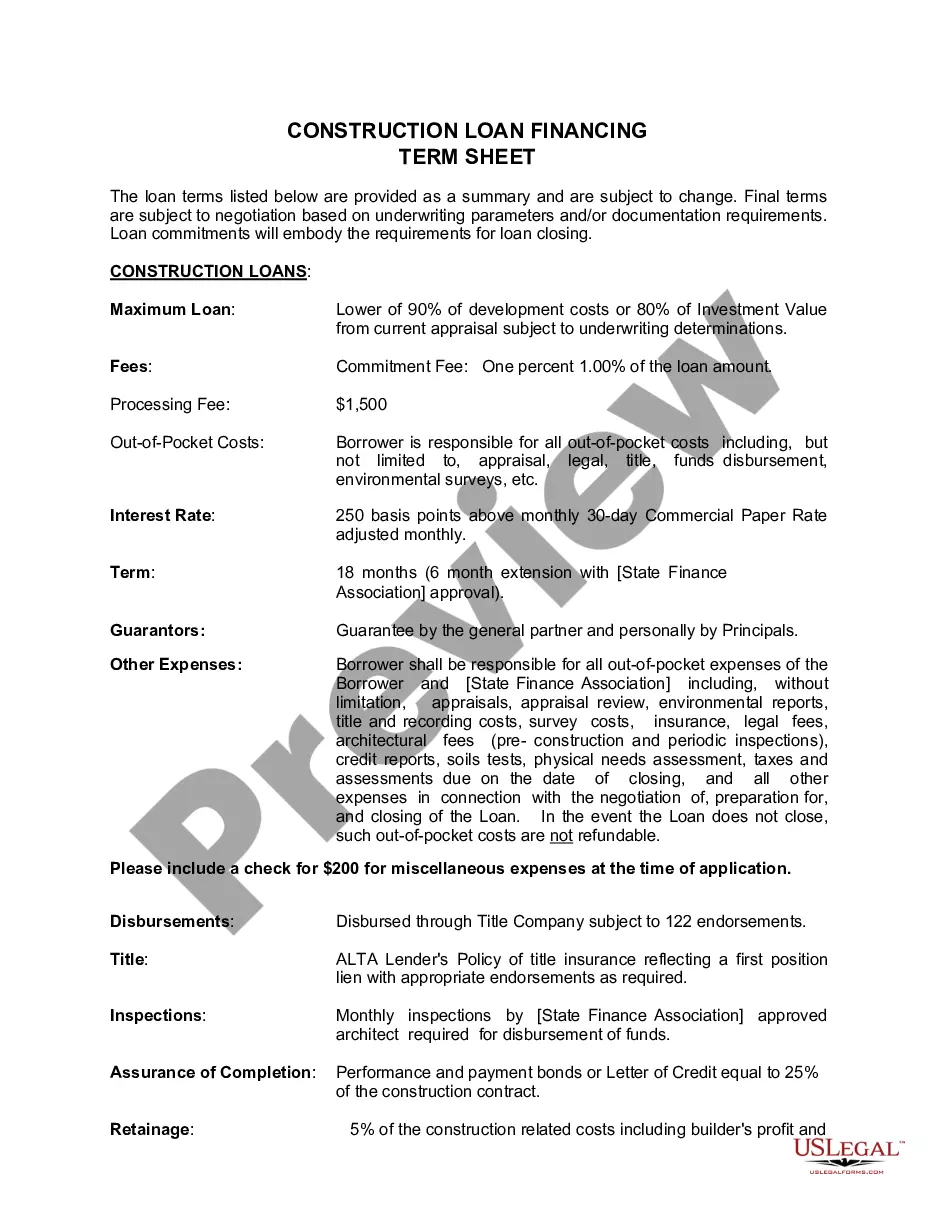

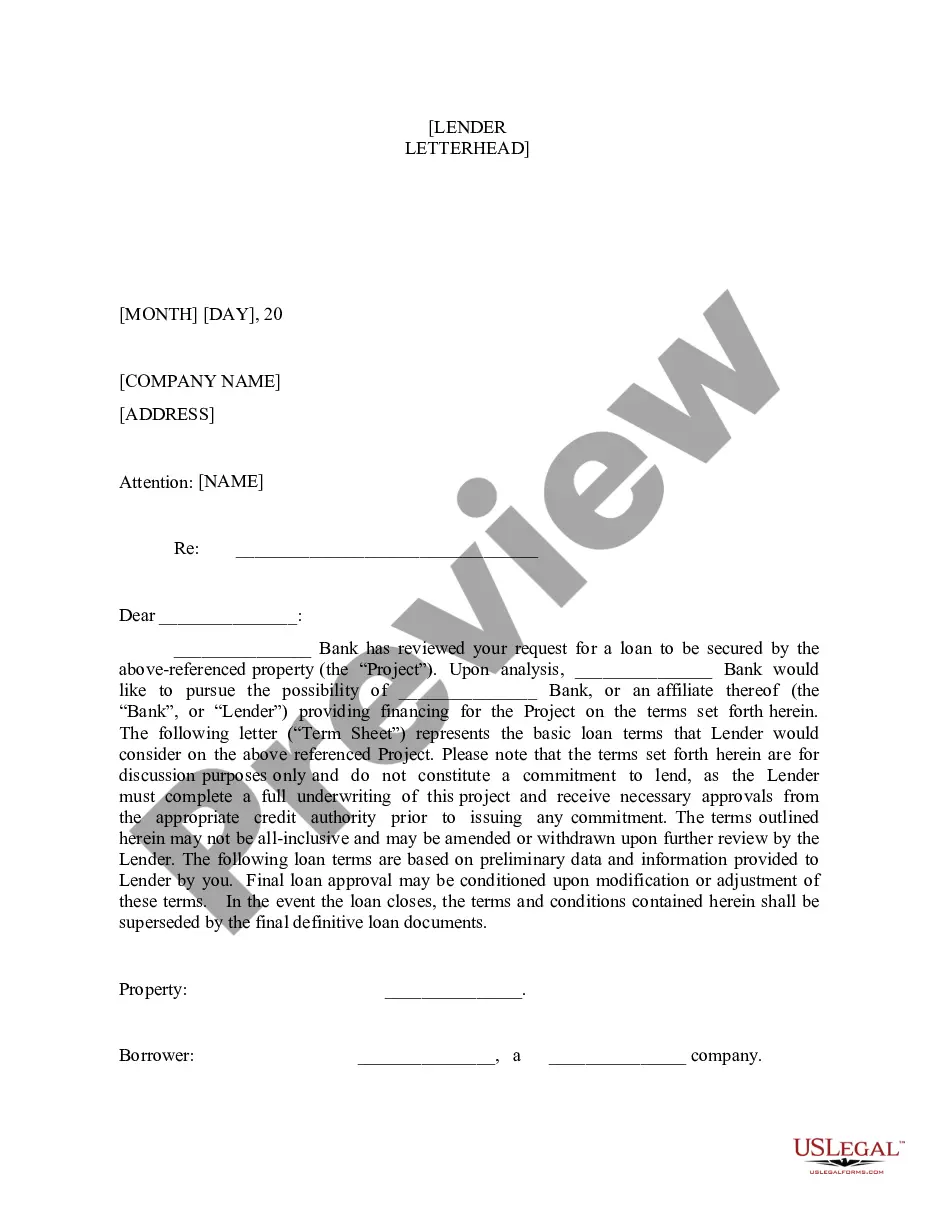

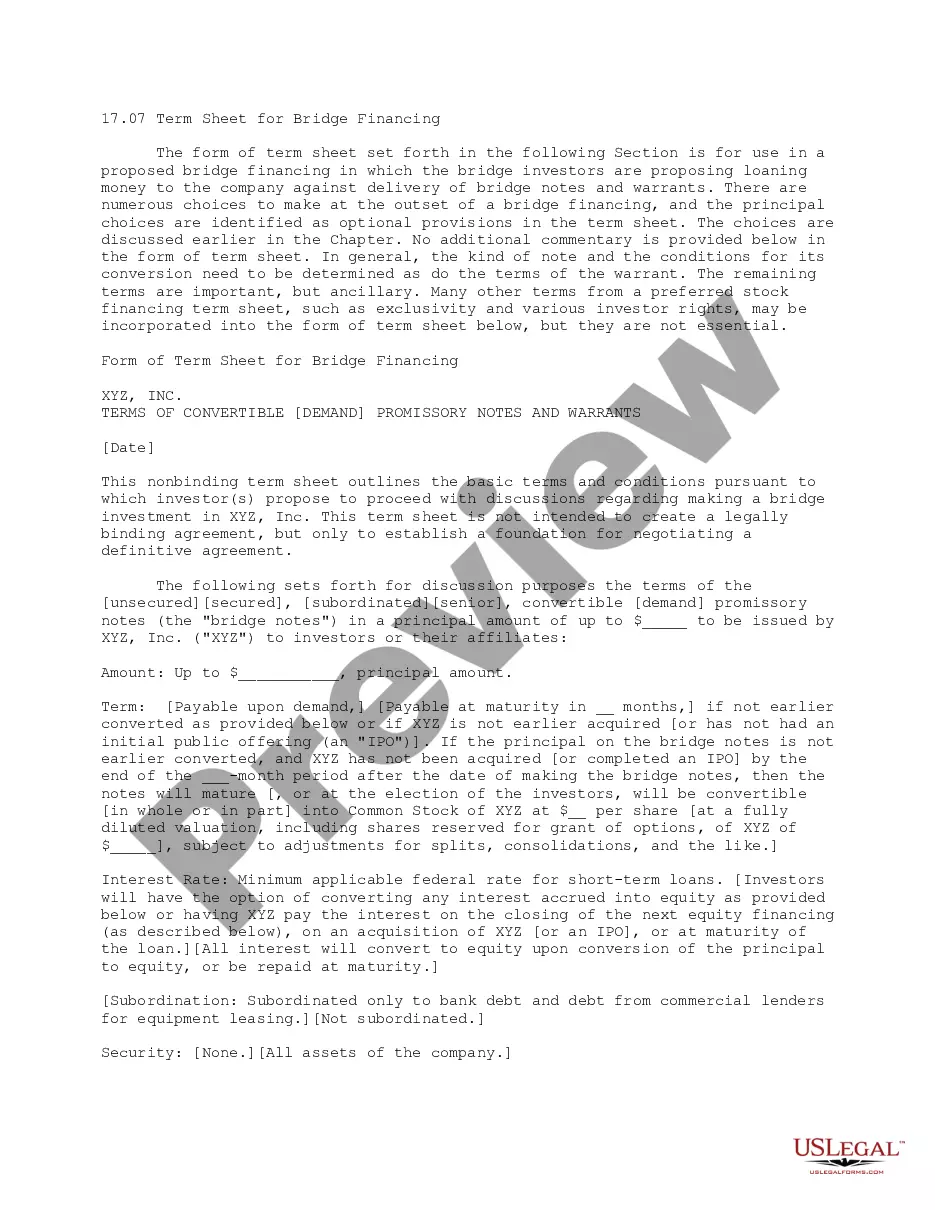

Missouri Construction Loan Financing Term Sheet

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Construction Loan Financing Term Sheet?

If you have to comprehensive, down load, or printing authorized papers templates, use US Legal Forms, the largest collection of authorized forms, that can be found online. Take advantage of the site`s simple and easy handy look for to obtain the documents you will need. A variety of templates for organization and personal functions are categorized by types and states, or keywords and phrases. Use US Legal Forms to obtain the Missouri Construction Loan Financing Term Sheet in just a handful of clicks.

When you are currently a US Legal Forms client, log in in your bank account and click on the Acquire option to find the Missouri Construction Loan Financing Term Sheet. Also you can entry forms you formerly saved inside the My Forms tab of your respective bank account.

If you are using US Legal Forms initially, refer to the instructions under:

- Step 1. Make sure you have chosen the shape for the proper town/land.

- Step 2. Take advantage of the Review method to look through the form`s content. Do not forget about to read the explanation.

- Step 3. When you are unhappy together with the form, make use of the Lookup field towards the top of the screen to find other types from the authorized form design.

- Step 4. Upon having identified the shape you will need, go through the Get now option. Opt for the prices prepare you like and put your references to sign up to have an bank account.

- Step 5. Method the transaction. You should use your charge card or PayPal bank account to complete the transaction.

- Step 6. Select the structure from the authorized form and down load it on the system.

- Step 7. Complete, change and printing or sign the Missouri Construction Loan Financing Term Sheet.

Every single authorized papers design you buy is your own property permanently. You may have acces to every form you saved in your acccount. Click on the My Forms portion and select a form to printing or down load once more.

Contend and down load, and printing the Missouri Construction Loan Financing Term Sheet with US Legal Forms. There are many specialist and status-particular forms you can utilize for your organization or personal demands.

Form popularity

FAQ

With a construction loan, the lender typically agrees to loan a certain percentage (95%, for example) of the future home's appraised value. Then, they'll suggest a down payment equal to the difference between the approved loan amount and the construction costs.

This includes the term, loan size, interest rate, and other financial matters common to debt. Risk mitigation preferences. The lender will often require specific conditions be met or specific information be provided on a recurring, timely manner.

As mentioned, construction loans are short-term loans, usually no longer than a year in length. On the other hand, traditional mortgages are long-term loans, with terms typically ranging from 15 ? 30 years. With a mortgage, the borrower receives the money in one lump sum.

So, for instance, if the home is appraised to be worth $500,000, they will loan you $500,000 x (95% as an example) = $475,000. The down payment will be your construction costs less the loan amount. So, if the construction is quoted to cost $500,000, your down payment will be $500,000 - $475,000 = $25,000.

Construction loans are typically paid out in installments as construction progresses. You will need to calculate the interest charges for each installment period. To do this, you simply multiply the loan amount by the interest rate for each period.

Personal Financial Responsibility: If you are responsible for covering the additional costs, you may need to contribute additional funds from your own pocket to cover the overage. This can strain your personal finances and potentially disrupt your financial plans.

These loans usually mature after about a year or less. Once the term is complete and your home is built, you will meet with your lender to begin conversion of your construction loan to permanent financing. You will have to apply separately for a permanent financing..