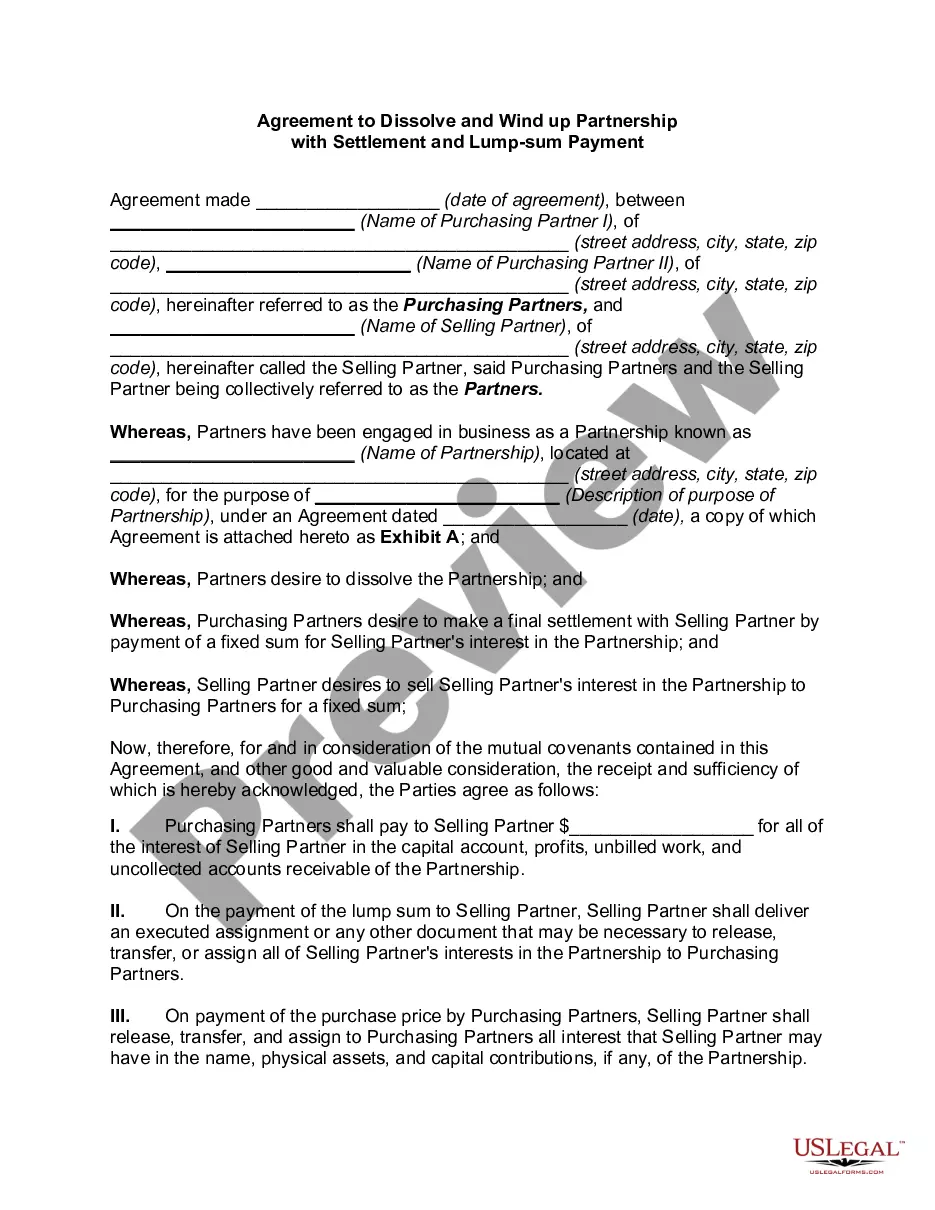

Mississippi Agreement to Dissolve and Wind up Partnership with Settlement and Lump Sum Payment

Description

How to fill out Agreement To Dissolve And Wind Up Partnership With Settlement And Lump Sum Payment?

If you are looking to acquire, obtain, or create legitimate document templates, utilize US Legal Forms, the largest collection of legal forms available online.

Take advantage of the site's user-friendly and efficient search feature to locate the documents you need.

Various templates for business and personal purposes are categorized by types and subjects, or keywords.

Step 5. Complete the payment process. You can use your credit card or PayPal account to finalize the transaction.

Step 6. Choose the format of the legal form and download it to your device. Step 7. Fill out, revise, and print or sign the Mississippi Agreement to Dissolve and Wind Up Partnership with Settlement and Lump Sum Payment. Every legal document template you purchase is yours forever. You have access to all forms you downloaded within your account. Go to the My documents section and select a form to print or download again.

- Use US Legal Forms to access the Mississippi Agreement to Dissolve and Wind Up Partnership with Settlement and Lump Sum Payment in just a few clicks.

- If you are a current US Legal Forms user, Log In to your account and click the Download button to retrieve the Mississippi Agreement to Dissolve and Wind Up Partnership with Settlement and Lump Sum Payment.

- You can also find forms you previously downloaded in the My documents section of your account.

- If this is your first time using US Legal Forms, follow the instructions below.

- Step 1. Ensure you have chosen the form for the correct city/state.

- Step 2. Use the Preview option to view the contents of the form. Be sure to read the description.

- Step 3. If you are dissatisfied with the form, utilize the Search field at the top of the screen to find alternative versions of the legal form template.

- Step 4. Once you have found the form you need, click the Purchase now button. Select your preferred pricing plan and enter your details to create an account.

Form popularity

FAQ

When a partnership dissolves, the individuals involved are no longer partners in a legal sense, but the partnership continues until the business's debts are settled, the legal existence of the business is terminated and the remaining assets of the company have been distributed.

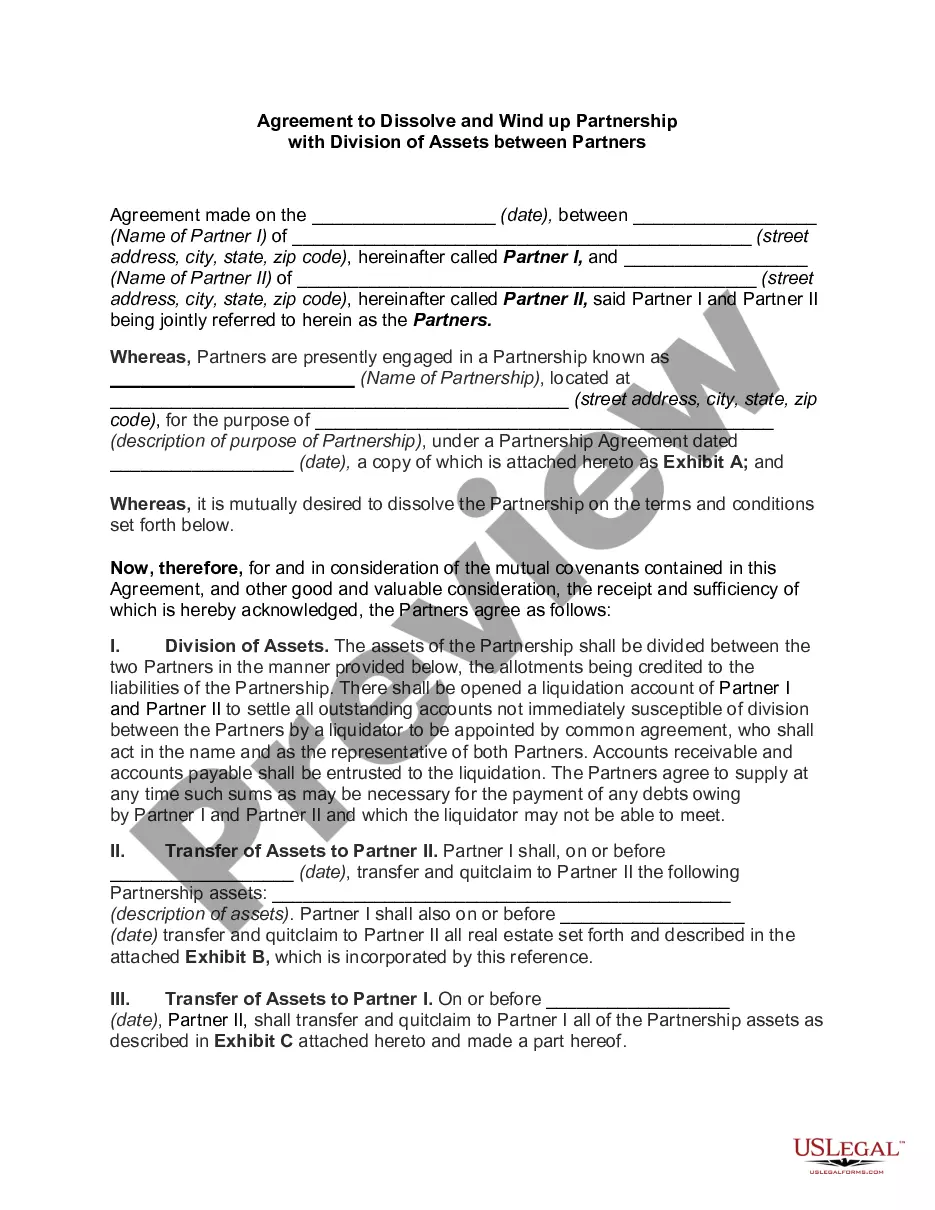

Only partnership assets are to be divided among partners upon dissolution. If assets were used by the partnership, but did not form part of the partnership assets, then those assets will not be divided upon dissolution (see, for example, Hansen v Hansen, 2005 SKQB 436).

The proceeds from the sale of assets along with the contribution of the partners at the time of dissolution of the firm are first used up to pay off the external liabilities, i.e., the creditors, bank loans, bank overdrafts, bills payable etc.

An agreement can spell out the order in which liabilities are to be paid, but if it does not, UPA Section 40(a) and RUPA Section 807(1) rank them in this order: (1) to creditors other than partners, (2) to partners for liabilities other than for capital and profits, (3) to partners for capital contributions, and

When a partnership dissolves, the individuals involved are no longer partners in a legal sense, but the partnership continues until the business's debts are settled, the legal existence of the business is terminated and the remaining assets of the company have been distributed.

Dissolution of a limited partnership is the first step toward termination (but termination does not necessarily follow dissolution). The limited partners have no power to dissolve the firm except on court order, and the death or bankruptcy of a limited partner does not dissolve the firm.

The liabilities of the partnership shall rank in order of payment, as follows:Those owing to creditors other than partners,Those owing to partners other than for capital and profits,Those owing to partners in respect of capital,Those owing to partners in respect of profits.

Settlement of accounts on dissolutionPayment of the debts of the firm to the third parties.Payment of advances and loans given by the partners.Payment of capital contributed by the partners.The surplus, if any, will be divided among the partners in their profit-sharing ratio.

If dissolution is not covered in the partnership agreement, the partners can later create a separate dissolution agreement for that purpose. However, the default rule is that any remaining money or property will be distributed to each partner according to their ownership interest in the partnership.

An agreement can spell out the order in which liabilities are to be paid, but if it does not, UPA Section 40(a) and RUPA Section 807(1) rank them in this order: (1) to creditors other than partners, (2) to partners for liabilities other than for capital and profits, (3) to partners for capital contributions, and