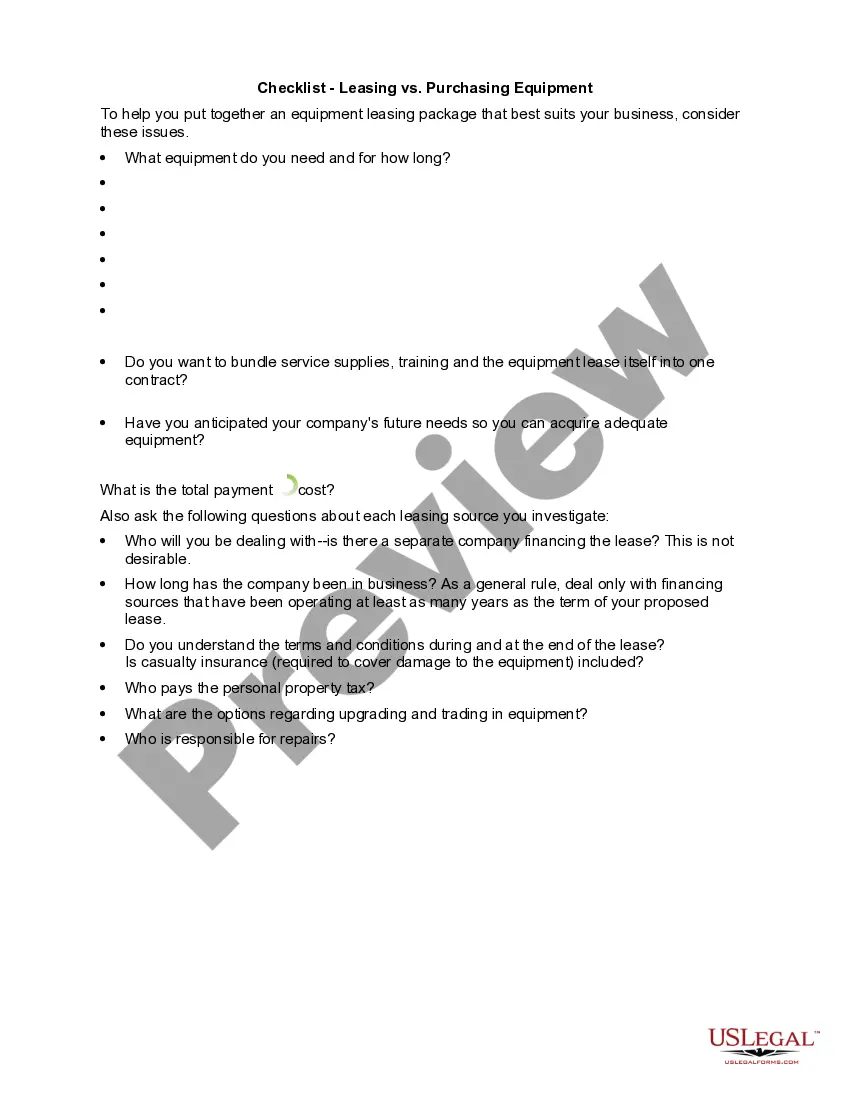

North Carolina Checklist - Leasing vs. Purchasing

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Checklist - Leasing Vs. Purchasing?

US Legal Forms - one of the most prominent collections of legal documents in the United States - provides a range of legal document templates that you can download or print.

By using the website, you can access thousands of forms for business and personal applications, sorted by categories, states, or keywords. You can find the latest types of forms such as the North Carolina Checklist - Leasing vs. Purchasing in moments.

If you have a membership, Log In and download the North Carolina Checklist - Leasing vs. Purchasing from your US Legal Forms library. The Download button will appear on every form you view. You can access all previously downloaded forms in the My documents section of your account.

Complete the transaction. Use a credit card or PayPal account to finalize the purchase.

Select the format and download the form to your device. Edit. Fill, modify, print, and sign the downloaded North Carolina Checklist - Leasing vs. Purchasing. Every template you add to your account does not have an expiration date and belongs to you permanently. Therefore, if you want to download or print another copy, just navigate to the My documents section and click on the form you need. Access the North Carolina Checklist - Leasing vs. Purchasing through US Legal Forms, one of the largest collections of legal document templates. Utilize a vast array of professional and state-specific templates that fulfill your business or personal requirements.

- If you want to use US Legal Forms for the first time, here are simple steps to get started.

- Ensure you have selected the correct form for your city/state.

- Click on the Review button to examine the contents of the form.

- Check the form description to confirm you have selected the correct form.

- If the form does not meet your needs, use the Search field at the top of the screen to find one that does.

- If you are satisfied with the form, confirm your selection by clicking the Get now button.

- Next, choose the pricing plan you prefer and provide your details to register for an account.

Form popularity

FAQ

A lease amount is determined by the difference between a vehicle's selling price and its residual value. Here's how that works: Consider two $30,000 vehicles: One has a residual value of 65 percent after 36 months, and the other has a 40 percent residual for that period.

Usually long term it's cheaper to buy an asset than lease it. Remember you won't be able to claim the entire amount paid as a business expense the value of asset is depreciated over several years. Buy if: The asset plays an integral role in your overall business success and you use it all the time.

A lease analysis uses various tools and methods to calculate and interpret financial data to determine its benefits for the lessee (renter) or the lessor (who receives payment). The income approach to value is an approach of appraisal where the value is determined by the income that is produced by the property.

The term buying refers to purchasing the asset by paying the price for it. Leasing is an arrangement wherein the owner of the asset permits another person to use the asset, for recurring payments.

This is calculated as:+ Total up front costs (down payment + other fees)+ Lost interest.+ Outstanding loan balance at time lease expires.- Market value of vehicle at time lease expires.= Net cost of buying.

When you lease, you're not paying for the entire vehicle, but rather the value you use up for the time you're driving it. When buying a vehicle, monthly payments go toward repaying the lender, plus interest. Unlike leasing, where your leaser owns the vehicle and you continue to pay monthly for the length of the lease.

North Carolina General Statute Chapter 47G governs Option to Purchase Contracts executed with Lease Agreements. The leases that are covered under the statute are residential lease agreements that are combined or executed with an option contract.

On the one hand, buying involves higher monthly costs, but you own an assetyour vehiclein the end. On the other hand, a lease has lower monthly payments and lets you drive a vehicle that may be more expensive than you could afford to buy, but you get into a cycle in which you never stop paying for the vehicle.

Whether you decide to lease or buy is dependent on several factors, such as the type of item you're debating over (real estate or equipment), the fair value of the asset, how you want your company financials to look over time, and the amount of capital your business currently has.

On the surface, leasing can be more appealing than buying. Monthly payments are usually lower because you're not paying back any principal. Instead, you're just borrowing and repaying the difference between the car's value when new and the car's residualits expected value when the lease endsplus finance charges.