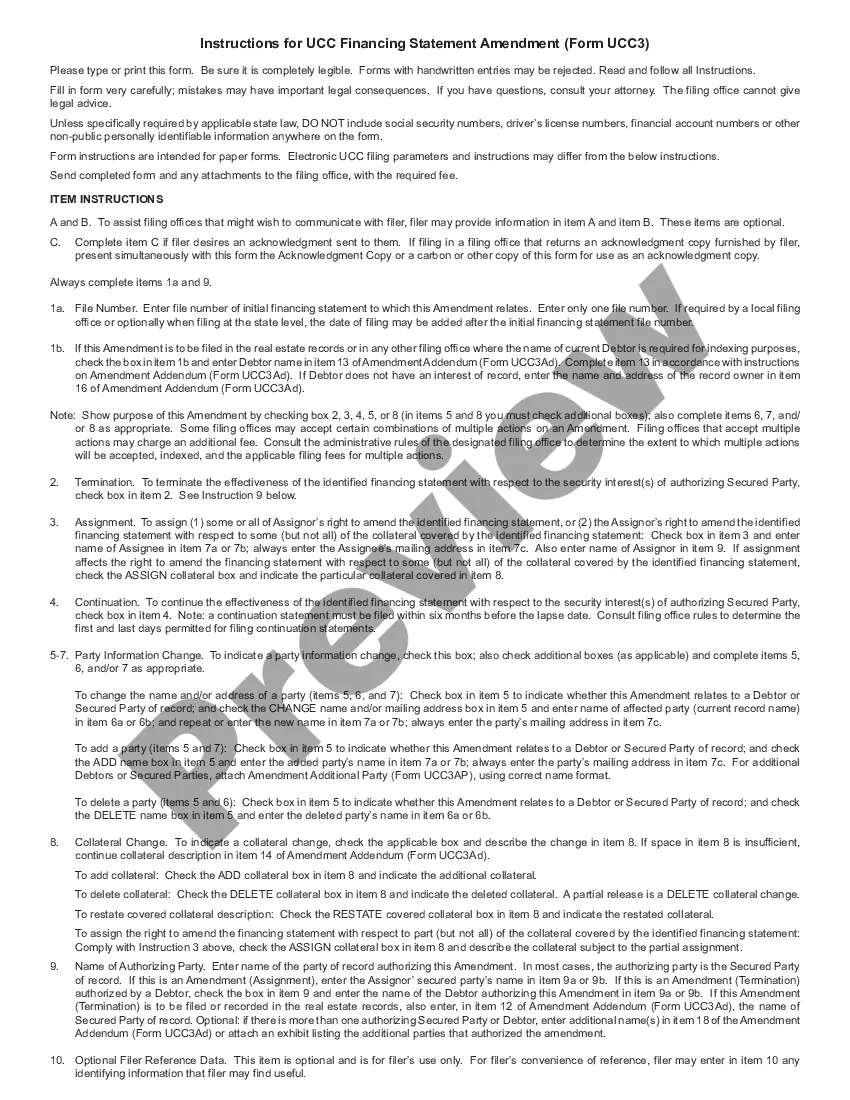

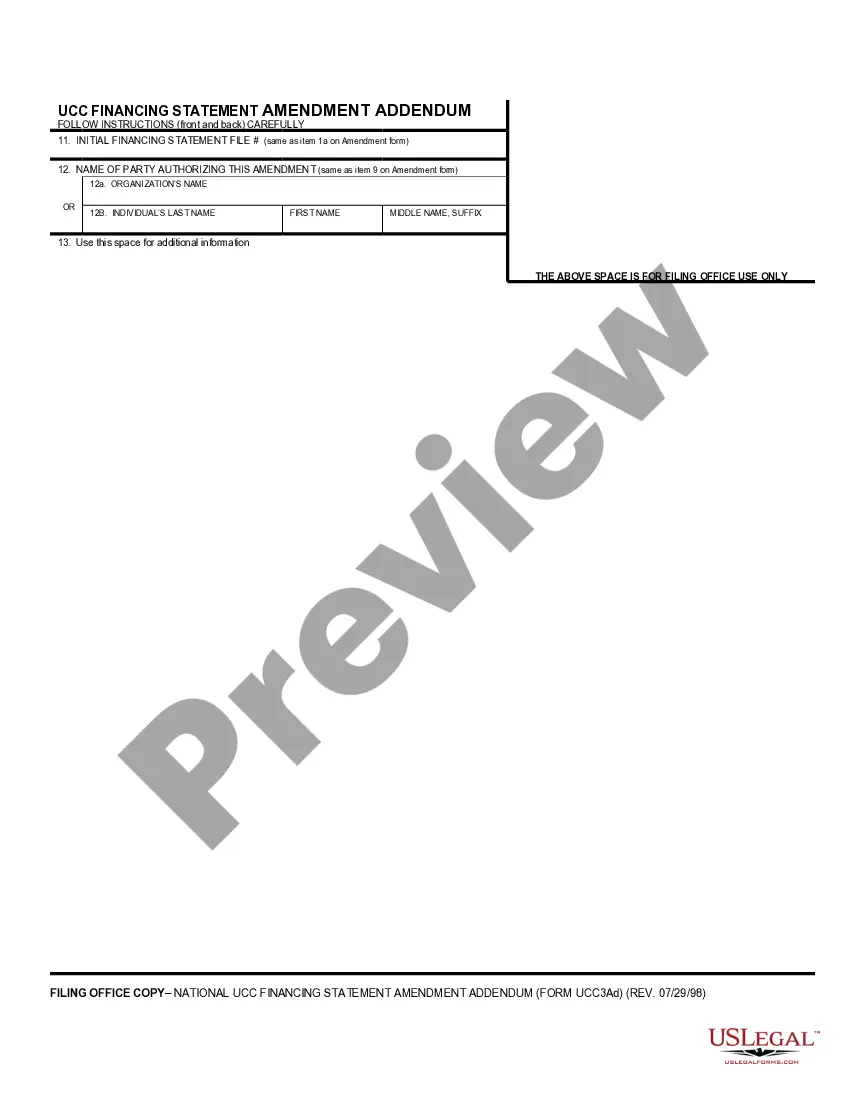

North Carolina UCC3 Financing Statement Amendment Addendum

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out North Carolina UCC3 Financing Statement Amendment Addendum?

Steer clear of expensive lawyers and discover the North Carolina UCC3 Financing Statement Amendment Addendum you require at an affordable cost on the US Legal Forms website.

Utilize our straightforward groups function to search for and acquire legal and tax documents. Review their descriptions and preview them before downloading.

Make payment via card or PayPal. Opt to receive the form in PDF or DOCX. Click Download and locate your form in the My documents section. Feel free to store the form on your device or print it out. After downloading, you can complete the North Carolina UCC3 Financing Statement Amendment Addendum by hand or using an editing software. Print it and reuse the template multiple times. Accomplish more for less with US Legal Forms!

- Additionally, US Legal Forms offers clients comprehensive guidelines on how to download and complete each template.

- US Legal Forms members simply need to Log In and download the particular document they require to their My documents section.

- Individuals who have not subscribed yet should adhere to the instructions outlined below.

- Confirm the North Carolina UCC3 Financing Statement Amendment Addendum is suitable for use in your state.

- If accessible, examine the description and utilize the Preview option prior to downloading the sample.

- If you are assured the template is appropriate for you, click Buy Now.

- If the template is inaccurate, employ the search tool to find the correct one.

- Subsequently, create your account and choose a subscription plan.

Form popularity

FAQ

When the debtor has satisfied all amounts owed to the lender, a UCC-3 termination statement (now called a UCC termination statement) is routinely filed to terminate the security interest perfected by the UCC-1 financing statement.

A UCC-3 termination statement (a Termination) is a required filing that terminates a security interest that has been perfected by a UCC-1 filing. 1. A Termination for personal property is accomplished by completing and filing form UCC-3 with the Secretary of State's office in the appropriate state.

When the debtor has satisfied all amounts owed to the lender, a UCC-3 termination statement (now called a UCC termination statement) is routinely filed to terminate the security interest perfected by the UCC-1 financing statement.

Rules vary by State around releasing a UCC lien after a borrower satisfied the debt. Primarily there are two main ways to remove them. One way is by having the lender file a UCC-3 Financing Statement Amendment. Another way to remove a UCC filing is by swearing an oath of full payment at the secretary of state office.

Also known as a UCC-3, and, depending on the context, a UCC-3 financing statement amendment, a UCC-3 termination statement, and a UCC-3 continuation statement. Under the Uniform Commercial Code, a UCC-3 is used to continue, assign, terminate, or amend an existing UCC-1 financing statement (UCC-1).

After receiving your request, the lender has 20 days to terminate the UCC filing.

A UCC1 financing statement is effective for a period of five years. A record that is not continued before its lapse date will cease to be effective, costing the secured party their perfected status and perhaps their priority position to collect. Once a financing statement has lapsed, it cannot be revived.

The secured party has 20 days to either terminate the filing or send a termination statement to the debtor that the debtor can then file. If this does not happen within the 20-day time frame, the debtor may file a UCC-3 termination statement.