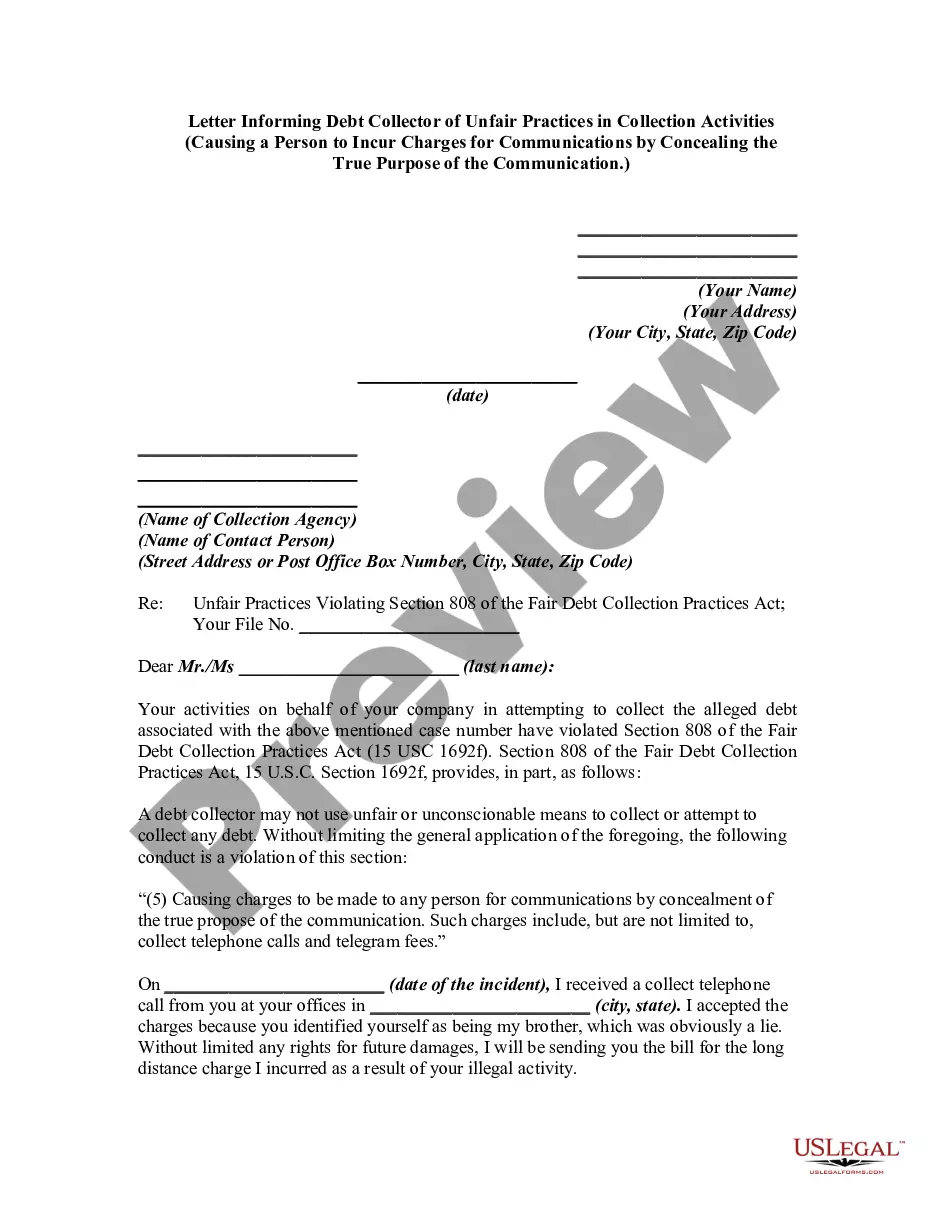

A debt collector may not use unfair or unconscionable means to collect a debt. This includes causing a person to incur charges for communications by concealing the true propose of the communication.

North Dakota Notice to Debt Collector - Causing a Consumer to Incur Charges for Communications by Concealing the Purpose of the Communication

Category:

State:

Multi-State

Control #:

US-DCPA-44

Format:

Word;

Rich Text

Instant download

Description

Use this form to notify a debt collector they violated the Fair Debt Collection Practices Act (FDCPA). Receiving notice from a consumer makes it more likely a debt collector will comply with the FDCPA. If they don't comply after receiving notice, your notice letter may help prove that their actions were intentional.

Free preview

How to fill out Notice To Debt Collector - Causing A Consumer To Incur Charges For Communications By Concealing The Purpose Of The Communication?

US Legal Forms - one of the largest collections of legal documents in the United States - offers a diverse selection of legal document templates that you can download or create.

By using the site, you can find thousands of forms for business and personal use, categorized by types, claims, or keywords. You can access the most recent versions of forms like the North Dakota Notice to Debt Collector - Causing a Consumer to Incur Charges for Communications by Concealing the Purpose of the Communication within seconds.

If you already have a membership, Log In and download the North Dakota Notice to Debt Collector - Causing a Consumer to Incur Charges for Communications by Concealing the Purpose of the Communication from your US Legal Forms library. The Download button will appear on each document you review. You have access to all previously downloaded forms from the My documents tab of your account.

Make modifications. Fill, edit, print, and sign the downloaded North Dakota Notice to Debt Collector - Causing a Consumer to Incur Charges for Communications by Concealing the Purpose of the Communication.

Every template you added to your account has no expiration date and is yours permanently. Therefore, if you wish to download or print another copy, just visit the My documents section and click on the form you want.

- If you want to utilize US Legal Forms for the first time, here are essential steps to get started.

- Ensure you have selected the correct form for your city/region. Click the Review button to examine the form's content. Read the form description to ensure you've chosen the right one.

- If the form does not suit your requirements, use the Search field at the top of the screen to find one that does.

- If you are satisfied with the form, confirm your choice by clicking the Get now button. Then, select your preferred pricing plan and provide your details to register for an account.

- Complete the transaction. Use a credit card or PayPal account to finalize the transaction.

- Choose the format and download the form to your device.

Form popularity

FAQ

The Fair Debt Collection Practices Act (FDCPA) (15 USC 1692 et seq.), which became effective in March 1978, was designed to eliminate abusive, deceptive, and unfair debt collection practices.

The California statute is called the Rosenthal Fair Debt Collection Practices Act. Creditors and debt collection agencies are permitted to take reasonable steps to enforce and collect payment of debts. That is because an efficient and productive economy requires a credit process.

7 Most Common FDCPA ViolationsContinued attempts to collect debt not owed.Illegal or unethical communication tactics.Disclosure verification of debt.Taking or threatening illegal action.False statements or false representation.Improper contact or sharing of info.Excessive phone calls.

Fortunately, there are legal actions you can take to stop this harassment:Write a Letter Requesting To Cease Communications.Document All Contact and Harassment.File a Complaint With the FTC.File a Complaint With Your State's Agency.Consider Suing the Debt Collection Agency for Harassment.

A debt collector may not communicate with a consumer at any unusual time (generally before a.m. or after p.m. in the consumer's time zone) or at any place that is inconvenient to the consumer, unless the consumer or a court of competent jurisdiction has given permission for such contacts.

The Fair Credit Reporting Act is a federal law that regulates the collection and reporting of credit information from consumers. The law governs how a consumer's credit information is collected and shared with others.

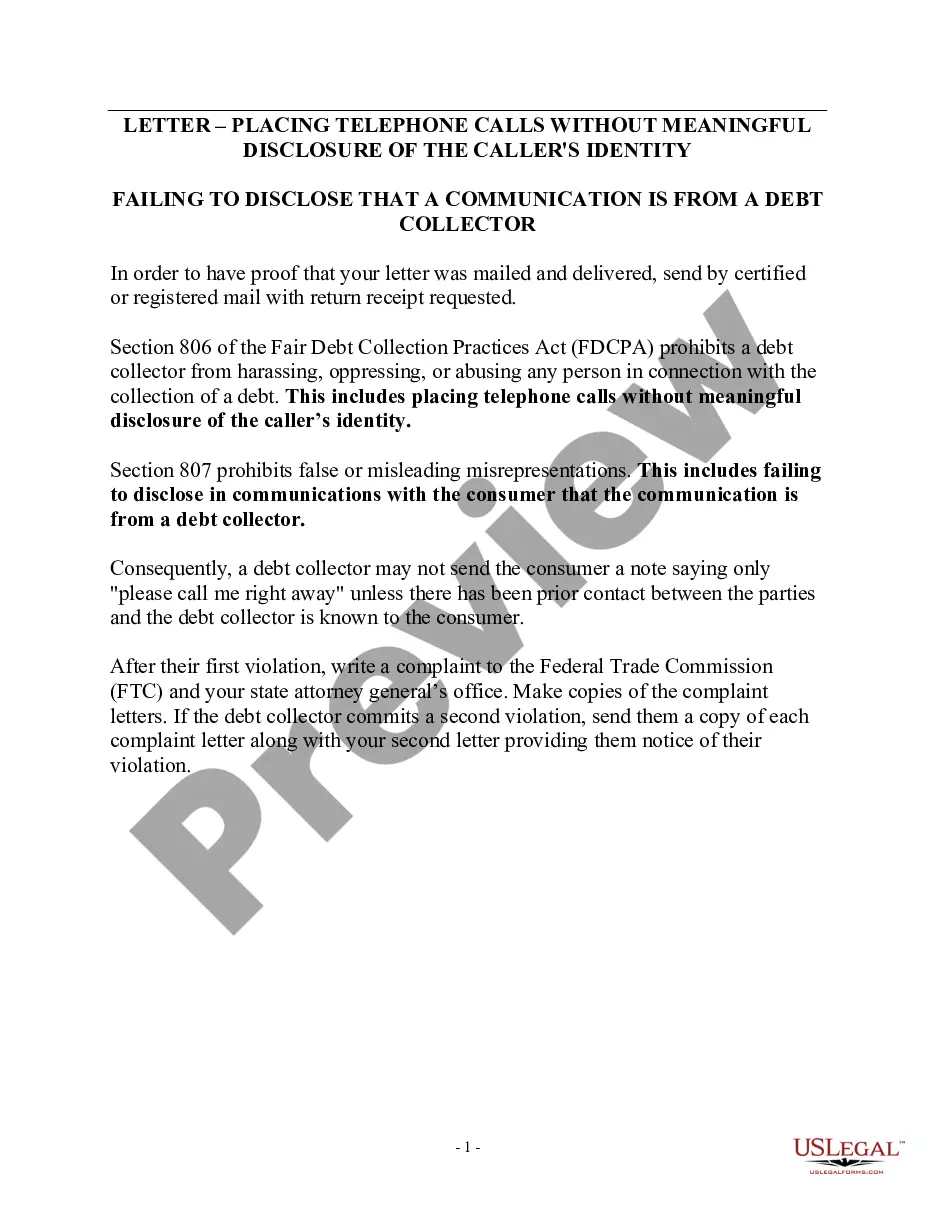

The Fair Debt Collection Practices Act (FDCPA) is the main federal law that governs debt collection practices. The FDCPA prohibits debt collection companies from using abusive, unfair or deceptive practices to collect debts from you.

Deceptive And Unfair Practices Calling you collect so that you have to pay to accept the call is an example of an unfair practice. Engaging in any practice that forces you to pay additional money other than the debt you owe is considered an FDCPA violation.

The Fair Debt Collection Practices Act makes it illegal for debt collectors to harass or threaten you when trying to collect on a debt. In addition, on November 30, 2021, the CFPB's new Debt Collection Rule became effective.

If a debt collector violates the FDCPA, you may sue that collector in state or federal court. You can even sue in small claims court. You must do this within one year from the date on which the violation occurred.