for the adverse action, a notice of the consumer's right to a free credit report and to dispute its accuracy and the consumer's credit score.

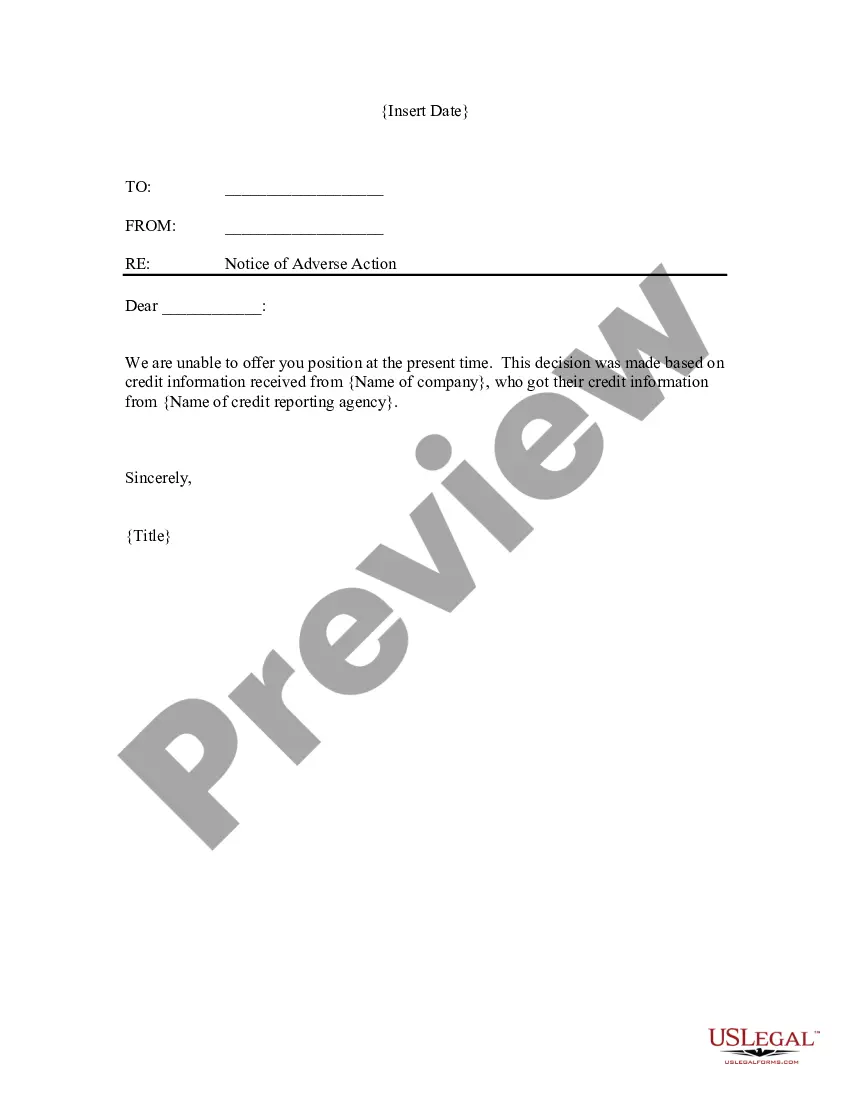

The following are examples of adverse actions employers might take: discharging the worker; demoting the worker; reprimanding the worker; committing harassment; creating a hostile work environment; laying the worker off; failing to hire or promote a worker; blacklisting the worker; transferring the worker to another

adverse action might also occur at pointofsale transactions where an account transaction is denied in real time. Notably, the ECOA does not consider an adverse action to have occurred where an action or forbearance on an account is taken in connection with inactivity, default, or delinquency as to that account.

Employers routinely obtain consumer reports that include the verification of the applicant/employee's Social Security number; current and previous residences; employment history, including all personnel files; education; references; credit history and reports; criminal history, including records from any criminal

A creditor must notify the applicant of adverse action within: 30 days after receiving a complete credit application. 30 days after receiving an incomplete credit application. 30 days after taking action on an existing credit account.

Adverse action is defined in the Equal Credit Opportunity Act and the FCRA to include: a denial or revocation of credit. a refusal to grant credit in the amount or terms requested. a negative change in account terms in connection with an unfavorable review of a consumer's account 5 U.S.C.

What is a Consumer Report? A consumer report contains information about your personal and credit characteristics, character, general reputation, and lifestyle. To be covered by the FCRA, a report must be prepared by a consumer reporting agency (CRA), a business that assembles such reports for other businesses.

If you're an organization that processes credit applications, it is your duty to provide an Adverse Action Notice if a consumer is denied credit. And you've got to provide it within 30 days of receiving a credit application.