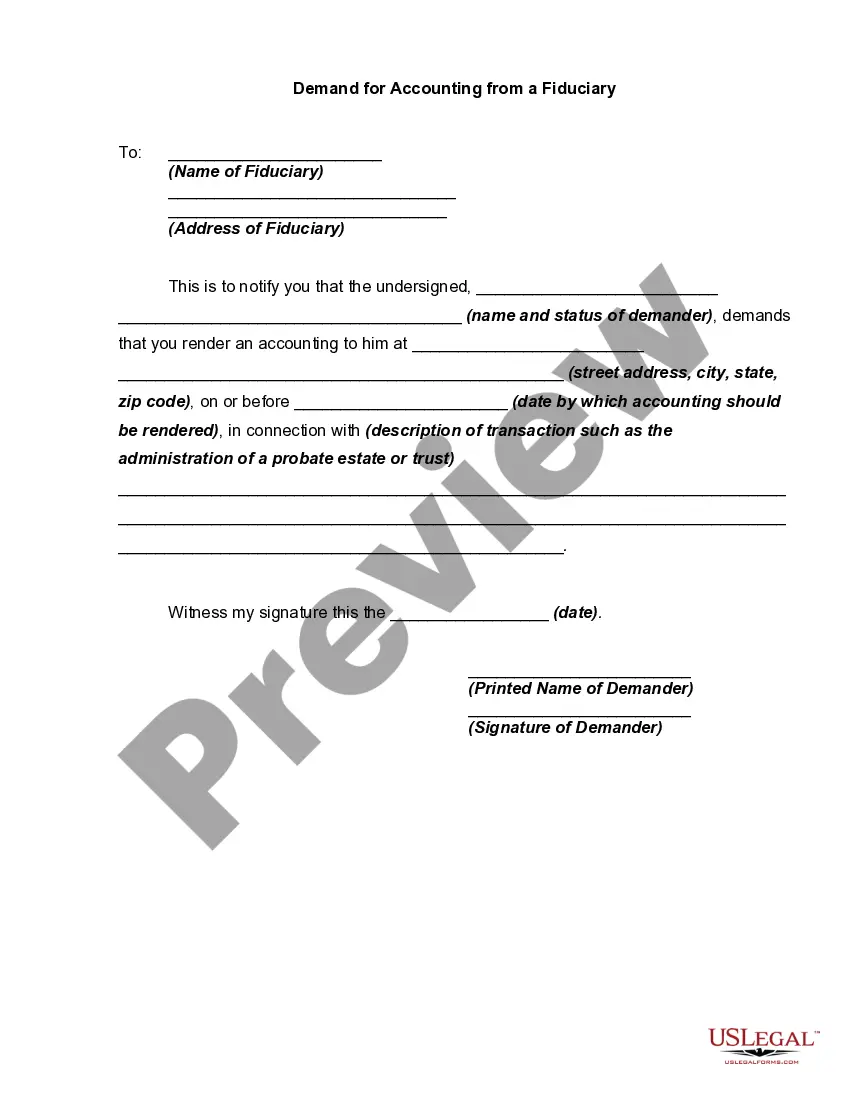

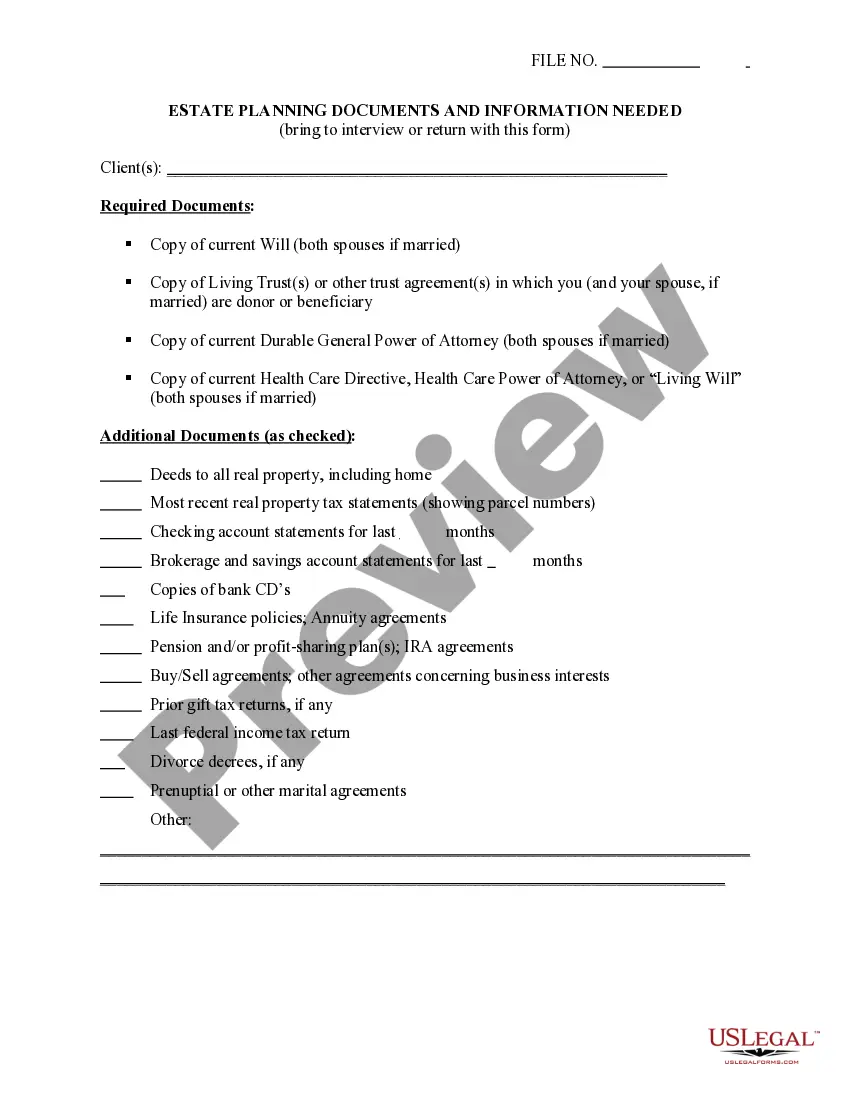

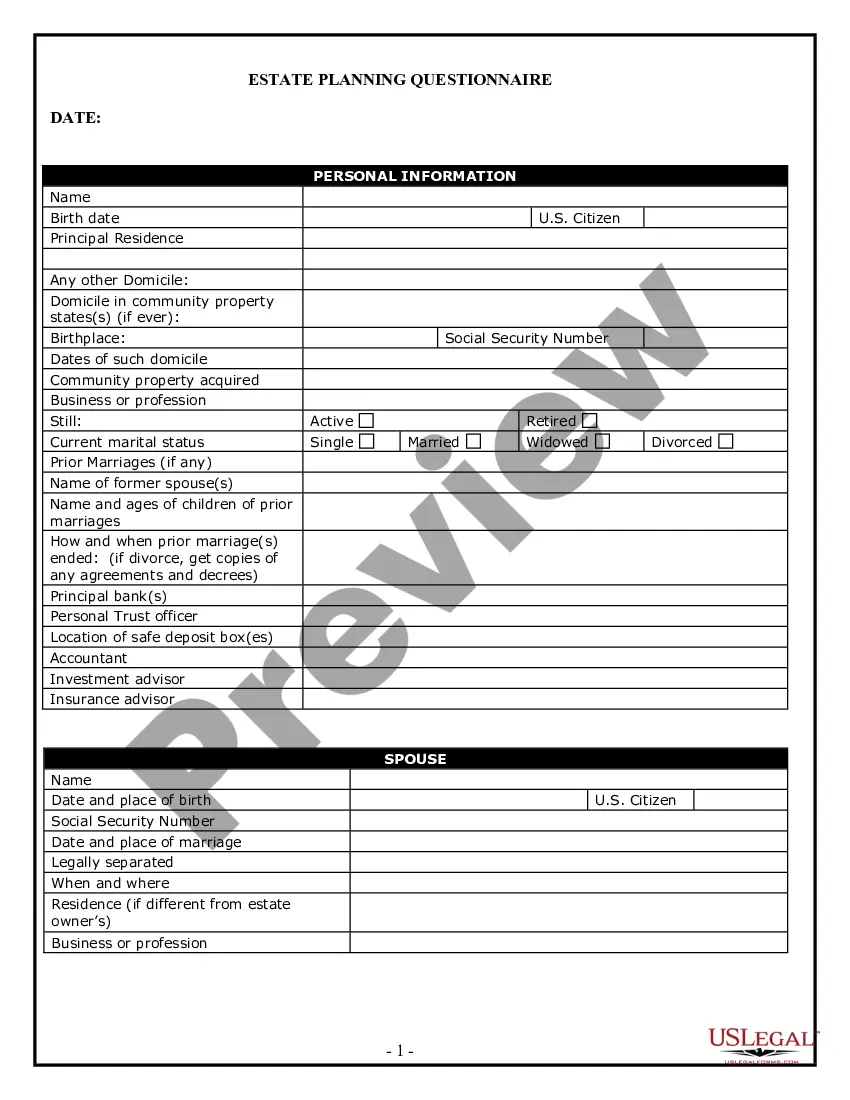

An accounting by a fiduciary usually involves an inventory of assets, debts, income, expenditures, and other items, which is submitted to a court. Such an accounting is used in various contexts, such as administration of a trust, estate, guardianship or conservatorship. Generally, a prior demand by an appropriate party for an accounting, and a refusal by the fiduciary to account, are conditions precedent to the bringing of an action for an accounting.

North Dakota Demand for Accounting from a Fiduciary such as an Executor, Conservator, Trustee or Legal Guardian

Instant download

Description

How to fill out Demand For Accounting From A Fiduciary Such As An Executor, Conservator, Trustee Or Legal Guardian?

If you desire to total, obtain, or create legal document templates, utilize US Legal Forms, the largest selection of legal forms, which can be accessed online.

Employ the site's straightforward and handy search feature to find the documents you require.

Various templates for commercial and personal reasons are categorized by type and jurisdiction, or keywords.

Step 5. Process the payment. You can use your credit card or PayPal account to complete the transaction.

Step 6. Select the format of the legal form and download it to your device. Step 7. Complete, edit, and print or sign the North Dakota Demand for Accounting from a Fiduciary such as an Executor, Conservator, Trustee, or Legal Guardian.

Every legal document template you acquire is yours permanently. You will have access to every form you saved in your account. Go to the My documents section and select a form to print or download again.

Complete and download, and print the North Dakota Demand for Accounting from a Fiduciary such as an Executor, Conservator, Trustee, or Legal Guardian through US Legal Forms. There are numerous professional and jurisdiction-specific forms you can employ for your business or personal requirements.

- Use US Legal Forms to retrieve the North Dakota Demand for Accounting from a Fiduciary like an Executor, Conservator, Trustee, or Legal Guardian within just a few clicks.

- If you are already a US Legal Forms subscriber, Log In to your account and select the Download option to receive the North Dakota Demand for Accounting from a Fiduciary such as an Executor, Conservator, Trustee, or Legal Guardian.

- Additionally, you can access forms you previously saved in the My documents section of your account.

- If you are utilizing US Legal Forms for the first time, adhere to the steps outlined below.

- Step 1. Verify that you have selected the form for the appropriate city/state.

- Step 2. Utilize the Preview feature to review the form's content. Remember to check the details.

- Step 3. If you are not satisfied with the form, use the Search bar at the top of the screen to find alternative versions of the legal form template.

- Step 4. Once you have found the necessary form, click on the Purchase now button. Choose the pricing plan you prefer and enter your information to sign up for the account.

Form popularity

FAQ

One major disadvantage of a conservatorship is the potential for loss of autonomy for the individual under care. Moreover, the process can be costly and time-consuming, often requiring ongoing court supervision. Understanding these factors is crucial when considering a North Dakota Demand for Accounting from a Fiduciary such as an Executor, Conservator, Trustee or Legal Guardian.

To file for a conservatorship in West Virginia, you must submit a petition to the court that outlines the need for a conservator. This process involves providing evidence of the individual's incapacity and may require medical reports. For assistance, consider using resources like uslegalforms, which can simplify navigating the North Dakota Demand for Accounting from a Fiduciary such as an Executor, Conservator, Trustee or Legal Guardian.

The primary purpose of a conservator is to protect and manage the financial and personal affairs of individuals who are incapable of doing so themselves. This includes making decisions about their health care, finances, and daily living circumstances. Knowing the role of a conservator can guide families in addressing a North Dakota Demand for Accounting from a Fiduciary such as an Executor, Conservator, Trustee or Legal Guardian.

An executor of a will has the responsibility to manage the estate and distribute assets according to the deceased's wishes. However, they cannot simply take everything for personal gain. The executor must follow legal guidelines and adhere to the North Dakota Demand for Accounting from a Fiduciary such as an Executor, Conservator, Trustee or Legal Guardian, ensuring all actions are fair and transparent.

Conservators and executors serve different roles in managing an estate. An executor administers a deceased person's estate according to the will, while a conservator manages the affairs of someone who cannot do so due to incapacity. Understanding these distinctions is important, especially when dealing with a North Dakota Demand for Accounting from a Fiduciary such as an Executor, Conservator, Trustee or Legal Guardian.

A trustee has a legal obligation to provide regular and accurate accounting to beneficiaries, detailing all transactions related to the trust’s assets. This duty ensures that beneficiaries are informed about the management and financial status of the trust. Failure to provide appropriate accounting can lead to a North Dakota Demand for Accounting from a Fiduciary such as an Executor, Conservator, Trustee or Legal Guardian. Utilizing platforms like uslegalforms can empower you with the appropriate forms and resources to address accounting concerns effectively.

Generally, a trustee must provide accounting to beneficiaries about how trust assets are managed. However, there may be specific situations where a trustee might not fulfill this obligation, possibly leading to a North Dakota Demand for Accounting from a Fiduciary such as an Executor, Conservator, Trustee or Legal Guardian. It is crucial for beneficiaries to know their rights to ensure transparency and proper management of the trust. Accessing proper legal resources can assist in addressing these accounting requirements effectively.

A trustee is a specific type of fiduciary who manages assets in a trust for the benefit of others. While all trustees are fiduciaries, not all fiduciaries are trustees. Fiduciaries can include executors, conservators, and legal guardians, each responsible for acting in the best interest of the individuals they serve. Understanding the distinction is important, especially in the context of a North Dakota Demand for Accounting from a Fiduciary such as an Executor, Conservator, Trustee or Legal Guardian.

A conservator and an executor serve different functions in the legal system. A conservator manages the affairs of someone who cannot do so themselves, while an executor handles the distribution of a deceased person's estate. Both roles require a clear understanding of North Dakota demand for accounting from a fiduciary, ensuring responsible management and oversight of assets. Clarifying these distinctions is essential for effective estate planning and management.

A conservator account generally does not include a beneficiary in the way other accounts do. The conservator manages the funds for the benefit of the conservatee, and upon the conservatee's passing, any remaining assets may become part of their estate. This detail underscores the need for strict adherence to North Dakota demand for accounting from a fiduciary to ensure correct asset management.