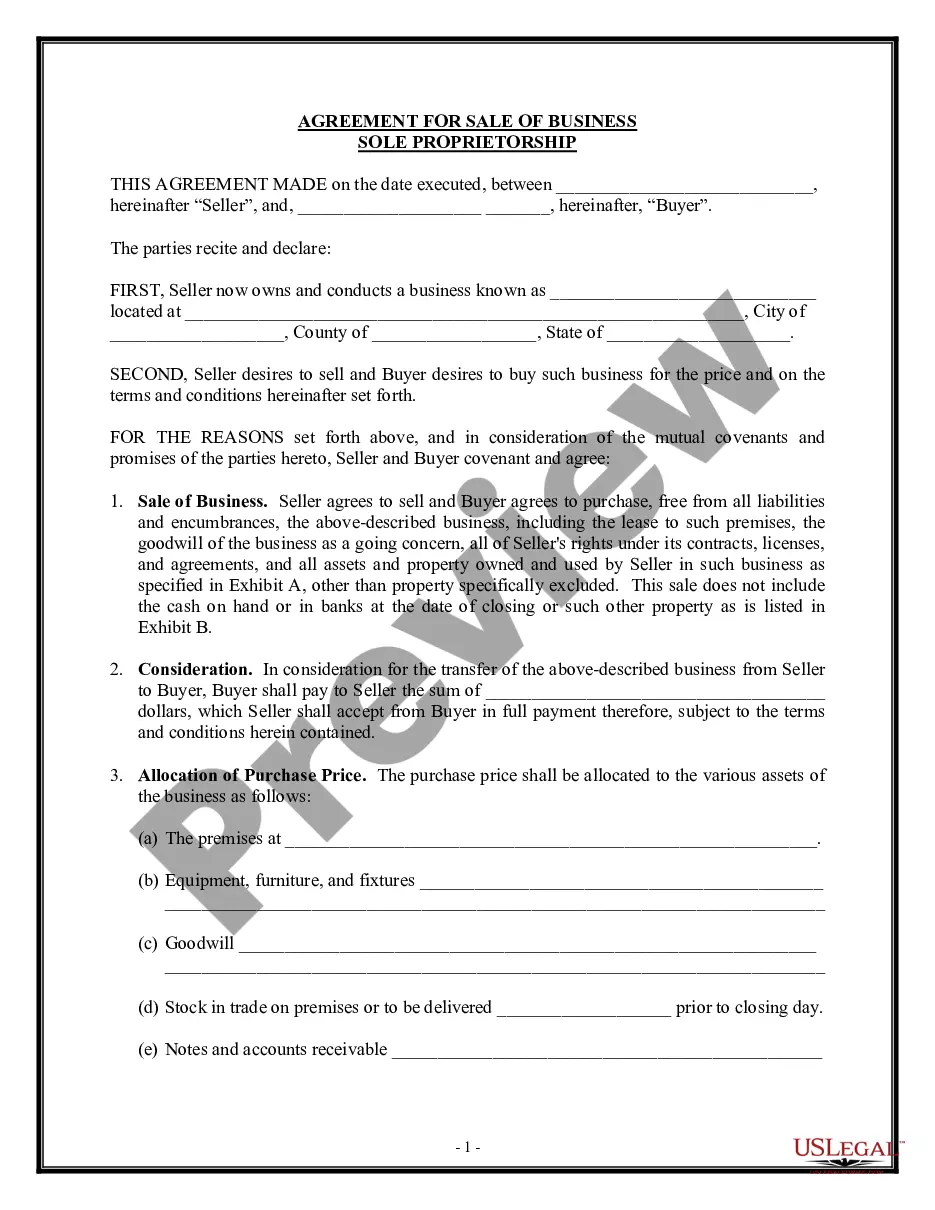

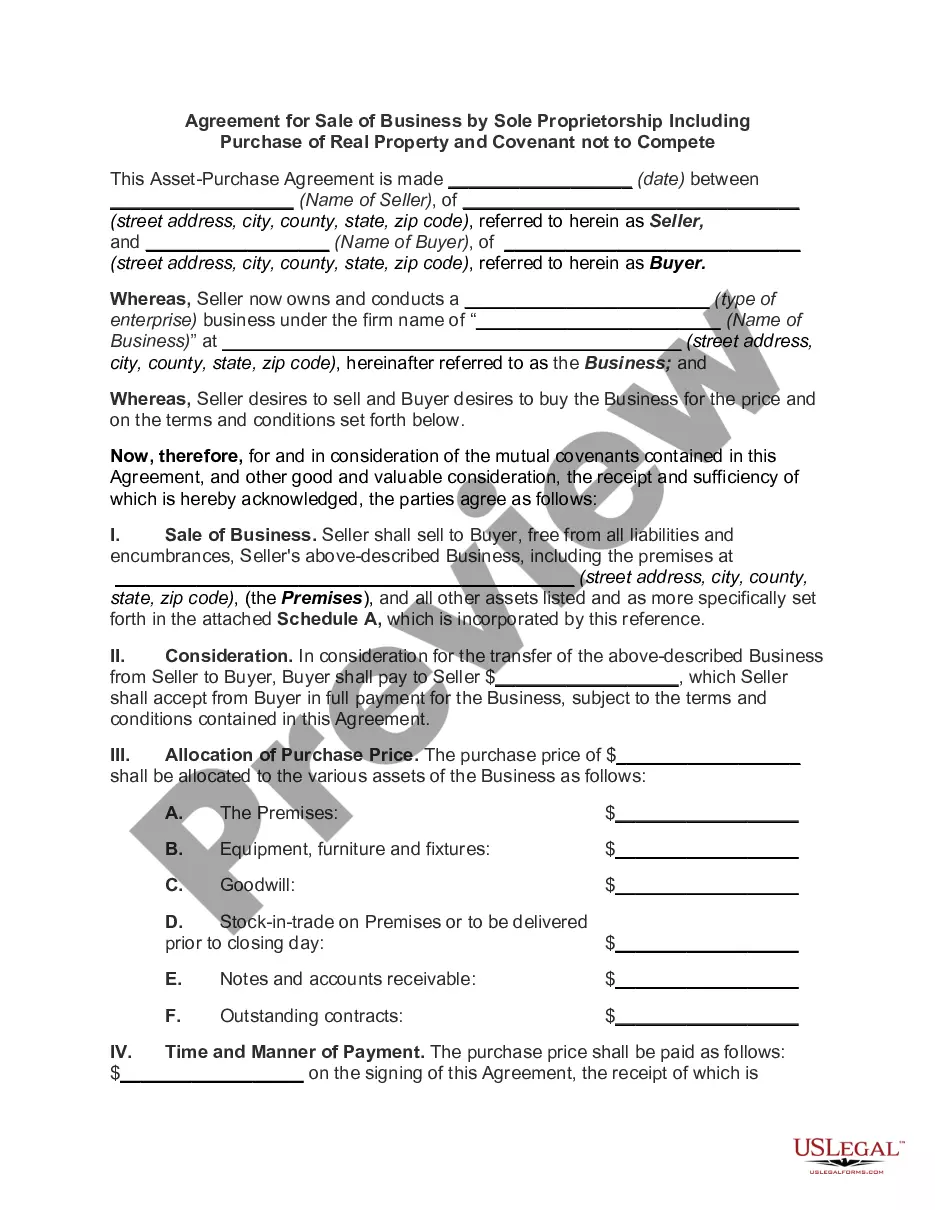

North Dakota Agreement for Sale of Business by Sole Proprietorship with Purchase Price Contingent on Audit

Description

How to fill out Agreement For Sale Of Business By Sole Proprietorship With Purchase Price Contingent On Audit?

Are you currently in a scenario where you need documents for either business or particular purposes almost every day.

There are numerous legal document templates available online, but finding reliable ones is not easy.

US Legal Forms offers a wide array of document templates, including the North Dakota Agreement for Sale of Business by Sole Proprietorship with Purchase Price Contingent on Audit, which are designed to comply with state and federal regulations.

- If you are already familiar with the US Legal Forms website and have an account, simply Log In.

- After that, you can download the North Dakota Agreement for Sale of Business by Sole Proprietorship with Purchase Price Contingent on Audit template.

- If you do not have an account and wish to start using US Legal Forms, follow these steps.

- Find the template you want and make sure it is for the correct city/state.

- Utilize the Review button to examine the form.

- Check the summary to ensure that you have selected the correct template.

- If the template is not what you're looking for, use the Search field to find the document that suits your needs.

- Once you locate the right template, click on Purchase now.

- Select the pricing plan you prefer, fill in the required information to create your account, and complete your purchase using PayPal or a credit card.

- Choose a suitable file format and download your version.

- Access all the document templates you have purchased in the My documents section. You can obtain an additional copy of North Dakota Agreement for Sale of Business by Sole Proprietorship with Purchase Price Contingent on Audit at any time if needed. Click the relevant template to download or print the document.

- Use US Legal Forms, the largest collection of legal forms, to save time and avoid mistakes.

- The service offers professionally drafted legal documents that you can use for various purposes.

- Create an account on US Legal Forms and start making your life a little easier.

Form popularity

FAQ

Legally, there are very few requirements when creating or selling a sole proprietorship. A sole proprietorship was designed to have only one owner. Therefore, when the owner dies or the business is sold, the structure automatically dissolves. A sole proprietorship cannot be transferred to another party.

A sole proprietorship is the simplest and most common structure chosen to start a business. It is an unincorporated business owned and run by one individual with no distinction between the business and you, the owner.

When a sole proprietor dies, all of his assets and liabilities become part of his estate, including the assets and liabilities generated from the business activity. Through a will, the owner can leave assets to a particular individual that allow him to continue operating the business.

With a sole proprietorship, that's not so easy. Legally, you and your sole proprietorship are one and the same: When you die, your business dies with you. By selling your business ahead of your death or transferring the assets in your will, you can keep it going.

What happens when a sole proprietor dies? - Since a sole proprietorship has no legal identity apart from its owner, the death of a sole proprietor terminates the business. You just studied 29 terms!

The owner of a sole proprietorship typically signs contracts in his or her own name, because the sole proprietorship has no separate identity under the law. The sole proprietor owner will typically have customers write checks in the owner's name, even if the business uses a fictitious name.

A sole proprietorshipalso referred to as a sole trader or a proprietorshipis an unincorporated business that has just one owner who pays personal income tax on profits earned from the business. A sole proprietorship is the easiest type of business to establish or take apart, due to a lack of government regulation.

As there is no separate entity under the law for a sole proprietorship business, contracts are normally signed by owner under his or her personal name. Even if the business uses a fictitious name, the owner will usually have his or her name written down in the checks issued by the clients.

In a sole proprietorship, when the business owner dies, the business is essentially concluded and all assets and debts pass through his estate. The sole proprietor's will can pass the business onto a certain beneficiary, but that creates a new sole proprietorship (or partnership if more than two beneficiaries).

The successor or legal heir has to first submit the death certificate of the sole proprietor and the succession certificate to the jurisdictional GST officer as documentary evidence. The proper officer will then add the successor as the authorised signatory for the deceased sole proprietor.